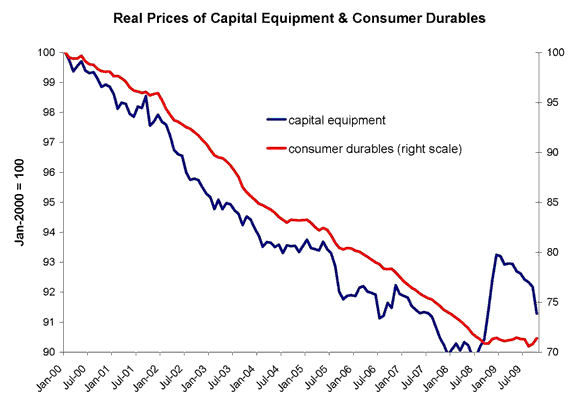

The graph below shows monthly price indices for capital equipment and consumer durables, though Oct 2009.

Economists know well that these goods have steady gotten cheaper over time. The mystery to me is that, beginning last September, they stopped getting cheaper and even got more expensive (note that the consumer durable price is on a different scale — it has tended to decline a lot over time — so the lack of decline is more remarkable there).

While you try to solve the mystery, please note:

1. volumes produced of these goods are obviously down, but that has been true in previous (ITC-less) recessions and those recessions did not have such price increases (note that my graph includes the 2001 recession). So I don’t think the high prices can be blamed on the low volumes alone.

2. For some items, one might be concerned that the price indices are based on “list prices” and those list prices have (perhaps) been discounted more heavily than usual. I am dubious of a significant “list price” bias because the increases are across broad categories of consumer durable goods, including things like cars, college textbooks, jewelry, and telephones where this bias is either less of an issue OR the BLS is measuring actual transaction prices by acting as would-be purchasers themselves).

3. Also note that most of the measured sub-index increases are nominal — I doubt that manufacturers sought to discount their goods by first hiking their list prices.

The ITC is known as the “Investment Tax Credit” — a credit going to the purchaser of a new durable good. The federal government used it in some of the 1960s and 1970s recessions, but not in the 1980s and 1990s. Professor Goolsbee has convincingly shown that the short run effect of the ITC is to make durables goods more expensive, rather than encouraging investment in them.

“Cash for Clunkers” was a kind of ITC — a subsidy going to purchases of new cars.

I have warned for a while now that investors may be rationally expecting further ITCs.

I raise all of this because the expectation of future ITCs may explain the price pattern in the chart: producers of durable goods are holding back production until those credits are in place?

Anyway, the point of this post is to hear your ideas, not to insist on the ITC interpretation.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply