The Bank of England is searching for an alternative activist monetary policy. This column argues that it is, indeed, time for change. Although the inflation-targeting framework, begun in 1997, is clearly an improvement on all of the formal and informal frameworks the UK tried before that, there is now room for improvement. When there turned out to be problems with the exchange rate and then house prices, the authorities were unable or unwilling to modify the framework. In future, it might be desirable for the Bank to be given more goal-independence as well as instrument-independence, alongside arrangements to improve key appointments.

Before the Global Crisis it seemed as though the problems of monetary policy in the UK had been solved:

- This was a country that had experienced 25% inflation in the mid-1970s, followed by poor experiences of monetary targeting and later exchange-rate targeting.

- The inflation targeting initiated in 1993 and consolidated in 1997 with the establishment of the Monetary Policy Committee of the Bank of England to set interest rates seemed to be ensuring price stability along with reasonable growth.

As late as 2010, Besley and Sheedy (2010) talked only of the difficulties facing inflation targeting in turbulent times, with little suggestion of any shortcomings in the Great Moderation years.

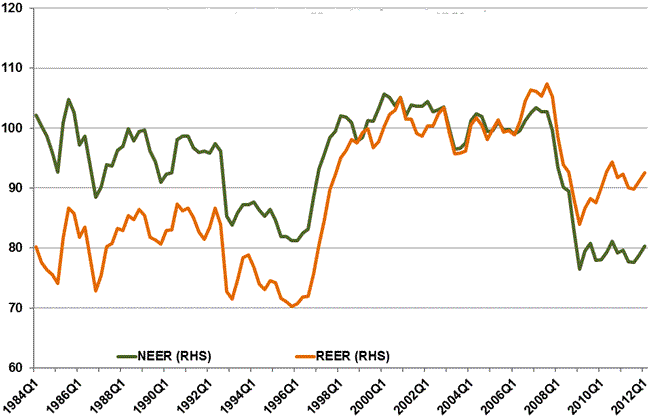

Figure 1. Nominal and real effective exchange rates

(click to enlarge)

First major problem

It is now much clearer that there were major problems in UK monetary policy during the Great Moderation period itself. These were related to its underlying conception:

- First, the sterling exchange rate appreciated by some 21% between first half 1996 and second half 1997, and it remained broadly at that level until 2008 (see Figure 1).

Prices and wages did not adjust to this level, so that the real effective exchange rate also remained some 27% above its 1984-1996 average.

It seems that the Monetary Policy Committee understood the initial appreciation and considered the exchange rate overvalued, but was essentially unable to predict ex ante or even explain ex post major exchange-rate movements (Cobham 2006 2013a).

The misalignment could not be addressed within the new monetary framework. Arguments about reducing interest rates to try to undo the overvaluation were always overruled by arguments about the need to keep to the inflation target. The Monetary Policy Committee managed overall aggregate demand, to hit its inflation target, but this meant in effect that it encouraged the more responsive output of non-tradables and services, while the output of tradables and manufactures was constrained by a severe lack of competitiveness.

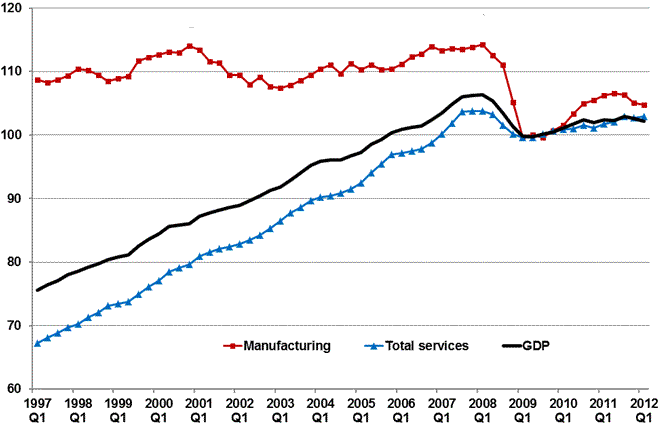

Although other factors were also at work, it is likely that the level of the exchange rate contributed to the stagnation of UK manufacturing over the 1997-2007 period, when services and overall GDP grew much faster (Figure 2).

Figure 2. Manufacturing, services and GDP

(click to enlarge)

The interest-rate differences

A striking interest-rate phenomenon from the ‘1999-2007 period’ may be related to this. While inflation was lower and growth higher in the UK than in the US and the Eurozone, nominal interest rates were on average significantly higher in the UK. Real interest rates were on average 2.3% higher (Table 1).

- Given capital mobility and liberalised financial markets, this difference is unlikely to reflect differences in equilibrium real interest rates.

It is more likely to reflect a situation where both the financial markets and the Monetary Policy Committee thought sterling was about to depreciate – ith possible inflationary consequences (given earlier experiences with exchange rate-prices pass-through). The Monetary Policy Committee felt obliged to keep its policy rate continuously high to offset such effects.1

Table 1. International comparisons, 1999-2007

Notes: data for 1999 Q1 to 2007 Q4; s.d. is standard deviation; inflation is CPI from International Financial Statistics; output growth is since four quarters before; policy rate data are end-quarter; real policy rates are ex post, i.e. nominal policy rates minus inflation.

Second major problem

The second problem during the Great Moderation is the lack of response to house-price growth.

- There is evidence that the Monetary Policy Committee took this issue rather more seriously than the US Federal Open Markets Committee (Cobham 2013b).

The Monetary Policy Committee presented arguments that house price growth was due to fundamentals (essentially the much lower level of long term interest rates) and was not a bubble (e.g. Nickell 2005). Nevertheless, the Committee was clearly wedded to the same view as the Fed, namely that monetary policy should not respond to asset prices but should just stand ready to soften any crash (‘cleaning’ rather than ‘leaning’).

- Excessive house price growth can be seen as a feature of the way in which western economic, monetary and financial systems had evolved over recent decades.

Financial liberalisation and the concentration of monetary policy on inflation in goods and services may have contributed to a more ‘elastic’ financial system (Borio and White 2004).

- It is possible to argue that, while under inflation targeting, central bankers made efforts to ensure that expectations of inflation in goods and services remained low, they made no such efforts with respect to inflation in asset prices.

Inflation expectations had a floor (the commitment to relax policy if prices crashed) but no ceiling – this was known as the ‘Greenspan put’.

In that sense the policy frameworks in the UK and the US – confirmed by the failure of the central banks to respond to rising house price growth –can be argued to have contributed to the eruption of the financial crisis in 2007-08. It is obvious, however, that different behaviour by the Bank of England alone could not have pre-empted the crisis in the absence of action in the US. The US was the dominant economy in the world and its housing-price fluctuations had by far the largest impact on US and other banks’ balance sheets. There is also no doubt that financial regulation was much too lax in the years before the crisis (Daripa, Kapur and Wright 2013).

Inflating targeting despite the shortcomings

Despite these arguable shortcomings, the UK’s formal monetary policy framework remains that of inflation targeting:

- Quantitative easing was originally justified in this way when it was introduced in March 2009.

- Policy has continued to be so presented even in the face of above-target inflation.

QE itself is probably widely agreed to have been an essential response to the crisis in 2009.

- But the evidence suggests QE’s effectiveness is declining over time (Goodhart and Ashworth 2012, Martin and Milas 2012).

The government has been casting around for ways to make monetary policy more activist.

Nominal-income targeting, pro-investment policies and forward guidance

There was a flurry of speculation about nominal income targeting after a speech by the new Governor-designate, Mark Carney, in December 2012. There are well-known problems with that strategy (see Goodhart, Baker and Ashworth 2013).

- The Monetary Policy Committee’s remit was restated by Chancellor Osborne in March 2013, with marginally more emphasis on economic growth but no fundamental change.

Instead the authorities have introduced pro-investment policies:

- The Funding for Lending Scheme;

This appears to be having relatively little impact so far on banks’ lending. And

- The Help to Buy initiative.2

This has been widely criticised for its likely effects on house prices rather than house construction.

More recently the new Governor has resorted to ‘forward guidance’ – announcing that it would not raise its policy rate until unemployment had fallen significantly. However, this was hedged around by several ‘knockout clauses’ which must have diluted the impact. So far this guidance seems to be being disbelieved by the financial markets, though there is some sign that the wider public has been influenced by it (Financial Times 2013).

Focus instruments rather than the framework

This focus on the instruments of monetary policy rather than the overall framework makes sense. There is a basic instrument problem:

- When firms and households are keen to invest but need to borrow to do so, a higher policy interest rate dampens investment at the margin.

- When confidence is low and firms and households are not keen to borrow and invest, a fall in the interest rate may have little impact on their plans (even when the interest is above zero).

Thus even if a new nominal income targeting framework required the Monetary Policy Committe to operate a more expansionary monetary policy that could not be done without appropriate instruments.

This sort of argument leads on inevitably to the elephant in the room, which is fiscal policy. Here the idea is to think of a ‘corridor’ around full employment (Leijonhufvud, 2009):

- Inside the full-employment corridor, the economy is largely self-adjusting and monetary policy is sufficient;

- Below the corridor, low confidence and expectations are a problem and pump-priming expectations-falsifying fiscal policy may be useful.

Macroprudential policy

However, in other respects the framework is already changing. A range of macroprudential levers are now controlled by the Bank’s Financial Policy Committee. This is the official answer to the issue of asset prices, and may provide some constraint on house prices (but not exchange rates).

- In the past, the main coordination problems in a crisis for a central bank were coordination between the central bank, the banking supervisory (microprudential) agency, and the ministry of finance.

- Now there is an added and more continuous issue of coordination between the body which operates macroprudential policy and the body which makes monetary policy decisions, where each body’s decision may impact on the other body’s objective as well as its own.

Concluding remarks

The inflation targeting framework since 1997 is clearly an improvement on all of the many formal and informal frameworks the UK has tried before. But there is room for improvement. Inflation targeting was arguably ‘best practice’ as of 1997 – including maybe some US influence on the neglect of the exchange rate.

But when there turned out to be problems with the exchange rate and then house prices, the authorities were unable or unwilling to modify that framework. This may have been in part due to the unusual continuity of personnel. At the Bank Mervyn King was Chief Economist, Deputy Governor and then Governor. At the Treasury, Gordon Brown and Ed Balls were dominant throughout the period.

- It is arguable that the UK had to pass through a period of very limited discretion, because of the historically poor reputation and credibility of UK monetary policy and the low level of central bank independence before 1997;

In the future, however, it might be possible and desirable for the Bank to be given more goal-independence as well as instrument-independence (along with arrangements to improve key appointments).

- This would allow the Bank to choose compromises between different objectives as circumstances change – always subject to an overriding price stability constraint.

Insofar as there is some evidence that the Bank is already doing this, in a limited and covert way (Wren-Lewis 2013), this would improve the transparency of monetary policy as well as its ability to produce socially desirable outcomes.

References

•Besley, T, and Sheedy, K (2010), “Monetary policy under Labour”, National Institute Economic Review 212, R15-33.

•Cobham, D (2006), “The overvaluation of sterling since 1996: how the policymakers responded and why”, Economic Journal 116, F185-207.

•Cobham, D (2013a), “Monetary policy under the Labour government: the first 13 years of the MPC”, Oxford Review of Economic Policy 29(1), 47-70.

•Cobham, D (2013b), “Central banks and house prices in the run-up to the crisis”, Oxford Economic Papers 65 (S1), i42-i65.

•Daripa, A, Kapur, S, and Wright, S (2013), “Labour’s record on financial regulation”, Oxford Review of Economic Policy 29(1), 71-94.

•Financial Times (2013), “Carney scores mixed success in his quest to win over believers”, Financial Times 6 September.

•Goodhart, C, and Ashworth, A (2012), “QE: a successful start may be running into diminishing returns”, Oxford Review of Economic Policy 28(4), 640-70.

•Goodhart, C, Baker, M, and Ashworth, A (2013), “Monetary targetry: Might Carney make a difference?”, VoxEU.org, 22 January.

•Martin, C, and Milas, C (2012), “Quantitative easing: a sceptical survey”, Oxford Review of Economic Policy 28(4), 750-64.

•Nickell, S (2005), “Practical issues in UK monetary policy, 2000-2005”, Bank of England.

•Wren-Lewis, S (2013), “Bean on nominal GDP targets”.

______

1 There is an ‘oral tradition’ that seeks to explain the phenomenon in terms of differential fiscal policies, but this is not consistent with the trends in fiscal deficits in the UK, US and Eurozone.

2 Under the Funding for Lending Scheme, banks get cheap financing if they undertake new lending (from summer 2012). Help to Buy gives a subsidy to house purchasers on their mortgages (from early 2013).

![]()

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply