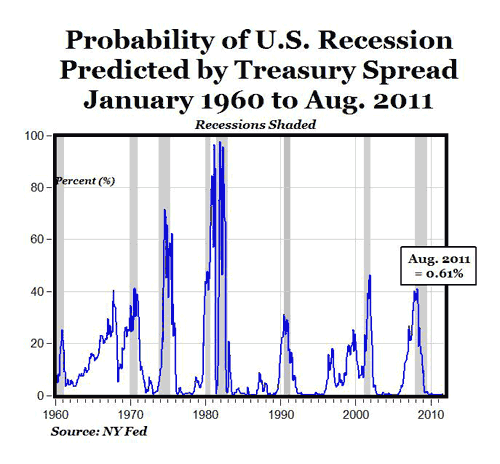

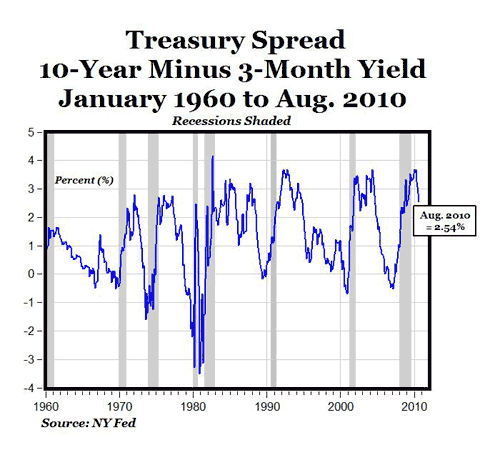

The New York Federal Reserve updated its “Probability of U.S. Recession Predicted by Treasury Spread” yesterday with treasury yield data through August 2010, and the Fed’s recession probability forecast through August 2011 (see top chart above). The NY Fed’s Treasury model uses the spread between the yields on 10-year Treasury notes (2.70% in August) and 3-month Treasury bills (0.16%) to calculate the probability of a U.S. recession up to twelve months ahead (see details here) using the spread between those two yields (2.85% in August, see bottom chart above).

The Fed’s model (data here) shows that the recession probability peaked during the October 2007 to April 2008 period at around 35-40% (see chart above), and has been declining since then in almost every month. For August 2010, the recession probability is only 0.08% and by a year from now in August of next year the recession probability is slightly higher, but only 0.61% (about 6/10 of 1%). According to the NY Fed Treasury Spread model, the chances of a double-dip recession through the middle of next year are essentially zero.

Leave a Reply