At the conclusion of this week’s FOMC meeting, policymakers released yet another statement that only a FedWatcher could love. It is definitely an exercise in reading between the lines. The Fed cut another $10 billion from the asset purchase program, as expected. The statement acknowledged that unemployment is no longer elevated and inflation has stabilized. But it is hard to see this as anything more that describing an evolution of activity that is fundamentally consistent with their existing outlook. Continue to expect the first rate hike around the middle of next year; my expectation leans toward the second quarter over the third.

The Fed began by acknowledging the second quarter GDP numbers:

Information received since the Federal Open Market Committee met in June indicates that growth in economic activity rebounded in the second quarter.

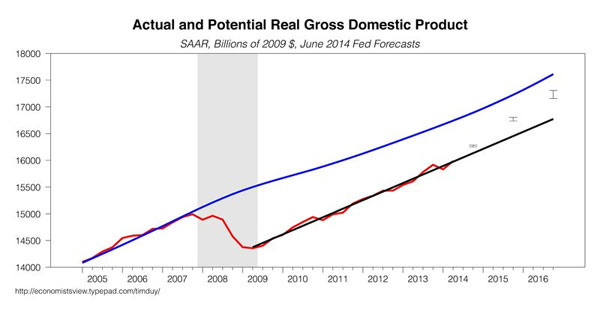

With the new data, the Fed’s (downwardly revised) growth expectations for this year remain attainable, but still requires an acceleration of activity that has so far been unattainable:

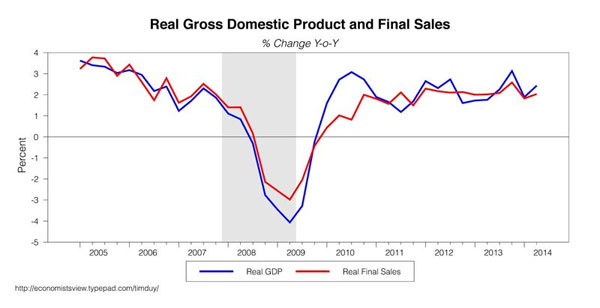

Despite all the quarterly twists and turns, underlying growth is simply nothing to write home about:

That slow yet steady growth, however, has been sufficient to support gradual improvement in labor markets, prompting the Fed to drop this line from the June statement:

The unemployment rate, though lower, remains elevated.

and replace it with:

Labor market conditions improved, with the unemployment rate declining further. However, a range of labor market indicators suggests that there remains significant underutilization of labor resources.

While the unemployment rate is no longer elevated, this is a fairly strong confirmation that Federal Reserve Chair Janet Yellen has the support of the FOMC. As a group, they continue to discount the improvement in the unemployment rate. And as long as wage growth remains tepid, this group will continue to have the upper hand.

The inflation story also reflects recent data. This from June:

Inflation has been running below the Committee’s longer-run objective, but longer-term inflation expectations have remained stable…The Committee sees the risks to the outlook for the economy and the labor market as nearly balanced. The Committee recognizes that inflation persistently below its 2 percent objective could pose risks to economic performance, and it is monitoring inflation developments carefully for evidence that inflation will move back toward its objective over the medium term.

became this:

Inflation has moved somewhat closer to the Committee’s longer-run objective. Longer-term inflation expectations have remained stable…The Committee sees the risks to the outlook for economic activity and the labor market as nearly balanced and judges that the likelihood of inflation running persistently below 2 percent has diminished somewhat.

Rather than something to worry over, I sense that the majority of the FOMC is feeling relief over the recent inflation data. It is often forgotten that the Fed WANTS inflation to move closer to 2%. The reality is finally starting to look like their forecast, which clears the way to begin normalizing policy next year. Given the current outlook, expect only gradual normalization.

Finally, we had a dissent:

Voting against was Charles I. Plosser who objected to the guidance indicating that it likely will be appropriate to maintain the current target range for the federal funds rate for “a considerable time after the asset purchase program ends,” because such language is time dependent and does not reflect the considerable economic progress that has been made toward the Committee’s goals.

We probably should have seen this coming; Philadelphia Fed President Charles Plosser raised this issue weeks ago. Clearly he is not getting much traction yet among his colleagues. I doubt they want to change the language before they have settled on a general exit strategy (which was probably the main topic of this meeting and will be the next). Somewhat surprising is that Dallas Federal Reserve President Richard Fisher did not join Plosser given Fisher’s sharp critique of monetary policy in Monday’s Wall Street Journal. Note to Fisher: Put up or shut up.

Bottom Line: Remember that we should see the statement shift in response to the data relative to the outlook. In short, the statement needs to remain consistent with the reaction function. The changes in the July statement reflect that consistency. The data continues to evolve in such a way that the Fed can remain patient in regards to policy normalization. We will see if that changes with the upcoming employment report; focus on the underlying numbers, as the Fed continues to discount the headline numbers.

Leave a Reply