We are embarking once again into that time of the year when reporters around the world become entranced and enthralled with that orgy of consumerism that defines Christmas in America. Soon we will be tracking the ups and downs of holiday sales with a zeal that is unmatched by any other regular economic event. Weary reporters – those who clearly disappointed their editors at some point during the year – will be dispatched to local big box stores across the nation to record the lines forming in anticipation of 5am openings on the fabled Black Friday. We will be bombarded with hundreds if not thousands of conflicting reports regarding the amount and patterns of holiday shopping, leaving overworked and underpaid analysts awash in data as they desperately try to quantify, once and for all, the “true” state of consumer spending – and thus by extension, the true state of the economy – in America.

Oooo, how I have come to loathe this exercise. And yet, here I am again, fretting over the financial state of US households in between checking off items on the Thanksgiving shopping list. It is like a car wreck – you don’t want to watch, but you can’t take your eyes off it.

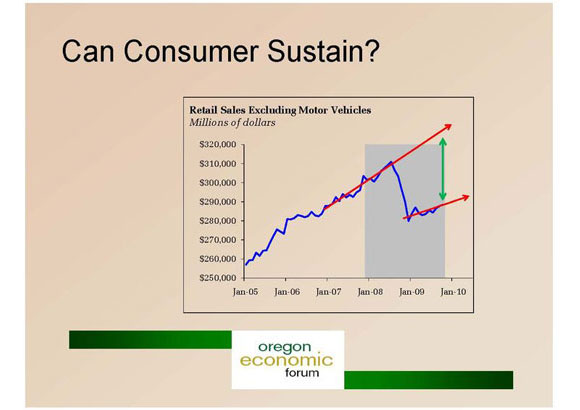

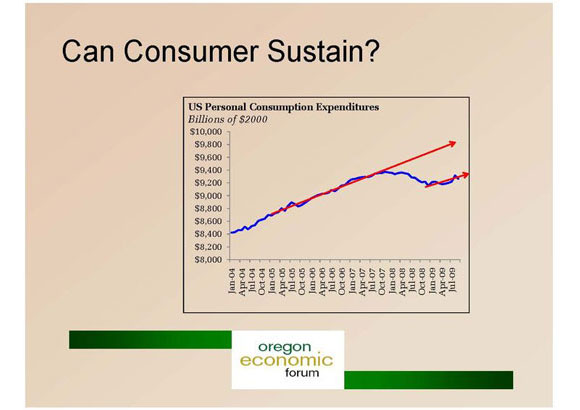

Car wreck is something of an appropriate comparison. Recently I have begun using charts of this sort to depict the current economic environment:

Not fancy econometrics, I know – most of my audiences are not interested in unit root tests. The point, obviously, is that even as activity creeps upward, the gap between the past and current trajectory of consumer spending is likely still widening. Much, much faster growth is necessary to close that gap. And households as of yet are seeing nothing to convince them their fortunes are set to change, that some Christmas miracle awaits. To be sure, Bloomberg trumpeted today’s data:

Confidence among U.S. consumers unexpectedly rose in November as a brightening outlook masked growing concern over joblessness.

How much did the outlook brighten? The story continues:

The Conference Board’s confidence index increased to 49.5 from 48.7 the prior month. The New York-based Conference Board’s index, which focuses on the labor market and purchase plans, averaged 58 in 2008 and 103.4 in 2007.

Not much brighter. Indeed, Economix more accurately reports the dismal mood of consumers, noting:

Over the last 30 years, the index has averaged about 95. In November, it was 49.5, up from 48.7 the previous month.

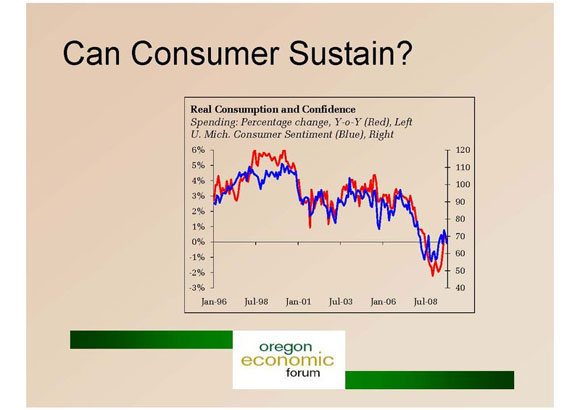

Yes, for three decades the Conference Board measure of confidence has averaged nearly twice current levels. This tells us something about the strength of consumer spending. Using the parallel measure from the University of Michigan:

Real year over year growth in the 1% range is not going to bring households back to trend anytime soon. To be sure, given the dependence of household on debt financed spending, it is arguably correct that past trends were unsustainable, that the only possible outcome from this mess was a permanent shock to the level of household spending. That, however, is likely cold comfort to the millions of Americans – those not employed by Goldman Sachs (GS), of course – who are just now realizing that their standard of living has shifted permanently lower. Lacking sufficient income gains and the ability to use debt to cover up their relative poverty, households are not seeing a path to a brighter future. And they will increasingly look for someone to blame. No wonder the knives are sharpening for Treasury Secretary Timothy Geithner and Federal Reserve Chairman Ben Bernanke. They are the public faces for an Administration that now owns this economy.

And where are policymakers as we slog through the final month of 2009? The Administration is poised to do virtually nothing:

The White House is lukewarm about proposals by congressional Democrats to introduce broad legislation to create jobs, instead favoring targeted measures that would be less likely to inflate the deficit, administration officials said.

There is as yet no agreement within the White House or in Congress on how to try to curb the U.S. jobless rate. But the differences in opinion suggest that rifts could emerge among Democrats as they wrestle with how to beat back the highest unemployment rate in a generation.

…Hamstrung by the nation’s $1.4 trillion deficit and his pledge not to raise taxes on middle-class Americans, Mr. Obama is keen to avoid any measures suggestive of a second, big-ticket stimulus.

Indeed, the failure of the Administration to take bold moves early in the year now cripples it in any attempt to take bold action now. Apparently, the best we can expect now is a “Cash for Caulkers” program that will dribble money into the economy, ensuring that we do little if any better than limp along.

Likewise, monetary policymakers too are caught in the headlights. As has already been widely noted, the minutes of the most recent FOMC meeting reiterated the Fed’s eagerness to reverse, not extend, policy:

…Overall, many participants viewed the risks to their inflation outlooks over the next few quarters as being roughly balanced. Some saw the risks as tilted to the downside in the near term, reflecting the quite elevated level of economic slack and the possibility that inflation expectations could begin to decline in response to the low level of actual inflation. But others felt that risks were tilted to the upside over a longer horizon, because of the possibility that inflation expectations could rise as a result of the public’s concerns about extraordinary monetary policy stimulus and large federal budget deficits. Moreover, these participants noted that banks might seek to reduce appreciably their excess reserves as the economy improves by purchasing securities or by easing credit standards and expanding their lending substantially. Such a development, if not offset by Federal Reserve actions, could give additional impetus to spending and, potentially, to actual and expected inflation. To keep inflation expectations anchored, all participants agreed that it was important for policy to be responsive to changes in the economic outlook and for the Federal Reserve to continue to clearly communicate its ability and intent to begin withdrawing monetary policy accommodation at the appropriate time and pace.

Read that carefully and realize this: An apparently not insignificant portion of the FOMC believes that there is a terrible risk that banks loosen their credit standards and increase lending at a time when, even if the economy posts expected gain, unemployment remains at unacceptably high levels. Silly me, I thought increased lending was the whole point of the exercise to lower interest and expand the balance sheet. That whole credit channel thing. If not to expand lending during a credit crunch, then what else are they expecting?

I am in shock that this sentence made it into the minutes. One can only conclude that a significant portion of policymakers are simply clueless. Or, more disconcerting, they have lost all faith in the ability of financial institutions to channel capital into activities with any hope of financial returns. Has the Fed now embraced the view that they manage the economy through little else then fueling and extinguishing bubbles?

At this juncture, only St. Louis Fed President James Bullard is signaling a willingness to at least keep the option of ongoing balance sheet expansion alive:

Federal Reserve Bank of St. Louis President James Bullard wants the Fed to continue to buy mortgage-backed securities beyond the March 2010 cutoff to give policy makers more flexibility as they seek to shepherd the economy toward recovery.

“I have advocated to keep the asset-purchase program open but at a very low level, and wait and see what happens, and as information comes in about the economy we can adjust that program while the federal-funds rate remains at zero,” Mr. Bullard told Dow Jones Newswires in an interview Sunday. He said “no decision has been made” about the program’s fate.

Mr. Bullard will be a voting member on the interest-rate-setting Federal Open Market Committee in 2010. In its statement after the November FOMC meeting, the central bank reiterated that it will continue to monitor its asset-purchase programs “in light of the evolving economic outlook and conditions in financial markets.”

Maybe if unemployment continues to rise Bullard’s vote will matter next year. Maybe.

Considering what all this means in light of Black Friday, I tend to think Phil Izzo at the Wall Street Journal is on the right path:

New reports Monday didn’t paint an encouraging picture. The Conference Board released a survey of spending intentions that showed U.S. households expect to spend an average of $390 this season, down 7% from estimates of $418 last year. That number is especially distressing because consumers were unusually pessimistic last year as the financial crisis went into full swing just as holiday shopping was getting underway.

“Job losses and uncertainty about the future are making for a very frugal shopper. Retailers will need to be quite creative to entice consumers to spend, both in stores and online this holiday season,” said Lynn Franco, director of the Conference Board Consumer Research Center.

A separate report from retail-tracking firm NPD Group indicated consumers may not be flocking to the mall for Black Friday. Just 32% of respondents said that they expect to begin their holiday shopping on Thanksgiving weekend or earlier.

Still, more broadly, whether sales gain 2% or 4% this holiday season may have great influence on the animal spirits that govern equity markets, I doubt it would alter much what should be our overall assessment of the economy: Economic activity is now increasing, something for which we should all be thankful this weekend. The alternative would be very unpleasant. But that growth should not lull us into policy complacency with regards to the very real economic stress felt across the nation. By all forecasts, it simply falls far short of what is necessary to restore confidence among households. 2.8% just won’t cut it.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

It’s very sad that the elite make decisions based on what will increase their wealth instead of what is needed by average Americans, but not surprising. The credit policies are established to squeeze every ounce of wealth from the middle class and put it back into its rightly home, the kings and queens of wealth. We, the masses have a right to exist to the extent we provide for the demands of the corporate elite – when will we shut up and realize that. HOPEFULLY NEVER!

It is time for us to stop acting dumb about the abuses by Industry, allowed by it’s wife, Government, perpetrated by their freaky friends, Unions. When laws favor business, people suffer. Why are we surprised that over 10% of the population is fruitlessly looking for paid employment? The laws make it so big business can violate the people of third world nations and collect more profits than making products at home.

Why don’t we STOP BUYING? Commercialism ruined the holidays. Now it is political. And we, the masses keep doing the same thing over and over again. 10% of us don’t have jobs but we have to buy gifts for everyone and their children? Hello? If you don’t have enough income to pay your living expenses, you don’t have discretionary income to buy gifts. If you have to prove your love in dollars, you don’t understand love. Instead of wasting our money on unessential garbage, mostly made in unfair trade policies that are devastating the middle class, STOP BUYING!

Maybe then Government will figure out that we need to sell our products to other countries instead of allowing them to sell to us and blocking truly free trade. Maybe Industry will figure out that the masses CAN fight back against their abuses. Maybe the average people in this country need to decide for themselves what is important instead of being mindless drones, blindly following the law of commerce.

My holiday wish is for all big business to crumble under the weight of their greed and deceit so that they can be replaced with small and medium sized business that have been shut down by predatory practices, unfair trade and preferential legislation for the past century. I wish government officials and corporate executives contributing to this economy feel the affect of their decisions personally, so they can learn compassion for humanity. I wish the masses would consciously decide that business and government has a right to exist to the extent they provide for the needs and demands of every day people … and make it true.