The divergence between PCE and CPI measures of inflation remains in the headlines. Pedro da Costa at Reuters sees a test of the Fed’s credibility at hand:

With the inflation rate about half of the Federal Reserve’s 2.0 percent target, the central bank is facing a major test and some experts wonder whether it will eventually need to ramp up its already aggressive bond buying program.

The challenge for policymakers is that they are clearly falling short of their dual mandate and that should open the door for additional asset purchases. But, but, but…I think that additional asset purchases is just about the last thing they want to do right now. We will see if their thinking evolved much at the last FOMC meeting, but the minutes of the March meeting clearly indicate that a large contingent of FOMC members are looking to end the asset purchase program by the end of this year. Take ongoing improvements in labor markets, add in concerns about financial stability, mix in some cost-benefit analysis about the efficacy of additional QE, and top-off with a dash of improving housing markets, bake at 350 for 40 minutes, and you get monetary policymakers hesitant to push the QE lever any further.

My sense is that policymakers will thus try to find reasons to dismiss falling PCE inflation as a non-issue. From an email exchange last week, today da Costa quotes me as saying:

“The Fed may view the divergence between the two measures as indicating that worries about deflation are premature,” said Tim Duy, a professor of economics at the University of Oregon. “If core CPI was trending down as well, the Fed would be more likely to conclude that their inflation forecasts should be guided lower.”

And also last week in March, Greg Ip at the Economist had this observation:

If CPI inflation were to converge to PCE inflation, that would be a concern. Goldman expects CPI inflation to drop to 1.8% in coming years and PCE inflation to rise to 1.5%. It would be preferable for both to converge to 2%; but so long as inflation expectations remain where they are, it is of little consequence for monetary policy – and a tangible plus for incomes and spending.

Yesterday, Philadelphia Federal Reserve President Charles Plosser had this to add, via the Wall Street Journal:

As of right now, “I’m not concerned” about inflation drifting too far under the central bank’s price target of 2%, Federal Reserve Bank of Philadelphia President Charles Plosser said in response to reporter’s questions at a conference here.

Inflation expectations “look pretty well anchored,” and it’s likely that price pressures as measured by the personal consumption expenditures price index will drift back up to 2% over time and reconverge with the consumer price index, he said.

Today, Chicago Federal Reserve President Charles Evans seemed resigned to low inflation. Again, from the Wall Street Journal:

“Inflation is low, and it’s lower than our long-run objective,” Mr. Evens said in an interview on Bloomberg Television, adding that he would like to see inflation closer to 2% but expects it to stay below 2% for several more years. Inflation, he said, “can be too low” when the central bank’s objective is 2%.

Asked if low inflation should prompt a policy response from the Fed, Mr. Evans said “I think it’s way too early to think like that.” In the debate over how the Fed might exit from the asset purchase program, Mr. Evans, a voting member of the policy-settingFederal Open Market Committee, said he remains “open minded [and] I’m listening to my colleagues.”

The general story seems to be that as long as inflation expectations remain anchored, and CPI inflation does not drift much below 2%, then the Fed will resist accelerating the pace of asset purchases.

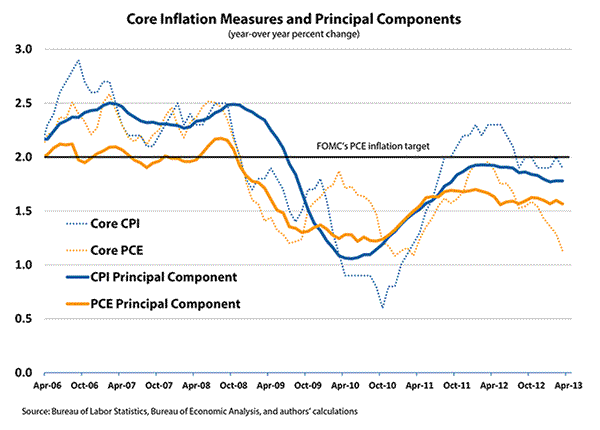

Also note that the downward inflation drift is an underlying trend, or so concludes the Federal Reserve Bank of Atlanta’s macroblog. The authors use a principle component model to estimate a common trend in the price data, and get these results:

The author’s note that by this measure, the decline in PCE is not as ominous as it first seems, but it is clear that inflation by either measure is missing the Fed’s target and currently trending away from that target. They conclude:

Does that mean we should ignore the recent disinflation being exhibited in the core PCE inflation measure? Well, let’s put it this way: If you’re a glass-half-full sort, we’d say that the recent disinflation trend exhibited by the PCE price index doesn’t seem to be “woven” into the detailed price data, and it certainly doesn’t look like what we saw in 2010. But to you glass-half-empty types, we’d also point out that getting the inflation trend up to 2 percent is proving to be a curiously difficult task.

Indeed, very curious given that we tend to think that at a minimum the monetary authority should be able to raise inflation rates. You are left with thinking that either the Federal Reserve still had more work to do or that monetary policy can do little more at this point than put a floor under the economy. If the latter, and if you want something more, you need to turn to fiscal policy.

Bottom Line: I suspect that at this point the Fed tends to think the costs of additional action still outweigh the benefits, and thus below-target inflation only induces pressure to maintain the current pace of QE longer than they currently anticipate rather than increase the pace of purchases.

Leave a Reply