If you are like many of our readers, you are a bond guy and are well aware that CMBS (commercial mortgage-backed securities) are in an absolute free-fall. If you aren’t a bond guy, let me be the first to tell you that the CMBS market is in an absolute free-fall. Here is the chart on the Barclays INVESTMENT GRADE CMBS index month-to-date.

Yes… that -19.61 number? That’s a percentage return vs. Treasuries. The whole index down 20% month-to-date. Ugh.

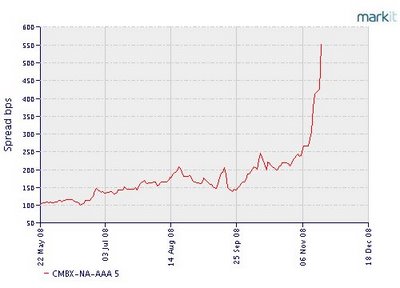

The story is no better for AAA-only bonds. Check out the AAA CMBX spread (higher spread = bad).

Readers may remember that I said AAA CMBX should tighten based on fundamental risk if the credit crisis was improving. That’s way back when this index was around 220. Now 550. So I’ll go ahead and say the credit crisis isn’t improving.

Anyway, this sparked an interesting debate among two colleagues of mine. I argued that if I had to blindly buy a CMBS deal full of hotel projects or retail projects, knowing nothing else about the deal, I’d buy the hotels. Its purely academic, because I actually wouldn’t buy either. But its an interesting debate, and I think its one that would extend to REIT stocks as well.

Here’s my thinking. I believe that the liquidity crisis is passing, but that we’re entering into a severe recession. Economic activity of all types are going to contract, so the question is who is better prepared for such a contraction?

Classically hotels have been viewed as more economically sensitive compared with retail. In a recession, business cut back on travel and consumers cut vacations. But they still keep shopping, even if at a reduced rate. Add in the fact that during the most recent recession, hotels were hit particularly hard, as 9/11 curtailed travel even more than a normal recession.

My conclusion is that the hotel sector might actually outperform the retail sector.

Post your thoughts, and remember death is not an option. You have to go to bed with one of these uglies, which one do you choose? I’m also posting a new poll on the same subject.

Leave a Reply