Since it is the Christmas holiday, and I am spending the week in southern Spain with my family, I have not been focusing too heavily on economic data and have instead been reading lots of different stuff, including Frederic Wakeman´s excellent The Fall of Imperial China, about the transition from the Qing, especially the late Qing, to the early Republic. Among other things I have been reading there is a very interesting article in the Winter 2010 edition of National Affairs, by Jim Manzi, and AI entrepreneur and senior fellow at the Manhattan Institute, that discusses the US within what he calls “the inherent conflict between the creative destruction involved in free-market capitalism and the innate human propensity to avoid risk and change.”

This has some relevance to China’s long-term economic and social prospects, and is a topic that I have discussed a lot with my students. In fact it is almost a subtext in Frederic Wakeman´s book. To put it simply, one of the great strengths of the US is its ability to change quickly and dramatically, even though this ability necessarily comes with a sometimes brutal insensitivity to the short-term social costs of the change. As Manzi puts it,

An economy built upon constant and relatively free innovation is inherently difficult to sustain in a democracy. This is not so much a matter of anti-market ideology as of the painful realities of economic change. Innovation forces change, and the pain involved tends to be felt immediately while the benefits are usually diffuse and harder to perceive in the short term.

It is therefore natural for people to organize to prevent the spread of significant innovation. The original Luddites were cotton weavers who, in the throes of Britain’s Industrial Revolution, responded to their displacement by automated weaving technology directly: They smashed looms. In America, people in similar situations rarely assault property en masse, but they do form political coalitions to pass laws that restrict innovation. It is understandable that the enormous waves of innovation always sweeping over a dynamic free-market economy will arouse great unease and opposition. But for that economy to prosper, the unease and opposition must be overcome.

A big question for me is how China decides in the future to face the continuing trade-off between social stability and rapid change. In the past it is pretty clear that China has experienced wrenching social change. This change began from a widespread recognition during the 1970s that the Chinese model simply was not working, and that without a dramatic transformation, China was likely to collapse. It took the brilliance of Deng Xiaoping to understand how to steer China forward without risking an even worse crisis, and the economic rewards for this transformation have been dramatic, even as the social cost of such rapid change has put increasing pressure on the political and social systems of the country. How is China likely to face the continuing trade-off in the future?

This is not just an abstract and very macro question. It addresses much more specific things such as the liquidation process following a financial crisis. For example, if we were to see a break in the housing bubble, there are broadly speaking two ways to address the problem. The so-called “Anglo-Saxon” model would involve a rapid liquidation of loans, the seizing and selling of collateral, and bankruptcies. The advantage of this model is that assets are quickly re-priced and allocated to their most profitable or efficient uses.

Assets that are non-viable at their original costs, in other words, are marked down and returned to the economy, and very often the new users engage in rapid innovation and the creation of new industries. One obvious example is the massive railroad bankruptcies that occurred in the US after 1873. The railroads were liquidated and purchased by new investors at steep discounts, allowing them to cut freight costs sharply, thereby spurring a whole series of new industries, most famously, I think, the mail-order retail business. More recently the collapse of the broadband suppliers and the subsequent drop in internet costs permitted the existence of Amazon.com, Ebay, Google and a host of other new technology companies.

But there is a cost. Liquidation can be brutal – businesses close down, land and assets are seized, workers lose jobs, families are forced to leave their homes, and so on. Americans, for whatever reason, have been more tolerant than many other societies of these kinds of disruptions, perhaps because of a combination of innate optimism and a robust political framework that absorbs some of the costs and anger. Other societies are less so.

The second way, broadly speaking, that the break in the housing bubble might occur, and without the brutal social adjustments, is what has sometimes been called the “Japanese” model. Rather than force bankruptcies and rapid liquidation, borrowers would be permitted easily to roll over their loans, financing costs would be kept low (at savers’ expense of course), and excess inventory taken off the market. The disadvantage of this kind of process is that assets are very slowly reallocated – sometimes after many years – to more efficient uses, and those assets taken off the market become a pure dead-weight to the economy. In addition the need to keep financing costs low, so as to delay recognition of the losses, hampers future growth by encouraging continued misallocation of capital and slowing the development of domestic consumption by forcing households to bear most of the cost of the adjustment via low interest rates on their savings. The advantage, of course, is that it much less socially disruptive and painful.

When I discuss this with my students at Peking University their responses, not surprisingly, vary. A number of them insist that Chinese have learned long ago to suffer disruption, and they will be forced to continue absorbing the costs of change since there is a widespread consensus among the leadership that China must continue in its forward rush. Others, the majority, think that although socially the Chinese are used to absorbing the cost of rapid social change, the political system itself is less able to do so. Most interestingly to me is that whenever we have these discussions it becomes pretty clear to me that for most of my students our discussions are not the first time they have thought of this or related issues. This is something that many students, at least within the elite schools, have thought about.

This discussion extends into the whole issue of financial reform, and not just for China. Financial crises are usually the way a distorted system rebalances, and although they are often necessary in the long run, they can obviously be painful in the short. Needless to say there is nothing like a financial crisis to bring out calls for the reform of the financial system, but I think we should be very cautious about what kinds of reform we ask for. The recent financial crisis, which seemed most to affect “Anglo-Saxon” financial systems, have brought out, predictably enough, fervent warnings about the riskiness of deregulated and fragmented financial systems, along with a pride of proposals for reform, many of which aim to prod and force financial systems into more rigid and constrained forms.

But we risk, as always, drawing the wrong lessons from the crisis, and confusing the triggers with the underlying causes of the crisis. Every major financial financial crisis in history was preceded by a massive liquidity build-up. which the financial sector was forced to accommodate, as it always does, by taking on too much risk. Hyman Minsky, and his disciples like Charles Kindleberg, describe this process vividly, with banks and other entities taking on too much risk as a function of excess liquidity and excessively low costs of capital. It doesn’t matter if the system is highly fragmented and deregulated or highly regulated and monolithic. After all a large part of the prestige of the “Anglo-Saxon” model derives from the spectacular collapse of its antithesis, the Japanese model of the 1980s, which seemed — mistakenly again — to prove the superiority of deregulated systems, with their breakneck innovation, over highly regulated and very rigid systems.

So which is it that can best prevent crisis and the associated economic costs — the very open systems or the very rigid systems? Neither, it turns out. All of them react more or less the same way to excessive liquidity and too-cheap capital — by taking on too much risk, whether in the form of complex derivatives and securitizations, in the case of the former, or in the form of very old fashioned collateralized loans, in the case of the latter.

So is there no room for financial sector reform? Of course there is, but the purpose of reform should not be to allow us to turn from the crisis and proclaim “Never again!” That is silly. It will happen again and again and again. Instead, the purpose of regulation should be to ensure that the financial system does a better job of allocating capital during “normal” periods. A financial system designed to minimize the risks of crisis is probably a waste of time. It should be designed to create the best mix of risk capital and safety consistent with a rapidly growing economy over the long run. Periodic financial crises are a necessary evil, and there is little we can do about them except try to create automatic structures (counter-cyclical in national balance sheets, as Mnsky argued) that minimize their transmissions into the real economy. So in China’s case, contrary to breathless advice by press and experts, the US financial crisis teaches almost nothing about how to manage financial sector risk. It neither proves nor disproves the usefulness of a highly deregulated and innovative financial system. China´s financial sector issues are different. China´s systematic misallocation of capital is its biggest financial problem. China needs serious governance reform and interest rate liberalization so that capital can flow to the most dynamic parts of the economy and be made available to risk-taking entrepreneurs in a way the fosters productivity growth. It needs capital to be correctly valued so that it is not wasted on creating overcapacity, asset market bubbles, and trophy projects, all of which detract from future consumption growth. But no matter how well-designed it is, the regulators should have a plan for the inevitable crisis, because it will come. The interesting question is not how China can avoid problems, but rather how it should deal with them when they come.

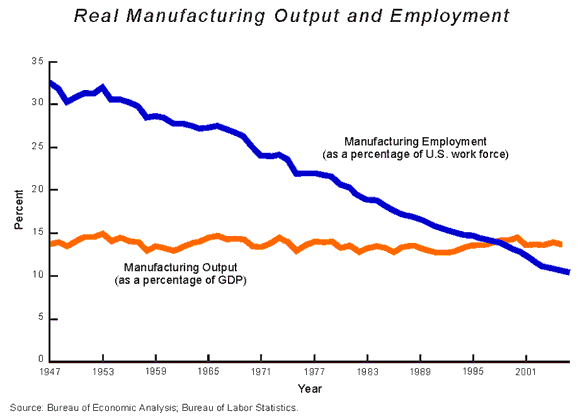

There was something else I thought was interesting in Manzi’s article discussed at the beginning of this entry. The graph below reproduces data about the recent history of manufacturing in the US. One of the claims that has been repeated so often that it has become true merely by virtue of repetition is that the US is losing its status as a great manufacturing power. The US used to make real “stuff”, according to this argument, but now it no longer does so. What this graph shows is that this claim is at best exaggerated, and almost certainly wrong.

The huge (and hugely disruptive) surge in manufacturing productivity in the last sixty years has dramatically reduced the share of American workers employed in manufacturing, but manufacturing’s share of GDP has barely budged.

The decline in US manufacturing labor has created a sense of crisis in manufacturing, but it mostly means that labor productivity has risen sharply. That is unquestionably a good thing. Unfortunately fears about US manufacturing decline have, unnecessarily I think, complicated discussions about China´s rise in the US, and created more worry then is merited. China´s growth is not hollowing out US manufacturing. There are certainly problems with imbalances that need to be addressed, but they need to be addressed rationally with a clear understanding of the difficult issues each country faces within the relationship.

By the way, and on a different subject, for those who are interested in demographics, the US Census Bureau released its latest projections. According to the release:

China’s population is projected to peak at slightly less than 1.4 billion in 2026, both earlier and at a lower level than previously projected. Meanwhile, India’s population is projected to surpass China’s population in 2025, according to new data being released by the U.S. Census Bureau. These figures come from the population estimates and projections for 227 countries and areas released today through the Census Bureau’s International Data Base. This release includes revisions for 21 countries, including China.

The latest projections indicate that by 2026, the population of China will begin to decline. Population growth in China, the world’s most populous country, is slowing and currently stands at 0.5 percent annually. China surpassed the 1.2 billion population mark in 1994 and reached 1.3 billion in 2006. According to the latest revisions, India is projected to become the world’s most populous country in 2025. The population growth rate in India currently is about 1.4 percent, nearly three times that of China. The difference in the growth rate between the two countries is explained by fertility. India’s total fertility rate — the number of births a woman is expected to have in her lifetime — is currently estimated at 2.7 and projected to decline slowly, and that is driving population growth in the country.

The slowdown in China’s population growth is the result of declining fertility. China’s total fertility rate is estimated to have been 2.2 in 1990, 1.8 in 1995 and less than 1.6 since 2000. China’s fertility rate is currently half a birth below that of the United States, which is more than two births per woman. Key evidence for the new fertility estimates comes from analysis of data from China’s recent census and surveys. One of the consequences to China’s declining fertility rate is that the number of new entrants to China’s labor force may be near its peak. The population ages 20-24 is projected to peak at 124 million in 2010. This peak is earlier than in India, which is projected to reach 116 million in 2024.

Despite a shrinking younger population, China’s labor force may continue to grow for several years since the population ages 20 to 59 (prime working ages) is not expected to peak until 2016 at 831 million, an increase of 24 million from the current estimated level. “These changes in China’s age structure may affect its economic growth and competitiveness in the world market,” said Daniel Goodkind, demographer in the Census Bureau’s Population Division. Given that China and India together account for 37 percent of the world’s population, their demographic trends have major implications for worldwide population change. The Census Bureau’s International Data Base includes projections by sex and age to 100-plus for 227 countries and other areas with populations of 5,000 or more and provides information on population size and growth, mortality, fertility and net migration.

So much for 2009. In two days I return to Beijing in time for the crazy end-of-year festivities at D22. I wish you all a great 2010.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply