The Dow Jones Industrial Average experienced its worst quarter since the beginning of 2009. The S&P 500 Index fell 14 percent during the third quarter, with the materials sector as the worst performer, falling 25 percent. Many base metal commodities saw double digit declines, but not surprisingly, gold increased 8 percent over the quarter. It appears that fear of a “2008 repeat” drove investors from stocks despite positive long-term fundamentals.

The Dow Jones Industrial Average experienced its worst quarter since the beginning of 2009. The S&P 500 Index fell 14 percent during the third quarter, with the materials sector as the worst performer, falling 25 percent. Many base metal commodities saw double digit declines, but not surprisingly, gold increased 8 percent over the quarter. It appears that fear of a “2008 repeat” drove investors from stocks despite positive long-term fundamentals.

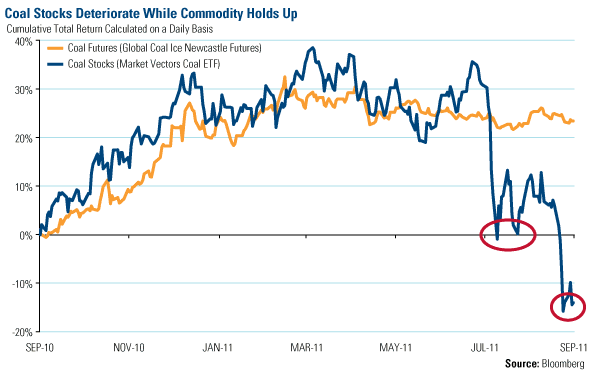

Coal was relatively flat for the quarter, but what’s interesting is that coal companies were severely discounted. Over the last two years, coal stocks and the commodity have closely tracked each other, until this summer, when worries about a global slowdown caused coal stocks to fall off a cliff, not once, but twice, in August and again in early September. This extreme divergence between coal companies and the commodity seems unwarranted when the long-term drivers of coal remain supportive.

We discussed coal in May in Coal Use in China Shines Light on Growth, and highlighted how the price of coal was supported by strong demand from reconstruction projects in Japan along with reduced supply from floods in Australia, Indonesia, South Africa and Colombia. As the largest consumer of coal in the world, China was expected to continue to demand a significant amount of coal over the long term.

This long-term driver hasn’t changed, even with China’s concentration on controlling inflation this year. Coal inventory levels at China’s top loading port have dropped, hitting a new low at the end of September, reports Macquarie Research. In mid-September, the Daqin Railway was under maintenance for a few weeks, causing reduced deliveries, which put further pressure on the country’s inventory. As the world’s largest coal transport railway, the Daqin line transports coal from northern China to Zinhuangdao for shipping to manufacturing centers in the south and the east.

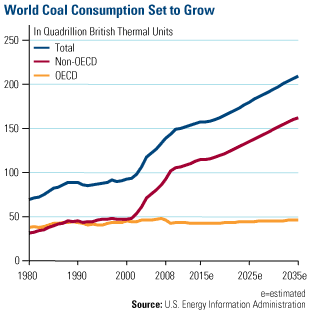

Throughout the world, coal demand is expected to rise significantly over the next 25 years. According to the U.S. Energy Information Administration’s (EIA) recent International Energy Outlook 2011, total coal demand will be driven largely by the non-OECD economies, which are primarily emerging markets. Specifically, the Asian non-OECD countries are projected to account for nearly all of the increase from 2008 through 2035, with China averaging 5.7 percent each year and India averaging 5.5 percent per year, says the EIA.

Today’s worries about a global slowdown shouldn’t impact China’s consumption levels for many commodities. In fact, a worldwide slowdown may spur additional demand from China. Macquarie explains that China’s government tends to “de-synchronize” the country compared with the rest of the world, creating an inverse relationship. This means that when the world is growing, China becomes so concerned about rising costs and inflation, that it moves quickly to slow growth.

Today’s worries about a global slowdown shouldn’t impact China’s consumption levels for many commodities. In fact, a worldwide slowdown may spur additional demand from China. Macquarie explains that China’s government tends to “de-synchronize” the country compared with the rest of the world, creating an inverse relationship. This means that when the world is growing, China becomes so concerned about rising costs and inflation, that it moves quickly to slow growth.

Conversely, when world demand for commodities slows, China ramps up its infrastructure projects and scoops up unwanted commodities. In China-The Great Stabilizer, I showed a Macquarie chart indicating how China’s demand for many base metals has run counter to world demand over the last 10 years. Most recently, in 2008, the de-synchronization took place when China first moved to slow growth to combat increasing inflation. As the global crisis caused a significant slowdown, “authorities moved quickly to substantially ease monetary and fiscal policy,” says Macquarie. Due to its long-term planning, China can start and stop infrastructure projects at will.

In addition, Macquarie says that potential growth of the country generally outpaces its energy and resources capacity.

The recent dramatic decline in coal stocks has been driven by concerns of a global slowdown, but with equities already down 40 percent from their July highs, we feel this negative sentiment is already priced in. Given the encouraging long-term fundamentals, along with the fact that the underlying commodity has roughly stayed the same over the past few months, it appears that fear is the driver. This is often when opportunity knocks.

John Derrick, director of research, contributed to this commentary.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply