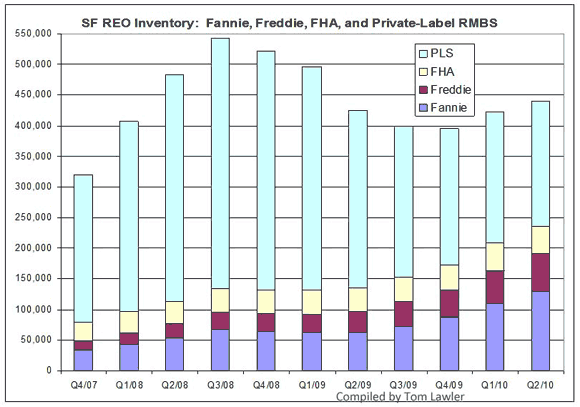

The ultimate indication of a mortgage that has gone bad is when the lender forecloses and ends up owning the property. The graph below (from http://www.calculatedriskblog.com/) shows the number of properties that are in “Real Estate Owned” status (REO) by Fannie Mae (FNMA), Freddie Mac, the Federal Housing Authority and owned by the owners of the private-label mortgage-backed securities that were created by the likes of Merrill Lynch – now part of Bank of America (BAC) and its now defunct brethren Bear Stearns – now owned by J.P. Morgan (JPM) and Lehman Brothers. The graph speaks volumes about the housing bubble and its aftermath.

The first thing to note by way of background is that the private-label paper creation pretty much came to an end in 2007 when the housing market first started to fall apart. At that point there was huge pressure on Fannie and Freddie to step up their activities, since otherwise mortgages would simply not be available. Still it is clear that early on, the worst loans were the ones that were being funded by Wall Street, not the conforming loans backed by Fannie, Freddie and the FHA (collectively, the F’s).

The light blue bar is far larger early on than all of the F’s combined. Through 2008, the private-label paper was dramatically increasing the number of homes foreclosed on, and of which they eventually took ownership. Since then, the banks that service these loans have been aggressive in auctioning them off.

Meanwhile the number of mortgages that the F’s have had to foreclose on and take ownership off has steadily increased. Still, the number of owned properties from the private label side still make up about as much as the three F’s combined.

Just to be clear, none of the private-label mortgages that went bad had anything to do with the Community Reinvestment Act (CRA), since the mortgage brokers who made these loans and then sold them to Wall Street to be sliced and diced in their magic Cuisinart were not subject to the provisions of the CRA. That Cuisinart turned the rotten vegetables of subprime and alt-A loans in to the gourmet AAA meals with the assistance to the sous chefs of S&P, Moody’s and Fitch. That meal is what gave the entire world economy food poisoning.

The F’s were relatively late to the game. This was not really due to any great virtue on the part of Fannie and Freddie, but because they were constrained by earlier (and unrelated) accounting scandals. However, once the private-label market begain to implode, there were very real fears than there would simply be no mortgage credit available. Congress stepped up the pressure on Fannie and Freddie (and the FHA, to a lesser degree) to step up their activities.

One of the things that they did was to raise the limit on conforming loans (those that the F’s were allowed to own and back) to $730,000 from under $400,000 since the “jumbo” mortgage market was being exclusively fed by the private-label side. In some areas of the country, notably on the coasts, $400,000 would not buy even a starter home in a dubious neighborhood at the top of the bubble.

The F’s stepped into the breach and dramatically increased their market share of the mortgage market during 2007 and 2008. With the demise of the private-label market, at one point the F’s were responsible for over 95% of the new mortgages being written (either owned or backed).

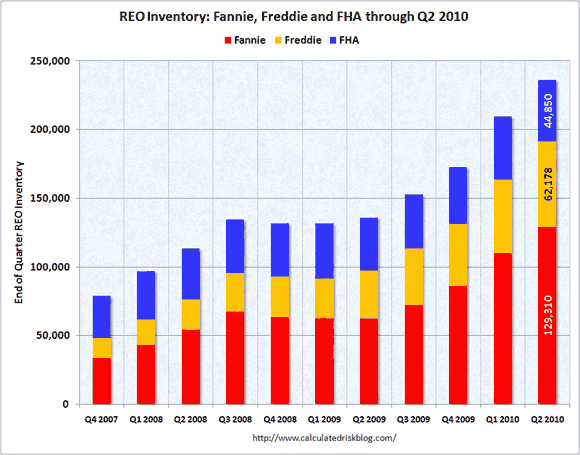

The second graph presents the same data, but just for the F’s — to make things a bit clearer — and to better show the growth in the Fs’ REO portfolios. Collectively, they increased by 13% in just the second quarter, and over the last year they have increased by 74%. In raw numbers, the F’s now own over 236.000 homes, up from less than 136,000 a year ago.

The Ugly Outlook

If anything, it looks like the growth of the F’s REO portfolio is accelerating. Like the banks that serviced the private-label paper, the F’s have no real desire to win these properties and become landlords. They are going to have to sell them off. As they do, that will put additional downward pressure on housing prices.

That, in turn, will leave more homeowners underwater on their mortgages, and thus vulrerable to foreclosure. The mess caused by the popping of the housing bubble is far from being cleaned up. Fannie and Freddie are now wards of the Federal Government and continue to lose money (although a big part of those losses are due to the interest payments they are making on loans from the Federal Government, their 80% owner, so there is a bit of double-counting going on).

The F’s continue to be a big drag on the Federal Budget, but if they were to suddenly go away, it is unlikely that the private sector would quickly step up to the plate. They certainly would not do so at the currently prevailing ultra-low mortgage rates. The financial reform legislation that was recently passed did not address the question of the F’s since what it did tackle was complicated enough. Separate legislation is going to be required next year on what to do with Fannie and Freddie.

Simply shuttting them down or allowing them to go into run off would throw the housing market into even more chaos. If they were fully nationalized, then all of their debt — about $5 trillion — would have to be consolidated into the federal debt, significantly raising the debt-to-GDP ratio. If we leave things as they are, then Fannie and Freddie are likely to continue to be a drag on the budget. There does not seem to be a good solution to the problem.

BANK OF AMER CP (BAC): Free Stock Analysis Report

JPMORGAN CHASE (JPM): Free Stock Analysis Report

FANNIE MAE (FNMA): Free Stock Analysis Report

Leave a Reply