What started the Great Depression? This column says that the industrial decline began before monetary contraction or banking panics – the conventional culprits – took hold. It attributes the massive drop in manufacturing hours to President Hoover’s labour policies, which kept nominal and real wages high.

Our current crisis continues to draw parallels to the Great Depression (Eichengreen and O’Rourke 2009) and has refocused attention on the 1930s. Several features of the US Depression, particularly its early phases, represent challenges to economic theory. These features, describe below in more detail, suggest that non-monetary, non-banking factors were important – in particular Herbert Hoover’s cartelisation and wage-setting policies.

In a recent paper, I consider the relationship between these facts and the start of the Depression, as well as the way in which it unfolded (Ohanian 2009). Several of these features of the Depression are not widely known, one of which is that the Depression was initially very severe in the industrial sector. Per-capita industrial hours worked declined by nearly 30% by the fall of 1930, roughly a year after the Depression started, which contrasts with the widely held view that the Depression started as a “garden variety” recession.

Standard explanations

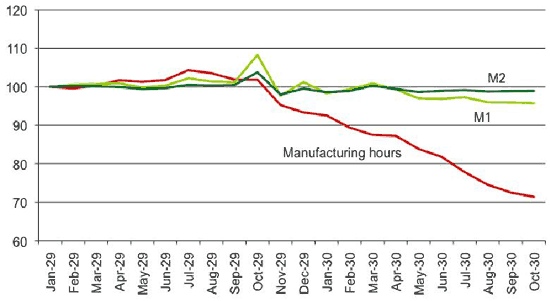

Economists cite monetary contraction (Friedman and Schwartz, 1963) and banking panics (Bernanke, 1983) as important determinants of the Depression, but industry was significantly depressed before either of these factors was quantitatively important. The attached figure shows per-capita industrial hours worked between January 1929 and September 1930, and two measures of the money stock from Friedman and Schwartz that roughly correspond to M1 and M2. Hours decline substantially, but these two measures of the money supply fall only about 4%, and 1%, respectively. Moreover, there are no significant banking panics during this early stage of the Depression. Friedman and Schwartz date the first banking panic occurring from November 1930 until January 1931, but this first episode is after industrial hours have fallen 30%. Moreover, Wicker (1996) argues that this first banking episode did not have important macroeconomic effects, which he states is also consistent with the views of Friedman and Schwartz.

Figure 1. Manufacturing hours and the money supply

Index: January 1929 = 100 for both series.

This indicates that a factor other than monetary contraction or bank runs was central in initiating the Depression. Moreover, this factor impacted the economy very differently across sectors. Hours worked in agriculture, which had roughly the same employment share as industry at that time, were roughly unchanged during the early 1930s, which indicates that the initiating factor behind the Depression was sector-specific.

Labour market data indicate that this factor impacted the economy by creating a labour market failure that prevented the industrial labour market from clearing. Nominal industrial wages declined little during the early stages of the Depression. Figure 3 from my paper shows both nominal and real manufacturing wages. Both micro and macro analyses suggest that these wages were above their market clearing levels. Curtis Simon (2000) analysed newspaper “situation wanted” advertisements in the 1930s, which were taken out by job seekers. Simon found that the supply price of labour – the wage rate being asked for by job seekers in their ads – was well below the wage rates that were being paid. Before the Depression, there was very little difference between the wage being asked for by job seekers and the wage being paid. In contrast, nominal wages in agriculture fell significantly, and agricultural employment changed very little at this time.

Mulligan (2005) and Chari, Kehoe, and McGrattan (2007) use aggregate data and reach a similar conclusion about an industrial labour market distortion by showing that there is a large deviation in the standard first order condition that equates the marginal rate of substitution between aggregate consumption and leisure to the real wage during the 1930s. These studies show that the marginal rate of substitution is much too low relative to the wage. Mulligan (2005) also shows that explanations such as changes in tax rates or transfers cannot plausibly account for the large gap in this condition. This evidence also suggests that the industrial wage was above its market-clearing level.

Basic economics

The basic economics from these analyses boils down to the following question: With substantial depression in the industrial sector, why didn’t the normal forces of supply and demand operate to lower the wage and raise output and hours worked?

I develop a theory to address this question of labour market failure based on President Hoover’s cartelisation and wage policies. Hoover’s views about competition and labour are clearly described in his memoirs (Hoover, 1951). Hoover thought that there was too much competition in the American economy in the 1920s and believed that industrial cooperation and codes of “fair competition” among business in the same industry would generate superior economic outcomes. Not surprisingly, Hoover’s initiatives that helped industry develop collusive trade groups fostered high industrial concentration and substantial monopoly distortions during this period (see Kovacic and Shapiro, 2000).

Hoover’ views about wages also differ considerably from today’s views. Many economists interpret high real wages as reflecting worker productivity that results from a skilled labour force working with a large stock of capital and efficient technologies. But Hoover believed that increasing wages in and of itself was important for promoting prosperity, as he apparently discounted the impact of higher wages on business hiring decisions.

Hoover’s economic views set the stage for meetings he held at the White House with major industry in late 1929 and advised them not to cut wages. Hoover told industry that maintaining wage levels would minimise the severity of a downturn and help him keep the peace with labour. Hoover also advised firms to share work among employees rather than relying exclusively on layoffs. Hoover then asked labour leaders not to strike and to withdraw requests for higher wages. Following these meetings, industry publicly acknowledged their compliance with Hoover’s labour programme as they held wage rates fixed and shared work among employees. And Hoover’s programme did keep the industrial peace – there was very little new unionisation or strikes during this period.

But declining prices and productivity, coupled with Hoover’s programme of fixing wages, significantly increased industrial labour costs. As the industrial decline intensified, industry leaders asked Hoover if he would support wage cuts that were proportional to the deflation that had occurred. But Hoover declined despite increasing criticism from various quarters that his programme was keeping wages far above their market-clearing levels. Many large firms kept their pledge with Hoover until the fall of 1931, at which point industrial hours worked had declined by nearly 40%.

I construct a growth model to analyse Hoover’s contribution to the start of the Depression that is similar to the model in Cole and Ohanian (2004), which analysed the contribution of Roosevelt’s cartelisation and wage-fixing policies. To account for the fact that Hoover’s policy did not impact the entire economy, I specify a two-sector model in which the industrial sector is directly impacted by Hoover’s programme and the other sector (agriculture) is not subject to this program. The impact of Hoover’s policy is analysed by feeding in the observed real manufacturing wage into the industrial sector of the economy. The industrial wage is exogenous from the perspective of firms in that industry, and I interpret this wage as the product of Hoover’s nominal wage maintenance programme and deflation. The model also includes lower productivity in the industrial sector, which further increases labour costs. Lower productivity in the model is specified as an exogenously reduced workweek (lower capital utilisation), though this could be modelled as another factor that depresses productivity and it would have the same effect on hiring decisions.

I find that Hoover’s programme generates a significant depression in the model, reducing real GDP by about 18% by the end of 1931, which accounts for about 2/3 of the Depression at that stage. The analysis is also consistent with the observed asymmetry across sectors, as industrial hours worked decline much more than agricultural hours. This asymmetry in sectoral responses in the model reflects the fact that the Hoover programme directly impacts the industrial sector, which then spills over to the agricultural sector because industrial output and agricultural output are complements and thus leads to a more moderate decline in agriculture.

Explaining the immediacy

The paper provides a theory for why the Depression was so immediately severe before significant monetary contraction and banking panics, why the Depression was so asymmetric across sectors, and also provides a theory for the industrial labour market failure – the fact that industrial wages were persistently well above their market-clearing level. This analysis, and my earlier work with Harold Cole (Cole and Ohanian 2004), suggests that the US economy of the 1930s would not have been as severely depressed if cartelisation and wage fixing policies had not been adopted. Ebell and Ritschl (2008) present a similar theory of the Depression by analysing the contribution of increased labour bargaining power on the economy in a search and matching framework and find that labour policy changes are central for understanding the Great Depression, including the enormous stock market decline.

While Hoover-type labour policies are not the central problem in today’s crisis, some economists are more broadly drawing parallels between labour market distortions of the 1930s and today and the contribution of public policy in generating those distortions. Casey Mulligan (2009a) shows that today’s crisis also features an increasing gap between the marginal rate of substitution between consumption and leisure and the real wage, and he interprets this gap as the consequence of public policies that implicitly – and substantially – raise the tax rate on debtors who have borrowed on assets whose value has fallen and impose large changes in marginal tax rates as a consequence of tax credits that are available only at certain income levels (see Mulligan 2009b, 2009c). While more research is needed on both of these episodes, the analyses cited in this article suggests that government policies that distorted labour markets are important for understanding both the 1930s and today.

References

•Chari, V.V., Patrick Kehoe, and Ellen McGrattan (2007), “Business Cycle Accounting”, Econometrica.

•Cole, Harold and Lee E. Ohanian (2004), “New Deal Policies and the Persistence of the Great Depression: A General Equilibrium Analysis”, Journal of Political Economy.

•Ebell, Monique, and Albrecht Ritschl (2008), “Real Origins of the Great Depression: Monopoly Power, Unions, and the American Business Cycle in the 1920s”, CEPR Discussion Paper 6146.

•Eichengreen, Barry, and Kevin O’Rourke (2009), “A Tale of Two Depressions”, VoxEU.org, 1 September.

•Friedman, Milton, and Anna Schwartz (1963), A Monetary History of the United States, Princeton University Press.

•Hoover, Herbert, The Memoirs of Herbert Hoover: Volume 3, The Great Depression, 1929-1941, The Macmillan Company.

•Kovacic, William and Carl Shapiro (2000), “Antitrust Policy: A Century of Economic and Legal Thinking”, Journal of Economic Perspectives, Winter.

•Mulligan, Casey (2005), “Public Policies as Specification Errors”, Review of Economic Dynamics.

•Mulligan, Casey (2009a), “What Caused the Recession of 2008? Evidence from Labour Productivity”, NBER Working Paper 14729.

•Mulligan, Casey (2009b), “A Depressing Scenario: Mortgage Debt Becomes Unemployment Insurance”, NBER Working Paper 14514.

•Mulligan, Casey (2009c), “Another (40 Percent) Marginal Tax Rate”, caseymulligan.blogspot.com, 9 October.

•Ohanian, Lee E. (2009) “What – or Who – Started the Great Depression?” NBER Working Paper No. 15258, August.

•Simon, Curtis (2001), “The Supply Price of Labour During the Great Depression”, Journal of Economic History.

•Wicker, Elmus (1996), The Banking Panics of the Great Depression, Cambridge University Press.

![]()

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply