I’ve been discussing possible explanations for the recent tendency of the dollar prices of commodities to move together. On Friday we received a very useful data point for distinguishing between the different hypotheses.

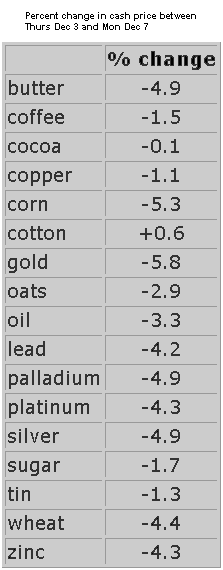

One possible explanation for the resurgence of commodity prices since January is the strengthening world economy, particularly outside the United States. But if that is what’s been going on, we should have seen further moves up on Friday, when the U.S. released a key employment report that was far stronger than most of us had anticipated. Whatever you believed about near-term world economic growth on Thursday, on Friday you should have become more optimistic than you’d been on Thursday. But what happened in commodity markets on Friday? The dollar price of almost everything fell quite dramatically.

One possible explanation for the resurgence of commodity prices since January is the strengthening world economy, particularly outside the United States. But if that is what’s been going on, we should have seen further moves up on Friday, when the U.S. released a key employment report that was far stronger than most of us had anticipated. Whatever you believed about near-term world economic growth on Thursday, on Friday you should have become more optimistic than you’d been on Thursday. But what happened in commodity markets on Friday? The dollar price of almost everything fell quite dramatically.

Others have suggested that inflation fears may be part of the commodity price picture. But if inflation expectations are subsiding as a result of a resumption in U.S. employment growth, it would be a very different account of inflation than the kinds of Phillips Curve specifications popular with the Federal Reserve.

Perhaps one could tell an inflation-expectations story based on fears about long-run fiscal solvency. Economic growth is the biggest single factor that could help the U.S. dig out of its deficit hole, and so maybe you’d be a little less concerned about a dollar crisis today than you would have been last week. I note for example this report:

Moody’s is looking at the debt of both the US and UK and does not like what it sees, according to recent data from the credit agency…. The rating of US debt will obviously be based on whether the economy rebounds enough so that the government can cut spending and the size of the national debt no longer grows at break neck speed.

A more natural interpretation of Friday’s commodity price moves would be based on the role of low short-term interest rates in encouraging the commodity price boom. The sooner U.S. employment recovers, the sooner the Fed will start raising interest rates, and the sooner the game of putting borrowed cash into commodities would be up. For example, the implied fed funds rate on the September 2010 futures contract went from 0.5% on Thursday to 0.6% on Friday, consistent with the claim that interest rates have been an important factor in recent commodity price movements.

The Fed is accustomed to thinking of unemployment as the key predictor of inflation, and of relative commodity prices as a separate factor beyond its direct control. I read Friday’s market moves as one more suggestion that commodity price inflation may have more to do with U.S. monetary policy, and less to do with U.S. employment, than many within the Fed are prepared to acknowledge.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply