“Obama, Pelosi and Reid are drafting a new stimulus bill that White House says could have twice the number of non-existent jobs as the last jobs bill.” – Jay Leno

Mother Market has built in a sharp V-shaped recovery (to justify current price levels, the P/Es need robust earnings in 2010). In the Great Depression we never had negative earnings across the whole index, but we did last year. US industry has now cut costs enough that in Q3 earnings have exceeded expecations on lousy revenues. To keep this up, we now need growth. The amount of growth requires a V shaped recovery – a sharp rise next year of at least 5%.

Today’s downgrade of Q3 GDP from 3.5% annualized to 2.8% raises the spectre of a slower U-shaped or a jobless L-shaped recovery, yet the market barely reacted.

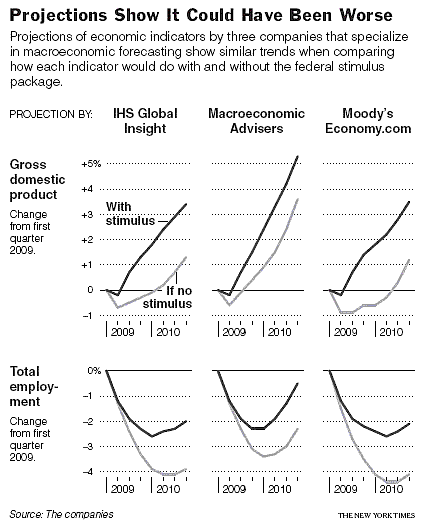

The NYT ran a piece on the recovery, and provided this first chart showing projections of some economics firms. Of course, this sort of thing has about the same predictiveness of the embarrassing unemployment projections of Obama with and without the stimulus. I assume the NYT dropped this in as part of a broader campaign to justify a new stimulus, since it is supposed to show how much worse we would be if there had been no stimulus. After the JobsGate scandal of ludicrous claims of how many jobs were saved or created by the stimulus, a new stimulus will need better support than this. (How much we should accept Moody’s analysis is also unclear, given how badly they did their ratings job during the bubble. This may be another example of feeding results to an audience that will pay for positive predictions.) Nonetheless it supports the conventional wisdom, which has been summarized on Bloomberg TV as “70% expect a V.”

When I scan the pundit-sphere, I grow concerned of a confirmatory bias in their predictions. Those who bash Obama see the U; those who gush see the V. More perverse, those who want a big jobs bill push the L to justify more stimulus (Krugman? Krugman?).

Yet it seems Mother Market still sees a V, at least in the short run. It could just as well become a W, a double-dip, in the long run. Let’s see if we can support the V, and estimate when it becomes a W.

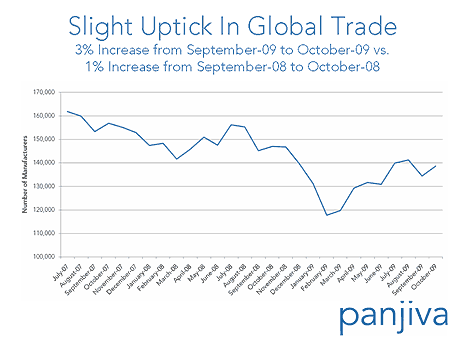

Some economic news shows recovery. Global trade has ticked up (see chart). The much watched Baltic Dry has shown a rise in rates (possibly because so much container capacity has been mothballed). Trucking fell slightly in Oct, but has been on an uptick. Rail data shows a bottoming but hasn’t ticked up much yet.

Charts of US GDP show a V, even with the reduction to 2.8% annualized, from a bad Q1 at -5.7% (this is a revision up from prior reports). Although holiday shopping surveys say watch out for Q4, they also suggest a flat to slightly up season, year on year. So far this week has started up, boding well for Black Friday. Surveys also indicate that this season will be late and value-driven, meaning people will wait for sales, so there may be upside surprise come the day after Xmas.

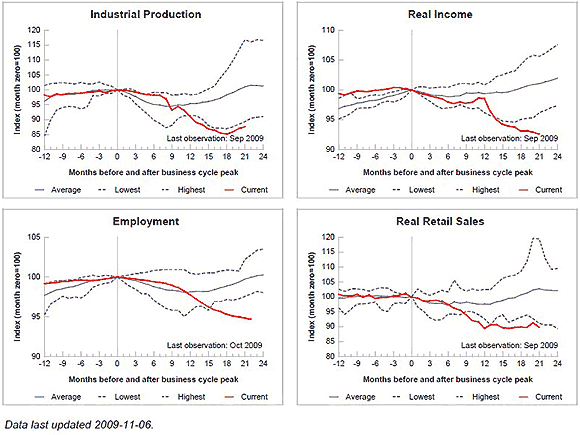

Some data is mixed. These four charts show various US indicators (as of Sept.) that are bottoming or have bottomed. The LEI has been in a V up for months, and continued up in October. ECRI also expects continued recovery despite a weekly blip down last week. Of most interest is industrial production, which is ticking up. Unfortunately, the Oct results were poor, with industrial production growth slowing to 0.1%, a four month low increase, and housing starts a six-month low. The industrial production flatness is lively a hangover of cash4clunkers plus prior inventory rebuilding, hence more likely a pause before an increase, not a change of trend.

One of the odd side consequences of C4C was an increase in imports of autos. The GDP revision down was partly due to this (more imports lowers GDP). Northern Trust expects a drop of such imports in Q4, which will lift GDP.

My conclusion is that Q4 will beat expectations, and will beat Q3, perhaps even get to 4%. After the revision today, expectations faded from a 3.3% range down to a piss poor L shaped pace:

Economists see the economy growing at a pace just above its long-term trend. They expect GDP to grow 2.5% in the fourth quarter, 3% in the first quarter of 2010 and 3.5% in the second quarter. That’s a far cry from the 6% growth seen in typical V-shaped recoveries, but it’s better than a poke in the eye with a sharp stick.

These expectations will likely meander upwards as retail data comes in, albeit it will largely be later than past history and driven by promotions and discounts. This should not surprise, since we are in a New Normal where past patterns do not predict behavior; yet it will likely fool the pundits and forecasters until the data pikes in.

Hence I expect a V-like recovery for several quarters out.

The problem is what happens after. This recovery is largely an artifact of government stimulus and gimmicks like C4C and the first time home buyer credit. We need to see the real economy begin to emerge. On this score things are troubling.

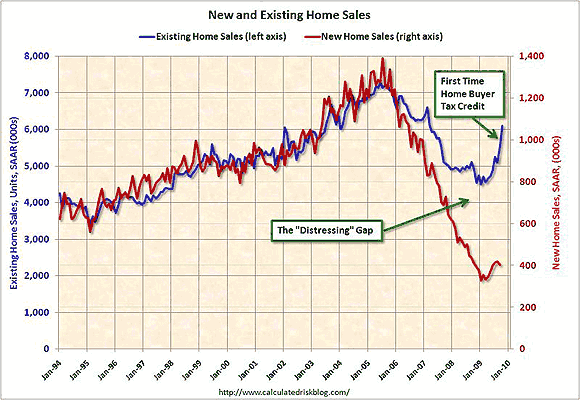

Real estate normally leads out of a recession. Not existing home sales, but new home construction, which drives growth across many sectors of the economy (new house, new appliances, new furnishings, etc.). Despite the big Oct jump in existing home sales, new home sales are in the dumpster. This chart from CalculatedRisk shows how dramatic the gap is. A slight uptrend over the summer is now fading in the winter.

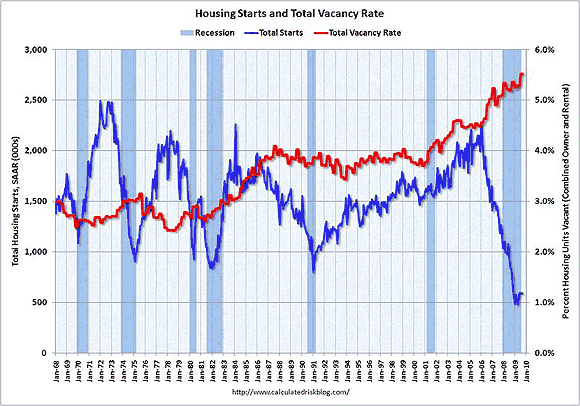

It may be too much to expect a large shift to new homes until the massive overhang of existing homes is worked off. The second chart compares vacancy rates to new home sales. Another huge gap.

Private Investment is a second driver of growth, and is reflected in bank lending to business. There are lots of charts showing a simple reality: banks are still cutting back on loans to business. Until that changes the private economy will be moribund and the V will be largely a concoction of government stimulus.

Stimulus will turn relatively negative late next year, and worse in 2011 when the expiration of the Bush tax cuts turns into a large tax increase. The impact of real estate and private investment does not seem likely to change appreciably in the first half of 2010. Hence we may see the start of the W in 2H10.

The negative effects of diminished stimulus can be seen in this Goldman Sachs analysis of why we won’t have a V, at least not past the first half of 2010:

Despite the sharp pickup in real GDP growth since the dark days of early 2009, we estimate that real final demand—net of the boost from fiscal policy—is still contracting at an annual rate of around 1% in the second half of 2009. Although we expect a moderate recovery of around 2% by the second half of 2010, such a 3-percentage-point improvement would be insufficient to offset the loss of 4-5 percentage points of stimulus from fiscal policy and the inventory cycle. Hence, real GDP growth is likely to slow anew to a below-trend pace.

Their chart shows we were in Peak Stimulus in Q3, a point I made several months ago, and with inventory rebuilding adding to a peak overall stimulus in Q4.

Hooverism may be the ironic response of Obama. He has already proffered a dangerous thought, that deficits could cause a double dip recession. (Krugman’s response: “What? Huh?”) He may push for accelerating the end of Bush tax cuts, replicating one of the huge mistakes of Hoover, to push for a tax increase in 1932 to help balance the budget. We had been coming out of the Depression, and promptly sunk back in. Something similar happened again in 1937.

There is one rule of Recession Club: you don’t raise taxes in recessions.

Obama has also begun the siren song of yet another stimulus, now a “jobs bill,” a belated recognition of how awful his Porkulus first Stimulus was. I suppose if he were to retarget existing stimulus and the remaining TARP money and avoid increasing the deficit, he might be able to help extend the period of government life support to prop up the economy and push off the W.

All of this will be tragically ironic, because he will be hoist by the petard of Keynesian economic revisionism that Hoover was laisse faire and did nothing, and FDR did something to get us out of the Depression. The victors rewrite history, and the post-war economic writers like Samuelson sure did a number on Hoover.

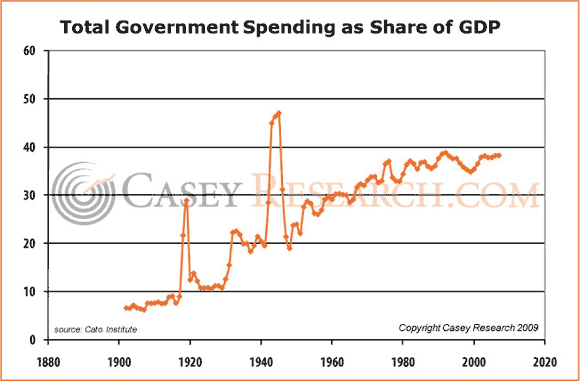

Look at the chart of Federal debt vs GDP. Hoover ramped it up, and FDR sustained that level until WWII. It was Hoover who first tried a massive stimulus to boost the economy, running up spending to 20% of GDP in his final two budgets (FY32 and FY33). FDR did not do a Krugman-like stimulus beyond what Hoover had already done, and indeed when he met Keynes in 1936 it was reported as a poor meeting. Rather than follow Keynes, one could say FDR followed Hoover. Heresy I know, but historically closer to the truth. How will history rank Obama, who so far has largely followed the path Bush first set?

Obama would do better to drop his progressive causes (climate change, healthcare reform and social justice) and first fix the financial sector (real estate, business loans, consumer credit) to get the private economy back on its feet. But it appears he would rather drive us off a cliff, albeit inadvertently through is apparent economic illiteracy.

All of this is why I say to embrace the W. Expect the V over the next few quarters, and watch how misguided government policies throw us back down again.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply