Following an anaemic performance with severe imbalances in the 1990s and a debilitating financial crisis in 2001, Turkey enjoyed a period of rapid economic growth. Since about 2007 onwards, however, economic growth has slowed significantly and productivity growth has stagnated. This column argues that, rather than providing another example of the ‘stop-and-go’ cycles typical of emerging economies, the Turkish economy’s ups and downs during this era reflect institutional improvements in the immediate aftermath of its financial crisis, followed by an ominous slide in the quality of these economic and political institutions.

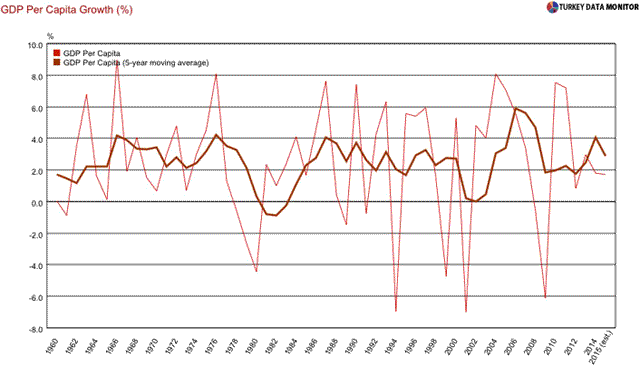

The Turkish economy has followed a roller-coaster ride in the past several decades. Following an anaemic performance with severe imbalances in the 1990s and a debilitating financial crisis in 2001, Turkey enjoyed five years of rapid economic growth, with GDP per capita increasing at almost 6% per annum – its highest ever rate since the 1960s – accompanied by structural changes, productivity growth and a broadening base of economic activity, both geographically and socially. From about 2007 onwards, however, economic growth slowed significantly as shown in Figure 1, and productivity growth stagnated for all practical purposes.

Figure 1. Turkish GDP per capita dynamics

Source: TURKSTAT, Development Ministry, Turkey Data Monitor.

What happened?

- The first explanation that comes to mind is that Turkey’s experience is just another example of the well-known ‘stop-and-go’ cycles so typical of emerging economies.

In recent work (Acemoglu and Ucer 2015), we depart from this point of view and argue that:

- Turkish economy’s ups and downs during this era reflect, first, institutional improvements in the immediate aftermath of its financial crisis, but then subsequently, an ominous slide in the quality of these economic and political institutions.

Why did Turkey undergo unusually rapid institutional improvements starting in 2001? Our answer emphasises a confluence of factors, partly external and partly internal. But perhaps most importantly:

- The 2001 financial crisis forced Turkey’s lethargic and conservative political system to accept a slew of fairly radical structural reforms imposed by the IMF and the World Bank.

These reforms not only brought under control the persistently high inflation and cut down budget deficits,1 but also imposed, inter alia, discipline on the budgetary process, shifted decision-making and regulatory authority towards autonomous agencies in an effort to cultivate rule-based policymaking (Atiyas 2012), and introduced transparency in the notoriously corrupt government procurement procedures.

In the background, these economic reforms were undergirded by major political changes. After their introduction by a care-taking government, they were overseen by the AK party (the Justice and Development Party), which ended the tutelage of the military over Turkish politics, which had held primacy at least since the founding of the Republic.

This political process, as well as the accompanying economic reforms, received a substantial boost from the general warming of EU-Turkey relations and the blossoming hopes among the Turkish population that accession to the EU was a real possibility. The EU process not only provided a powerful institutional anchor for many of the political and governance reforms, but also brought the promise of membership provided that economic and political reforms would continue.

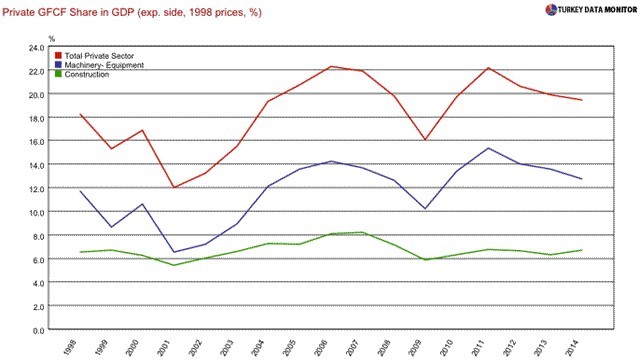

This account of the 2002-06 period as one of high-quality growth is not uncontroversial, and it is not possible to establish with any certainty whether a five-year growth spell reflects the flourishing of an economy under new economic institutions and reforms, or the first phase of yet another stop-and-go cycle. And yet, not only were the changes in economic institutions we have just described potentially far-reaching, but several pieces of evidence support the case that the nature of economic growth was very different during this interval than both before or after. Not only was productivity high by the standards of what came before and what was to follow (as well as by international comparisons), but the notorious macroeconomic imbalances of the 1990s subsided, as just described. Moreover, about half of productivity growth was driven by efficiency gains (i.e. driven by total factor productivity), while, as depicted in Figure 2, private investment as a share of GDP (in constant prices) rebounded sharply from its lows of the late 1990s (averaging about 17%), to almost 22% by the mid-2000s.

Figure 2. Private investment dynamics

Source: TURKSTAT; Turkey Data Monitor.

