Polaris Industries (PII) showed once again that consumers are wild about its off-road vehicles. Last week, the company delivered another strong earnings report.

Growth and Income

Analysts estimate that Polaris will grow its earnings per share 27.7% in 2010, 11.2% in 2011, and 12.5% per year for the next three to five years. In addition, the company offers investors decent income with its dividend yield of 2.5%.

The stock has a Zacks #2 Rank. It trades at 15.8x 2010 consensus EPS estimates and 14.2x 2011 consensus EPS estimates.

Business

Polaris designs, engineers, and manufactures off-road vehicles including all terrain vehicles, snowmobiles, and motorcycles. The company also provides replacement parts and accessories.

Strong Second-Quarter Results

On July 20, Polaris reported revenue of $430.9 million, up 25% year-over-year. The company earned $0.76 per share, an increase of 43.4% over the year-ago quarter. More importantly, Polaris beat the Zacks Consensus Estimate by 9 cents, or 13.4%.

PII has now beaten the Zacks Consensus for the last five quarters by an average 14.1%.

Polaris increased its sales and earnings guidance for 2010. Management now expects sales growth of 17%-20%, and EPS of $3.80-$3.90. That’s up from its previous guidance of 8%-11% sales growth and EPS of $3.48-$3.60.

The company’s strong quarterly results were driven by market share gains across most of its product lines.

Estimates

The company’s strong second-quarter results prompted analysts to raise their estimates for 2010 and 2011. In the last week, the Zacks Consensus Estimate for 2010 rose 27 cents, or 7.4%, to $3.90. The Zacks Consensus Estimate for 2011 increased 24 cents, or 5.9%, to $4.33.

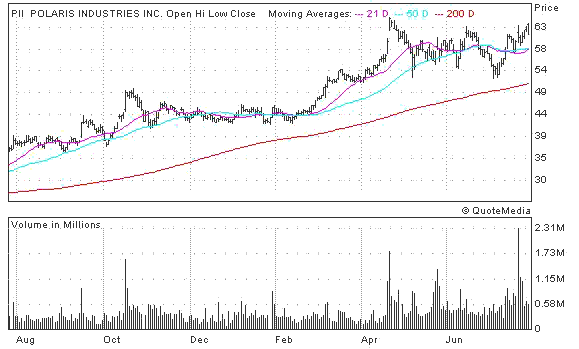

The Chart

During the recent market correction, PII shares sold-off about 19% from its April highs. In the last three weeks, however, the stock has rebounded nicely. It is looks set to make a run at new highs.

Leave a Reply