Recently, entrepreneurial lawyers have taken up the cause of renters who stopped paying their mortgages, as if they are somehow the victim in this mortgage crisis. The mortgage crisis has certainly generated a lot of damage, but those who bought houses with teaser rates with little money down are hardly victims (Michael Moore compares them to rape victims), but rather, scammers looking for a free lunch (underpriced options of home values).

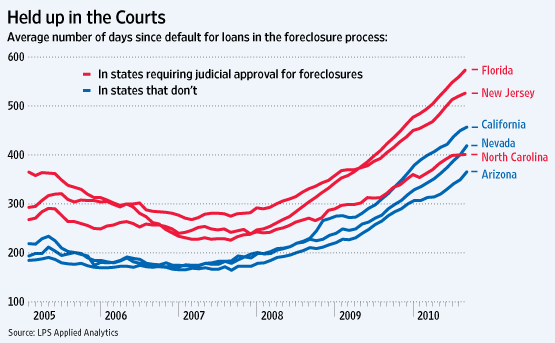

A chart in the WSJ shows the increase in time it takes between when a homeowner stops paying his mortgage, and when a bank can actually take possession of the property. The average time over all states in 478, and the latest activity to help the non-paying renters will probably boost that further.

The families of the 9/11 victims averaged $1.8MM for their injustice, the 33 victims of the USS Cole that were killed by Al Quada got about $0.4MM, and those who were killed idiosyncratically generally received nothing. The key to being a successful victim is to be a victim others can empathize with, thus the more the easier it is to do.

I remember in my litigation I was a modestly rich guy in fending off litigation from my former employer, a very (~100x more) rich guy. While I was in my career time out I spoke with a state legislator about state law, noting that unlike other states a party did not have to specify the intellectual property in question when alleging a violation of said property. Now, any proposed legislation would not affect me, but I thought the status quo was unjust. The law made confidentiality agreements perpetual non-competes for litigious parties with sufficient means (you can read more here). The legislator told me straight up: “it does not happen enough to a group anyone cares about’. True enough. Who cares about an hedge fund employee getting screwed? When my lawyer told the judge the allegations against me were costly and prevented my ability to work she said “Can’t he golf?”, and the courtroom laughed. Sympathy is for the historically disadvantaged, the poor, and people aligned with such groups, and sympathy often leads to specific redress if not subsidy.

On the other hand, when everyone is a victim, by definition you can’t give yourselves a boatload of money, because it has to come from somewhere else. Thus, you have the Laffer curve of redistribution where if you suffer a bizarre injustice or injury, you get no money or sympathy, and if everyone suffers an injury, you have to suck it up (though, like our ‘greatest generation‘ you can capture sympathy if not respect from future generations about your suffering later).

A key here is the conflation of injustice and injury. Injustice implies a third party was negligent or malicious, whereas injury is just random bad luck. From a societal point of view it makes a difference because we ought to compensate victims of injustice and they get to take the moral high ground, while victims of bad luck just get put into standard welfare programs. In practice, the difference is whether one side’s affiliation can provide useful indirect support as a PR prop or voting block, or whether one party himself can provide useful direct support. The facts in disputes are pretty messy, requiring more effort than most are willing to apply, but the benefits are usually straightforward, and you can predict interested people’s inference of messy facts pretty well based on which inference offers them greater benefits.

Currently, the homeowners are changing the mortgage contract ex post because lawyers and politicians find them useful muckraking props for their power and profit grabs. Prior default curves for mortgage cohorts are now totally irrelevant because there is now little stigma for defaulting on a mortgage–rather the opposite–and you get to live rent free for a longer time if you stop paying. Pre-2006 was a different world for mortgage behavior. Such expropriations are not free, however, they get built into current prices and contracts, and so make things much worse because sellers and lenders rationally anticipate lower recovery rates and higher default rates. The current housing morass will not get better until government stops ‘helping’.

Leave a Reply