Equally important was the broadening of the base of the Turkish economy. Economic growth was in part driven by newer regions and firms than had been the norm in Turkish economic history.2 Moreover, there were improvements in health indicators and schooling among the poorest and most disadvantaged segments of the Turkish society,3 while fuelled by employment and income growth, inequality contracted significantly.4

These characteristics bolster our view that, absent the institutional turnaround, economic growth in Turkey could have continued without morphing into the low-quality growth observed in the post-2007 period, the latter characterised by, inter alia, little productivity and investment growth, if any, as well as a deteriorating growth-capital inflow nexus.

Reversal of reforms

Why then did these institutional improvements come to an end, bringing down both the rate and quality of economic growth in Turkey? We argue that the institutional change emanated from the political realm.

- To start with, the government of the AK party, which had earlier supported the economic opening, made an about-face once it became sufficiently powerful as the twin constraints coming from a strong opposition and the threat of military intervention disappeared.

Gradually, the de jure and the de facto control of the ruling cadre of the AK party intensified, amplifying corruption and arbitrary, unpredictable decision-making.

- Additionally, and as we argue quite pivotally, EU-accession talks collapsed, undermining both the anchor tying the AK party to the reform process and undermining the support that had built up for institutional change within a fairly broad segment of Turkish population.

The slide in economic institutions followed the political reversal quite closely.

The reforms initiated by the IMF and the World Bank gradually came to be reversed, with Turkey’s recently institutionalised rule-based policy framework increasingly shifting back towards discretion. The procurement law introduced in 2002 under the auspices of the IMF and World Bank, which at first reined in corruption, perhaps tells the story most vividly – more and more industries and items were declared exempt from the law by the ruling AK party, removing this fairly substantial barrier against corrupt practices (Gurakar and Gunduz 2015). The increase in corruption was not confined to procurements, and came to permeate deeper into the Turkish economy. As the power of autonomous agencies was clipped, taxation and regulation decisions turned increasingly arbitrary. The macroeconomic framework also worsened, as reflected by near zero or negative real interest rates while the economy was booming (especially during 2010-11), and increased government spending started propping up the economy. This low-quality growth also led to a relatively large current account deficit and an inflation rate stuck at high single-digits, markedly higher than Turkey’s trade partners.

Though, as already noted, we do not pretend that our arguments conclusively establish these causal links, they both invite further research into this fascinating and rather unusual episode of Turkish history and on the role of various external and internal anchors in triggering rapid institutional reform in institutionally weak economies, while suggesting some potentially useful lessons for the future of such economies. Admittedly, the prospect of a resurgence of institutional reforms and high-quality growth in Turkey looks dim at the moment, but ours is still a hopeful story for emerging market economies – it underscores the ability of economies with weak institutions to reform rapidly and enjoy the fruits of these institutional improvements in terms of rapid economic growth.

We are of course aware, and emphasise in our paper, that the process of all scale institutional change in Turkey was triggered by a deep financial crisis, which left few other choices to the political elites who would have otherwise not dreamt of mending the institutional ills serving their interests. Perhaps more ominously, the Turkish spring of institutional revival did not last, and appears to have made way to autocratic one-party rule.

These realistic caveats notwithstanding, we do believe that similar windows of opportunities present themselves to other emerging economies with some frequency, and the institutional about-face that the AK party engineered after about 2007 was not a forgone conclusion, and could have been prevented with a stronger civil society, more rambunctious and independent media, non-partisan and independent judicial institutions, and more vibrant and credible parliamentary opposition — conditions that were absent in Turkey at the beginning of 2000 but that are closer to being met in many Latin American and Asian economies.

References

•Acemoglu, D and E M Ucer (2015), “The Ups and Downs of Turkish Growth, 2002-2015: Political Dynamics, the EU and the Institutional Slide”, NBER Working Paper No. 21608.

•Atiyas, I (2012), “Economic Institutions and Institutional Change in Turkey during the Neoliberal Era”, New Perspectives on Turkey 14: 45-69.

•Gurakar, E Ç, and U Gunduz (2015), Europeanisation and De- Europeanisation of Public Procurement Policy in Turkey: Transparency versus Clientelism (Reform and Transition in the Mediterranean), Palgrave Pivot.

•World Bank (2014), Turkey’s Transitions: Integration, Inclusion, Institutions, Country Economic Memorandum, the World Bank, Washington D.C.

Footnotes

1 Inflation, which had averaged around 80% in the 1990s, swiftly fell to single digits, while public sector debt also declined sharply from a post-2001 crisis peak of 75% of GDP to about 35%.

2 The role of so-called ‘Anatolian Tiger’ cities (e.g. Konya, Kayseri, and Gaziantep) in this process is often emphasised.

3 For example, Turkey shows the largest improvements within the OECD in the quality of education as measured by OECD’s Program for International Student Assessment scores, with gains disproportionately concentrated among poorer households and in rural areas (World Bank 2014). The health and educational improvements were driven in large part by increased spending, makes feasible by reduced interest rate payments following the sharp drop in inflation. For example, we estimate that the share of health expenditures in total government expenditure increased by about 6 percentage points from 11% in 2002 to 17% in 2007 while the share of education rose from about 10% to almost 14%.

4 For example, the headline Gini coefficient of income inequality dropped from a very high 42% in 2003 to about 38% in 2008.

![]()

Leave a Reply