The Bernanke era at the Fed came to an end today and many are already opining on what it means. Many smart things have been said about the Bernanke Fed, but most accounts have overlooked two of its biggest failures. No assessment of the Bernanke Fed is complete without recognizing them. So what were these two failures?

First, the Bernanke Fed never tried Abenomics. That is, for all the Fed has done over the past five years it never tried to do the kind of monetary regime change now being done by the Bank of Japan. A year ago, Japanese monetary authorities shook things up by credibly committing to permanently raising the nominal size of the Japanese economy. The evidence so far shows this program to be a smashing success. From the start, the Bernanke Fed took the opposite approach. It credibly committed to a temporary expansion of its balance sheet. The U.S. monetary injections, therefore, were never intended to be permanent and this makes all difference in the efficacy of monetary policy.

So for all the praise the Bernanke Fed gets for preventing the second Great Depression, it should be equally noted that it allowed the long slump. By failing to do Abenomics for the U.S. economy, the Bernanke Fed effectively kept monetary policy tight for the past five years. There is no other way to say it.

Okay, maybe there is another way to say it. The Bernanke Fed failed to meaningfully address the endogenous fall in the money supply and the decrease in money velocity. The Bernanke Fed could have done an American version of Abenomics, like nominal GDP level targeting, that would have arrested these developments.

Instead, it did not and passively allowed total dollar spending to remain depressed. This failure to act is no different than an explicit tightening of monetary policy in terms of damage done to the economy. The only difference is that the public is more aware of the explicit form.

In my view, this is the biggest failure of the Bernanke Fed. It had many opportunities to do it and much encouragement (e.g. Christina Romer’s call for Ben Bernanke to have a a Volker Moment). But it was not the only serious failure. There was another big one that preceded it.

This failure is that the Bernanke Fed in 2008 arguably turned what would have been an otherwise mild recession into the Great Recession. Over at Bloomberg opinions, Ramesh Ponnuru recently discussed this failure:

There’s another view of the Fed’s role in the crisis, though, that has been voiced by economists such as Scott Sumner of Bentley University, David Beckworth of Western Kentucky University and Robert Hetzel of the Richmond Fed. They dissent from the prevailing view that the Fed has been extremely loose since the crisis hit. Instead, they argue that the Fed has actually been extremely tight, and that when its performance during the crisis is measured against the proper yardstick, the central bank emerges as the chief villain of the story.

In the second half of 2008, housing prices, many commodity prices, inflation expectations and stocks all suggested deflation was coming. Fed officials, though, kept talking about backward-looking measures of inflation that made it look high. Their hawkish pronouncements effectively tightened monetary policy by shaping market expectations about its future direction. In August 2008, the Fed minutes explicitly said to expect tighter money. Even after Lehman Brothers Holdings Inc. collapsed the following month, the Fed refused to cut rates and fretted about inflation (which didn’t arrive). A few weeks later, the Fed decided to pay banks interest on excess reserves, a contractionary move. Only then did it cut interest rates.

Looking back, the Fed’s response from about mid-to-late 2008 was amazingly bad. It had done a decent job over the previous two years as the housing sector was undergoing its own recession, but for some reason lost focus in mid-2008. I believe it got overly worried about headline inflation. By failing to act more aggressively during this time, the Fed allowed monetary conditions to passively tighten. Here is how I previously described this period :

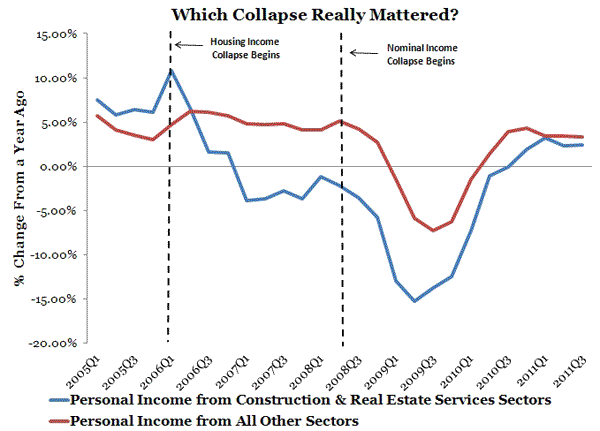

[t]he Fed passively tightened monetary policy starting around mid-2008. This can be seen in the figure below:

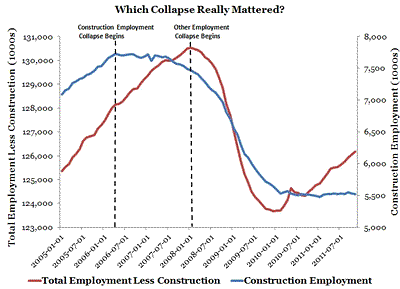

The figure shows that despite the fall in the growth rate of personal income from construction and real estate services that began in early 2006, personal income in the rest of the economy continued to grow at about 5% a year up through mid-2008. The Fed was able to stabilize nominal incomes overall for almost two years while structural changes were taken place in those sectors closely tied to the housing boom. This is a remarkable accomplishment and is especially clear when comparing construction employment with all other employment:

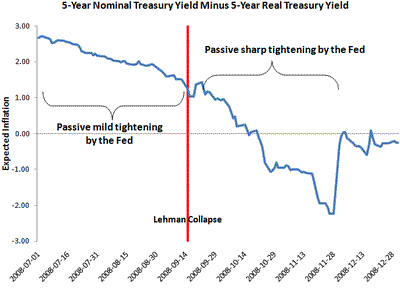

But around mid-2008 the Fed began failing to sufficiently respond to the decline in expected aggregate demand growth. Thus, it began passively tightening around that time as can be seen in the two figures below. The first figure shows the spread between the nominal and real yield on 5-year treasuries. It fell about 170 basis points during the period leading up to the collapse of Lehman in September. This decline in inflation expectations implies a decline in expected aggregate spending and thus a passive tightening of monetary policy. (Even if the spread was reflecting a heightened liquidity premium during this time the implication is the same. A heightened liquidity premium indicates increased demand for liquidity that, in turn, also implies less spending.)

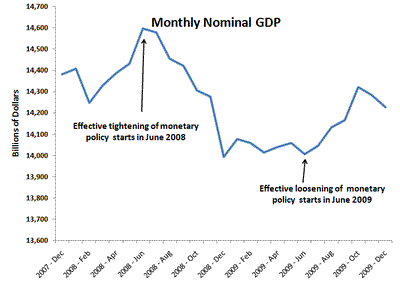

The decline in expected aggregated demand began affecting current spending decisions as seen below. Nominal GDP began falling in June 2008.

The Fed’s failure to stabilize and restore aggregate spending meant it was passively tightening. This failure to act was epitomized by the Fed’s decision in September, 2008 to not lower the federal funds rate despite the collapsing economy. This passive tightening is what turned a mild recession into the Great Recession.

Though this Bernanke failure was big, I do view it as less heinous than the failure to do an Abenomics-like program. The 2008 failure happened in real time and would have been difficult for anyone to have nimbly responded these developments. Still, my sense is that more could have done in both cases and this is why I consider them to be the big failures of the Bernanke Fed.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply