With some trepidation, last night I called up a guy who manages a hedge fund (with some of my money in it) and asked, “So, how’d we do?” He says, ”We’re down 3% for the month. We got creamed on our longs but we were hedged, so the net was not so bad.”

I say, “Gee that’s great news! So you were long puts?” He gave a surprise response:

“No puts. We were long a bunch of long dated Treasury zero coupon bonds.”

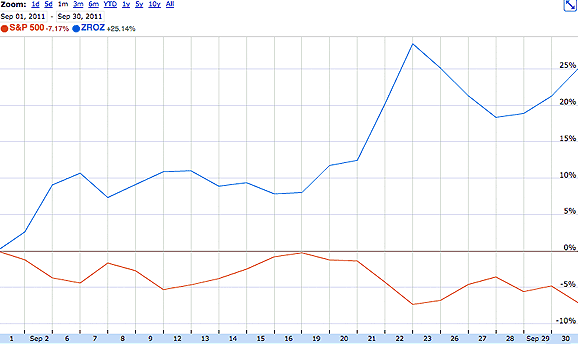

My guy’s defensive tactics worked very well in September. I think there was some of the biggest % moves in history in bond land. Consider this chart. Zeros were up 25% while the S&P was down 8%.

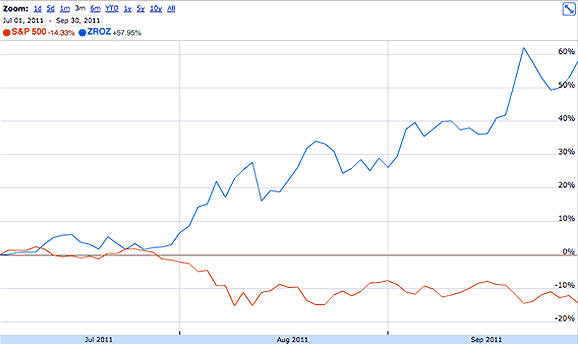

This trend has been going on for months. This chart looks at the last three. Note that Zeros are up 50%! Note also how tight the inverse correlation is.

I find this troubling. While I can get comfortable with a balanced portfolio where bonds counter cyclically provide a natural hedge, I do have trouble with hedge funds using the bond market as a synthetic “Put” against long equity exposure.

The reason for my concern is the leverage that is involved in creating a viable hedging mechanism. Based on recent results the hedging ratio of long zeros as a hedge against long stocks is about 3 to 1. So a billion of stocks is “hedged” when a $350mm long zero position is coupled with it. A zero has the duration equivalent of 4+Xs a straight ten-year. So another way of thinking of this is that to “hedge” $1 of S&P one would need to “own” (It’s all leveraged) about $2 in ten-year bonds.

I think this an unnatural act of a sort. Leveraged bets in bonds are just that. A bet on bonds. They are not supposed to be a hedge against equity exposure. But they are. So what does that mean?

I conclude that we are in a bubble for bonds. There are people who own them for the wrong reasons. It’s speculation, not investing, that’s driving the bond market. So we are in the worst kind of bubble. A speculative one.

Please don’t read this as a recommendation to get short bonds. It’s not. I think we are in a bond bubble, but I don’t see that changing anytime soon. That said, a final thought from the fellow who runs money.

We’re concerned that our hedges are going to decouple. Interest rates can’t go much lower from here. It’s possible that global stocks can go down and US interest rates don’t follow suit.

If that happens we will have to respond. We may be forced to unwind the zeros and just buy more traditional insurance. The problem is that the alternative is very costly.

What he is saying is that he would be a net seller of Treasuries with a long duration and a net buyer of equity put protection. By itself, this would tend to exert downward pressure on stocks and also downward pressure on long dated bonds.

Where’s the Good News?

Leave a Reply