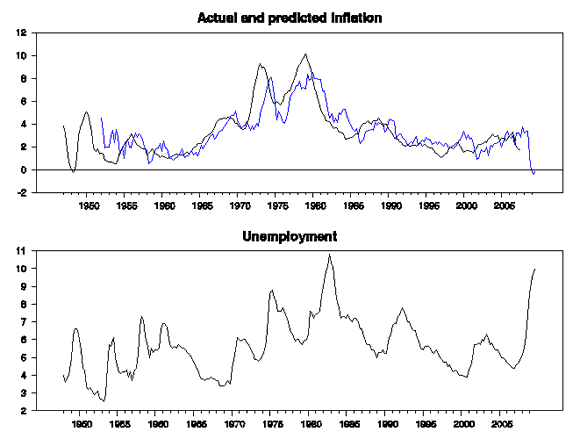

With unemployment likely to stay near 10% for the next year, it is hard to imagine wage inflation returning any time soon. In October I illustrated a simple Phillips curve relation that could be used to forecast the inflation rate over the next two years as a function of the realized inflation rate over the previous five years along with the current unemployment rate. The figure below updates that forecast using the December unemployment numbers. The relation is still calling for deflation, not inflation, over the next two years.

Top panel: Black line is the value of subsequent average 2-year inflation rate (πt+8) corresponding to each indicated date t Blue line is the predicted value from the dynamic regression for each indicated date t. Bottom panel: unemployment rate as of last month of indicated quarter t.

Downward pressure on rents is another factor that makes a surge in the large owner-equivalent-rent component of the CPI unlikely. Why then would anybody expect an immediate resurgence of inflation?

Greg Mankiw offers this analysis:

One basic lesson of economics is that prices rise when the government creates an excessive amount of money. In other words, inflation occurs when too much money is chasing too few goods. A second lesson is that governments resort to rapid monetary growth because they face fiscal problems. When government spending exceeds tax collection, policy makers sometimes turn to their central banks, which essentially print money to cover the budget shortfall….

The federal government’s budget deficit was $390 billion in the first quarter of fiscal 2010, or about 11 percent of gross domestic product. Such a large deficit was unimaginable just a few years ago. The Federal Reserve has also been rapidly creating money. The monetary base– meaning currency plus bank reserves– is the money-supply measure that the Fed controls most directly. That figure has more than doubled over the last two years. Yet, despite having the two classic ingredients for high inflation, the United States has experienced only benign price increases….What gives?

Part of the answer is that while we have large budget deficits and rapid money growth, one isn’t causing the other. Ben S. Bernanke, the Fed chairman, has been printing money not to finance President Obama’s spending but to rescue the financial system and prop up a weak economy.

I see this last issue a little differently from Greg. I would emphasize that there are a number of components that could contribute to future fiscal deficits. These include not just the standard concerns about whether taxes will be raised sufficiently to cover growing entitlements– and that by itself is of course a huge issue— but also prospective expenditures needed to make good on the government’s guarantees of the obligations of institutions such as Fannie, Freddie, and the FDIC, whose notional commitments exceed the entire federal debt held by the public. The business of making such loan guarantees is by its nature a decision of fiscal as opposed to monetary policy. But having the Fed absorb credit risks that private actors will not is the essence of the new monetary policy adopted by the Federal Reserve over the last year and a half. I furthermore am persuaded that the Fed assumed these obligations precisely because the U.S. Congress was unwilling to authorize such actions as an explicit fiscal act. As I wrote in my contribution to the recent book, The Road Ahead for the Fed:

If I were the chair of the Federal Reserve, I would want to be asking, “why was I invited to this party?” The answer unfortunately appears to be, “because you’re the one with the deep pockets.” That the Fed should find itself in a position where Congress and the White House are viewing its ability to print money as an asset to fund initiatives they otherwise couldn’t afford is something that should give pause to any self-respecting central banker.

Greg Mankiw’s source of reassurance is thus the cause of my personal anxiety. I think the separation between monetary and fiscal policy has become increasingly blurred. I maintain that the keys to preventing a resurgence of inflation in the U.S. are (1) credible and responsible commitment from Congress that it is not going to allow the debt-to-GDP ratio to continue to balloon over the next decade, and (2) a return of the Federal Reserve to a primary focus on controlling the money supply rather than trying to target particular yield spreads.

And what about the monetary expansion we’ve seen already? Here is Greg’s analysis:

As the economy recovers, banks may start lending out some of their hoards of reserves. That could lead to faster growth in broader money-supply measures and, eventually, to substantial inflation. But the Fed has the tools it needs to prevent that outcome.

For one, it can sell the large portfolio of mortgage-backed securities and other assets it has accumulated over the last couple of years. When the private purchasers of those assets paid up, they would drain reserves from the banking system.

And as a result of legislative changes in October 2008, the Fed has a new tool: it can pay interest on reserves. With short-term interest rates currently near zero, this tool has been largely irrelevant. But as the economy recovers and interest rates rise, the Fed can increase the interest rate it pays banks to hold reserves as well.

Here again I differ from Greg. I see no conceptual distinction between short-term T-bills issued by the Treasury and interest-bearing reserves created by the Fed. Both represent liabilities from the government that must be repaid with interest. The Treasury should not assume it can always roll over an increasing volume of debt simply by issuing more debt, nor should the Fed assume that it can always persuade banks to continue to hold a trillion dollars in excess reserves simply by exercising its one true power– the ability to print more money. The value of the new Federal Reserve liabilities ultimately will be determined by the long-term fiscal soundness of the U.S. government.

Let me nevertheless again emphasize that I don’t see these dynamics playing out in the form of a near-term surge in inflation, for the reasons I spelled out in the beginning. Inflation is not something you should be afraid of for 2010. But what we need is a convincing commitment from the government to both near-term stimulus and longer-term fiscal responsibility in order to be assured that it’s not a concern over the next decade.

And that’s not what I’m seeing from the U.S. Congress.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply