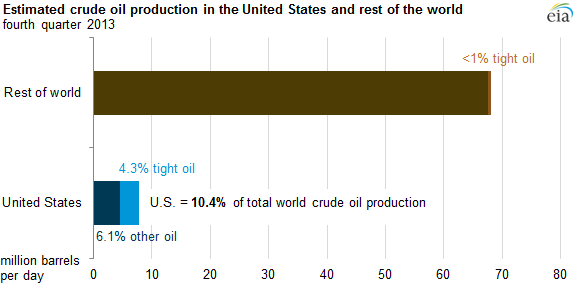

Oil produced from tight formations in the United States inaccessible before the days of horizontal fracturing is now accounting for 4.3% of total global crude oil production, according to new estimates released by the EIA last week.

Source: EIA

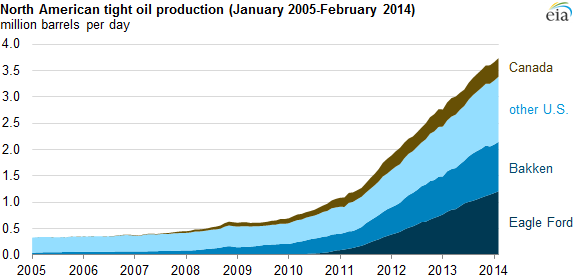

Most of the tight oil production is coming from the Bakken in North Dakota and Eagle Ford in Texas, though 340,000 b/d is now also being produced in Canada and 120,000 b/d in Russia.

Source: EIA

But this does not mean a flood of new oil is about to come on market. If it were not for the new tight oil, total world field production would be lower today than it was in 2005. And the new stuff is expensive. Chevron CEO John Watson last month said “Essentially, for a company like mine and many others, $100 a barrel is becoming the new $20 in our business”. And even with these elevated prices, Royal Dutch Shell; recently gave up on its large investments in Texan tight oil after concluding they couldn’t make a profit.

New production from tight formations drove the price of natural gas below the point at which it was profitable to produce. We’re still in the process of correcting that, and I expect natural gas prices to continue to rise from here. That same cycle of undershooting the sustainable price could replay in oil markets.

We’re used to thinking of a technological advance as something that enables us to produce better products at a lower price. Accessing tight oil formations using fracking is an important technological advance. But it’s clearly a much inferior source of energy compared to the days when we could just drill a few hundred feet into the earth and the oil would come gushing out. And anyone interpreting the recent trends as signaling that we’re about to return to that kind of a world is misreading the true meaning of what is happening.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply