I suppose I should not have been shocked. Economics is full of obvious truths that sound odd when expressed in an unfamiliar way. Everyone knows that the real demand for money slopes downward, as a function of the nominal interest rates. It’s in all the textbooks. If you raise the opportunity cost of holding base money (the interest rate) people will hold less base money. It’s basic supply and demand.

But people seem shocked by the implications. Higher interest rates raise velocity. In a moment I’ll show you some evidence. And there is a mountain of academic studies that show this to be true (Cagan, etc.) But what it implies is that holding the money supply constant, higher interest rates will raise not just V, but also NGDP and inflation. And that’s what shocks people.

They are not always shocked by this relationship. They understand that fiscal stimulus can raise interest rates and raise inflation, holding M constant. Ditto for greater animal spirits leading to more investment. It’s the tight money that throws people off. How can tight money raise inflation? It doesn’t, but the higher short term interest rates caused by tight money do raise inflation. We don’t notice it because the overall effect is for lower inflation. The reduction in M reduces NGDP and inflation by more than the higher interest rates from tight money raises V and inflation. There is nothing at all controversial in what I am saying here. Indeed this is an argument that Keynesians frequently make to criticize monetarism. The gains from more M will be offset by less V.

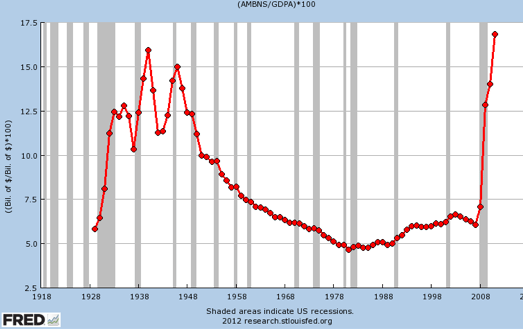

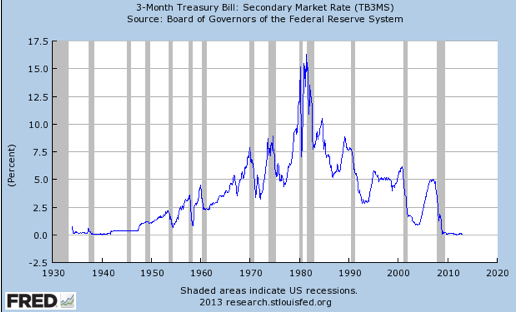

I could not find a time series of base velocity, but I did find it’s inverse, the base/GDP ratio. And I found short term interest rates since 1934. Note that between 1929 and 1934 (not shown on graph) the short term rate plunged from about 6% to little more than zero. That explains the huge surge in the base/GDP ratio during 1929-34, and the resulting plunge in base velocity. There is a drop in the base/GDP ratio in 1937 as rates rose slightly above zero in a premature exit from the zero rate trap (coming soon to theatres near you.) Then rates go right back to zero, and the base/GDP ratio shoots up again peaking in 1940, when T-bill yields hit bottom. After the war, interest rates trended upward all the way to 1981, and the base/GDP ratio falls, bottoming out in 1981 (i.e. velocity peaks). Then interest rates fall gradually, and velocity falls as well, as the base/GDP ratio rises. Recent years are a repeat of the 1930s. I would add that after 2008 you don’t want to look at the nominal interest rate alone, rather the velocity of bank reserves depends on the short term interest rate minus IOR, which is actually negative. The last 4 years are the least costly time in all of world history to hold reserves.

Leave a Reply