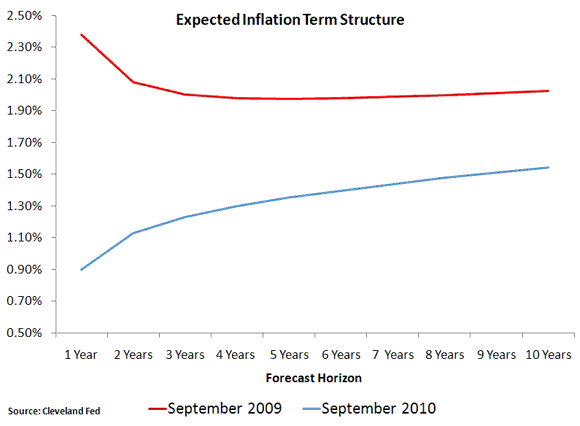

As you prepare for an important FOMC meeting, I would like to direct your attention to several graphs and ask that you consider their implications. First up is a figure of monthly expected inflation across different horizons that comes from the Cleveland Fed. The data is based, in part, on the Treasury market. This figure shows expected inflation in September 2009 and in September 2010. Note that the one-year inflation forecast over the last year went from 2.38% to 0.90% while the ten-year forecast moved from 2.03% to 1.54%. As I have shown before, a dramatic downward trend underlies these differences:

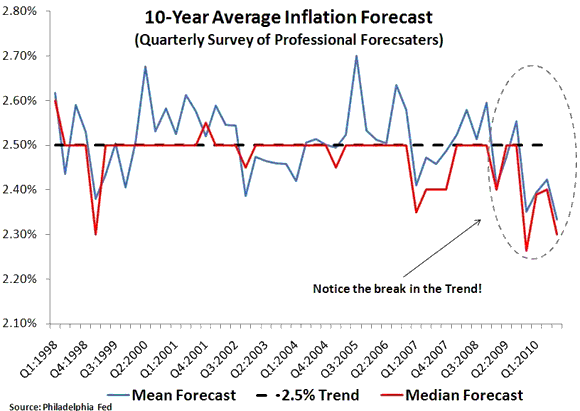

Second up is a figure showing the 10-year average CPI inflation forecast from the Philadelphia Fed’s Survey of Professional Forecasters. This survey is on a quarterly frequency, but tells a similar story to the monthly Cleveland Fed data: there has been a downward trend over the last year or so:

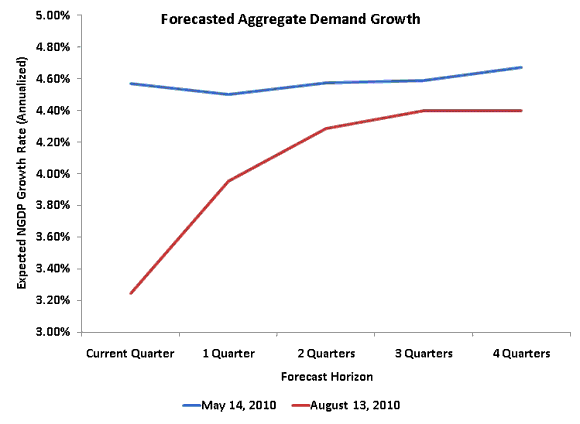

Third up is the mean quarterly forecast (median is similar) of nominal GDP from this same survey. It too shows a decline in the forecast:

In short, whether it is market-driven data (Cleveland Fed) or survey data (Philadelphia Fed), the nominal economic outlook is down. Now the Fed can shape nominal expectations if it really wanted to so, but according to these figures it is not. How do you as a member of the FOMC interpret this passivity? Would it be too much to say that by failing to act the FOMC is effectively tightening monetary policy? This is something I would like you to consider this evening and as you do your final preparations for the big meeting tomorrow.

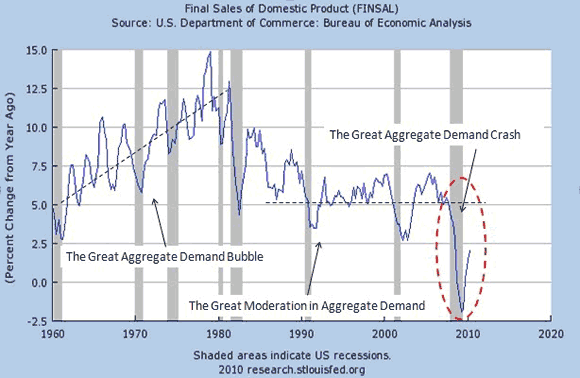

Oh, one more thing. The figure below shows the historical growth rate of actual aggregate demand (AD), as measured by final sales of domestic output, up through 2010:Q2. Based on one of my more popular blog posts, I have added some labels to this figure which comes from the St. Louis Fed. This figure shows that not only was there a Great AD Crash, but the AD recovery is far from complete. Between the declining forecast above and this incomplete AD recovery does it not seem that monetary policy should be doing more?

Thanks for listening and I look forward to your valiant efforts to stabilize aggregate spending.

Leave a Reply