However you want to describe it — green shoots, changes in the second derivative, inflection points — talk of a brighter future is all the rage, even in the most pessimistic of hearts. That may be the case but where might all of this take us. Here is some dot connecting from a couple different sources that might at least give one scenario.

First, the NYT had a report on Christina Romer’s latest pronouncements. She is of the opinion that the economy needs to achieve a growth rate of 2.5% before unemployment will fall. Ms. Romer expects GDP growth will approximate 3% in 2010.

Now 2.5% is pretty much trend rate which would be fine if you didn’t look behind that number to see what drove it and you probably know what it was. It was of course, consumer spending. That was the engine of growth and it, by many accounts, is severely damaged. Lost wealth, stagnant incomes and excessive debt loads throw into doubt the likelihood of any robust rebound in consumer spending.

Here is a little bit of the history of consumer spending from the Economist:

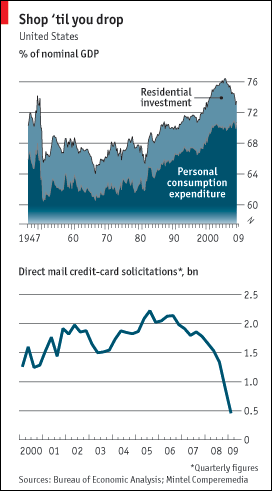

Since the early 1980s, spending by households on goods, services and homes has grown faster than GDP, making it the locomotive of American—and global—expansion. By 2006 it accounted for 76% of nominal GDP, the highest since quarterly data begin in 1947 (see top chart).

This was accompanied by a steady decline in the personal saving rate and a rise in household debt relative to income. By itself, this was not a problem; household debt has risen relative to income since the 1950s, as a growing share of the population has taken out mortgages. Despite the higher debt burden, falling interest rates kept total household financial obligations—interest payments, rent and leases—within a range during the 1980s and 1990s.

An inflection-point occurred around 2000. Income growth stagnated but debts continued to grow rapidly, from 94% of income to 133% in 2007. The share of income devoted to servicing those obligations also jumped. A study in 2007 by Karen Dynan and Donald Kohn, both of the Fed, attributed that partly to more of the population reaching home-buying age, and mostly to a rise in home prices which made it possible to borrow more.

Financial innovation also played a role as the industry devised new ways for Americans to borrow against their homes. One manifestation was the plethora of credit-card offers to even marginal borrowers: more than 8 billion poured into Americans’ mailboxes in 2006, according to Mintel Comperemedia, a consumer-research firm. From 2003 to the end of 2006, consumers borrowed almost $2 trillion against their properties via home-equity loans and “cash-out” mortgage refinancings. A dramatic reversal is now under way. Last year household wealth fell by 18%, or by $11 trillion. Macroeconomic Advisers, a forecasting firm, estimates the resulting negative “wealth effect” will depress consumption by 2% this year.

Since the early 1980s, spending by households on goods, services and homes has grown faster than GDP, making it the locomotive of American—and global—expansion. By 2006 it accounted for 76% of nominal GDP, the highest since quarterly data begin in 1947 (see top chart).

Since the early 1980s, spending by households on goods, services and homes has grown faster than GDP, making it the locomotive of American—and global—expansion. By 2006 it accounted for 76% of nominal GDP, the highest since quarterly data begin in 1947 (see top chart).The article goes on to state the obvious and oft stated conclusion that consumers are going to have to deleverage. The question is how far do they deleverage and the author offers that if they could get back to 2000 levels that would probably represent a comfort zone for investors. The problem is that getting back to that level will require a real pullback for more than a few years.

This is how they bracket the effects:

This process, known as deleveraging, requires consumption to grow more slowly than income in coming years. A sudden rush to return debt ratios to where they were in 2000 would require ridding households of some $3 trillion in mortgage debt—an almost impossible task. More probably, mortgage debt will grow more slowly than income through a combination of lenders writing off impaired loans, homeowners paying down existing mortgages and new homeowners taking out smaller mortgages than in the past. Bruce Kasman of JPMorgan Chase estimates that the most dramatic phase of increased saving has already occurred, and spending will grow only a bit less than income.

But Martin Barnes of BCA Research, a financial-forecasting service, is more pessimistic. For debt to return to a more sustainable trend, real consumer spending would need to grow by just 1.3% a year from 2009 to 2013, the weakest such five-year stretch since the 1930s. It could grow even more slowly than that if taxes rise faster, he reckons, or if stagnant productivity impedes real-income growth.

This implies that for America to grow at a trend rate of about 2.5% something else will have to grow more quickly. Ideally that would be exports and investment. But given the torpor in the rest of the world, that will not be easy.

So, getting to that magical 2.5% number might be harder that Ms. Romer thinks. And to the extent you don’t get there it almost becomes a game of chasing one’s tail. As unemployment becomes chronic consumer spending is suppressed and to the extent unemployment does drop, the additional income goes to saving and deleveraging instead of consumption thus retarding further improvement.

John Jansen who writes Across the Curve was musing on these numbers this morning and put together a pretty cogent analysis:

In order for the unemployment rate to stabilize the economy needs job growth in the neighborhood of 150K to account for the new workers entering the work force each month. We are light years away from reaching that level.

Without a healthy labor market there can be no growth in income and without that support consumption will languish. With home prices decimated and consumers’ faith in the resiliency of their 401Ks shattered consumption will compete with savings for cash as consumers repair their finances. The savings rate is now 4 percent and some analysts see it pushing towards 7 percent and 8 percent.

That is a significant amount of sacrificed consumption which translates into slower labor market recovery and slower profit growth for business.

Business investment should also lag in the upcoming periods. One of the more interesting pieces of data which will be published later this week is capacity utilization. That series is a record lows and indicates a surfeit of excess capacity in the system. If one believes that ( and I have no reason to disbelieve) then from what source will business investment spring.

I am an armchair economist only but an awful lot of that excess capacity will need to be employed before business investment can stage a robust recovery.

My base premise is that after 25 years of economic growth in which economic growth was around 3 percent, I think we are about to enter a period in which growth is closer to 2 percent. I will check the 3 percent average. That is a guess from the vantage point of my “armchair”. But my point is that we will retrench and experience slower growth in the years ahead.

I also believe that there is a 1000 pound gorilla in the room in the form of future tax increases. Given the deficit forecasts of the Administration and the activist agenda on which they have embarked it is inconceivable to me that the Administration will not reqeust a tax hike sometime in the future. And I mean a healthy tax hike which reaches down into the middle class to raise revenue.

Jansen throws a few other ingredients into the economic crock pot but seems to come to the same conclusions with regard to employment and consumption. It’s a conundrum that won’t be easy to solve.

Many would and do argue that the American consumer will be back on their horses sooner than most believe. That after a period of deleveraging they will adapt to a debt level that’s considerably higher than 2000. I, for one, am leery of counting out the country’s propensity to consume and wouldn’t be surprised if spending did rebound quicker than the folks I’ve cited here expect. At the same time, I can see the jolt that’s been delivered to my circle of acquaintenances by the events of the last 18 months or so. Habits have changed and I think it might be some time before they are comfortable with any new obligations.

So, we might very well find ourselves in a sort of under-consumption trap. If Americans do continue to save at elevated rates, at least in terms relative to recent history, unemployment could become a persistent problem. If unemployment becomes a persistent problem then even if the savings rate goes down the overall level of consumption is going to be insufficient to move the economy up to a sustainagle growth level.

Jansen also wrote of the probablility of a rather significant tax increase. It seems pretty obvious that on the current curve and with the addition of very expensive new initiatives from the Obama administration that must come to pass. But, of course, if you have a chronic unemployment problem along with a weak consumer sector, that’s an economic and political impossibility. Traps beget traps.

The way out is naturally investment and the creation of new jobs via new industries. I’ve no doubt that will happen and it will happen in this country before it occurs elsewhere. If nothing else, America is quite good at reinventing itself. That isn’t a short-term process and also not one that’s likely to be started by government regardless of all the claims for health care and green technologies leading us out of the wilderness.

Recovery may indeed be on the horizon but it looks as if those who predict a weak one are probablyl spot on. In fact, it looks very much like we could be revisiting the 70’s again. That wasn’t a fun decade.

Graph: Economist

What recovery? You’re speaking as if this fantasy creature exists, when it in fact does not. I think there will be no ‘recovery’. I think that business as usual is done.