At first blush, the second quarter statistics from the Job Openings and Labor Turnover Survey (commonly referred to as JOLTS and released Tuesday by the U.S. Bureau of Labor Statistics) suggest little has changed recently in U.S. labor markets:

“There were 3.2 million job openings on the last business day of May 2010, the U.S. Bureau of Labor Statistics reported today. The job openings rate was little changed over the month at 2.4 percent. The hires rate (3.4 percent) was little changed and the separations rate (3.1 percent) was unchanged.”

Despite a slight step backward in May, the overall trend in job openings has been positive—Calculated Risk has the picture—but in a sense this fact has just deepened the puzzle of why the unemployment rate is so darn high. As we wrote in the first quarter issue of the Atlanta Fed’s EconSouth:

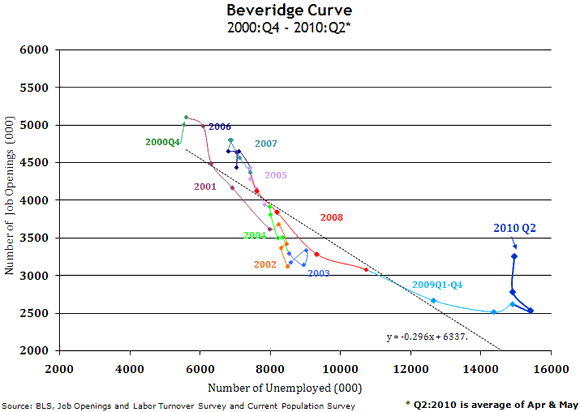

“The disconnect between the supply of and demand for workers that is reflected in statistics such as the unemployment rate, the hiring rate, and the layoff rate can be dynamically expressed by the Beveridge curve. Named after British economist William Beveridge, the curve is a graphical representation of the relationship between unemployment (from the BLS’;s household survey) and job vacancies, reflected here through the JOLTS.”

Since the second quarter of last year, the unemployment rate has far exceeded the level that would be predicted by the average correlation between unemployment and job vacancies over the past decade. Yesterday’;s report indicates that the anomaly only deepened in the first two months of the second quarter.

The dashed line in the chart above, which is estimated from the data from 2000–08, represents the predicted relationship between the number of unemployed persons in the United States and the number of job openings. That simple relationship would suggest that, given the average number of job openings in April and May, the unemployed would be expected to number about 10.4 million—not the nearly 15 million we actually saw.

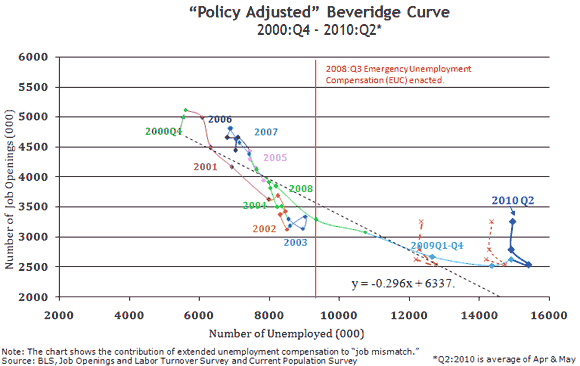

Some analysts have suggested the unemployment benefits policies of the last couple of years may be responsible for abnormally high unemployment rates. Estimates generated by several researchers in the Federal Reserve—here and here, for example—suggest that extended unemployment benefits may have increased the unemployment rate by somewhere between 0.4 and 1.7 percentage points. But even if we accept those numbers and adjust the Beveridge curve by assuming that the number of unemployed would be correspondingly lower without the benefits policy, it’s not clear that the puzzle is resolved:

If you tend to believe the higher end of the benefits-bias estimates, no puzzle emerges until the second quarter of 2010. And, of course, some estimates apparently deliver an even larger impact of the extended benefits policy. Let’s call the question unsettled at this point.

The most tempting explanation for the seeming shift in the Beveridge curve relationship (to me, anyway) is a problem with the mismatch between skills required in the jobs that are available and skills possessed by the pool of workers available to take those jobs. The problem with this tempting explanation is that it is not so clear that the usual sort of structural shifts we might point to—for example, only nursing jobs being available to laid-off construction workers—are so obviously an explanation (an issue we explored in a previous macroblog post).

But these sorts of subplots may miss the truly big part of the story. I have noticed a recent spate of articles repeating a theme we hear anecdotally from many sources, in many industries. For example, this from a June USA Today article…

“… the [auto] industry is poised to add up to 15,000 this year and could need up to 100,000 new workers a year from 2011 through 2013.

“… Automakers need workers with more and different skills than in the past on the factory floor.… Among priorities: computer skills and the ability to work with less supervision than their predecessors. That likely means education beyond high school.”

… or more recently, this one from the New York Times:

“Factory owners have been adding jobs slowly but steadily since the beginning of the year, giving a lift to the fragile economic recovery…

“Yet some of these employers complain that they cannot fill their openings.

“Plenty of people are applying for the jobs. The problem, the companies say, is a mismatch between the kind of skilled workers needed and the ranks of the unemployed.”

Now I realize that a few anecdotes don’;t make facts, but I have been in more than a few conversations with businesspeople who have claimed that the productivity gains realized in the United States throughout the recession and early recovery reflect upgrades in business processes—bundled with a necessary upgrade in the skill set of the workers who will implement those processes. This dynamic suggests that the shift in required skills has been concentrated within individual industries and businesses, not across sectors or geographic areas that would be captured by our most straightforward measures of structural change.

The data necessary to test this proposition are not easy to come by. That challenge is unfortunate, because the return on figuring out what is beneath those Beveridge curve graphs is very high.

Leave a Reply