Alright so the Fed isn’t going to defend the 10yr at 3%, and in fact appears to be targeting the belly of the yeild curve. That doesn’t change the fundamental problem of deflation. Near term, based entirely on technicals, I’ve made a small short play in Treasuries. But I’m really just looking for a new entry on the long-side.

Almost exactly 2-years ago, I made my now famous (in my own mind) analogy of inflation to a Monopoly game. Basically my point was inflation wasn’t about the price of any given property (or good) but the price of all the properties. Allowing any given good (at the time it was energy) to rise isn’t, in and of itself, inflation.

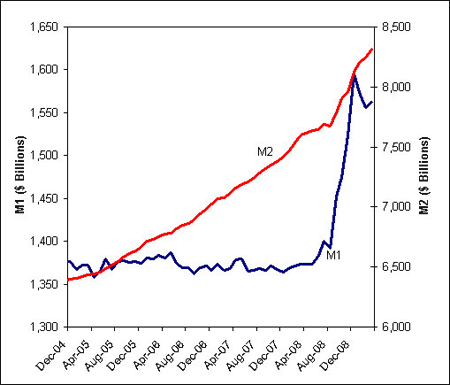

Now there is fear that the Fed and Treasury’s activities, especially the Fed’s recent panache for “crediting bank reserves” (which means printing money). Here is the chart for M1 and M2 up 14% and 9% respectively in the last year.

Back to my Monopoly analogy. We might think of the M’s as the actual multi-colored cash that each player has. As I demonstrated two years ago, an increase in cash available should cause the price level to rise, but only if you hold the savings rate constant.

Speaking more technically, you could say that an increase monetary base would have some multiplied impact on transactable money. In your textbook from college, this only involved banks and their willingness to lend. Actually, most often text books assume banks want to lend as much as they are legally allowed, which isn’t the case right now. But I digress.

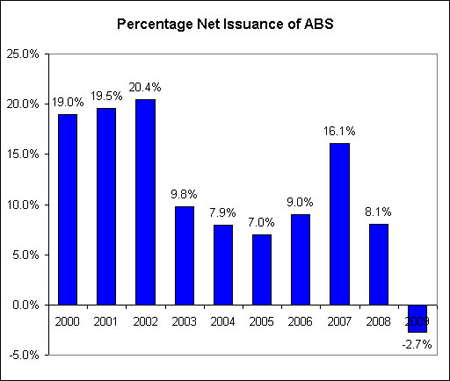

The securitization market makes this all much more complicated. The supply of loanable funds isn’t just a function of cash in the banking system, but also cash invested in the shadow banking system. Right now net new issuance in ABS (meaning new issuance less principal being returned in old issues) is negative, meaning supply of funds from the shadow banking system is contracting.

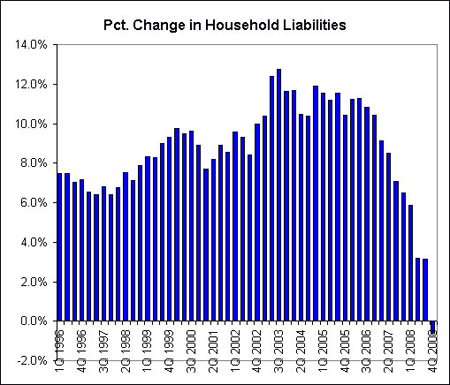

This contraction of funds doesn’t show up anywhere in the Ms, at least not directly, but obviously it matters in terms of consumers ability to buy goods. And it isn’t just about availability of credit, which had everything to do with liquidity. Its about demand for credit also. Consumers want to save, they don’t want to borrow right now. The following chart of household liabilities shows consumers actually decreased their total liabilities in 2008, the first year-over-year outright decline since the Federal Reserve began keeping the data in 1952.

Consumers are like a Monopoly player who has mortgaged all his properties. Passing GO doesn’t cause him to buy more houses, it causes him to unmortgage his properties! That isn’t inflation!

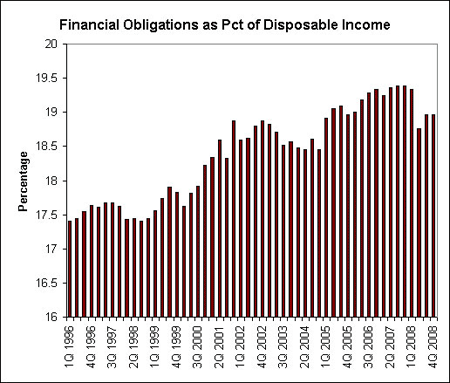

Getting back to consumers, it isn’t clear to me that consumers are actually running out of money. Check this chart of the Household Financial Obligation Ratio, basically a debt service coverage ratio for consumers.

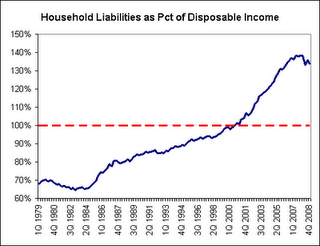

So consumers might not have to repay debt all at once, which is nice. It means a second-half recovery of sorts remains in play. But the large losses in assets coupled with out-sized debt ratios are going to cause consumers to keep saving at an elevated level. Check out liabilities as a percentage of disposable income.

This isn’t a perfect ratio, since liabilities is a stock and income is a flow. But with declining asset values (both homes and financial assets), means that consumers are actually going to have to rely on incomes to pay debt service. Or for that matter to qualify for loans. So I’d think this ratio moves back toward 100%. That implies $3.6 trillion. TRILLION. It will be repaid over time to be sure, but it will remain a continual drag on consumer spending levels.

So keep this in mind when you think about the size of Fed/Treasury programs. $3.6 trillion. Are we worried about $800 billion for the “Stimulus Package” or the $1 trillion revised TALF? Not in terms of inflation.

I’m looking forward to the day when I’m worried about inflation. It isn’t today.

Leave a Reply