On Friday I discussed the cyclically-adjusted U.S. budget deficit and asked any Keynesian to reconcile its decline with the steady growth of aggregate demand. Robert Waldman graciously replied, but he really didn’t answer my question. His response focused on the pace of the recovery and changes in the overall budget balance. My question was about the structural budget balance. This distinction is an important one. So let me try this one more time.

The structural budget balance is the best way to gauge the stance of fiscal policy, as noted by Paul Krugman:

[M]easuring austerity is tricky. You can’t just use budget surpluses or deficits, because these are affected by the state of the economy. You can — and I often have — use “cyclically adjusted” budget balances, which are supposed to take account of this effect. This is better; however, these numbers depend on estimates of potential output, which themselves seem to be affected by business cycle developments. So the best measure, arguably, would look directly at policy changes. And it turns out that the IMF Fiscal Monitor provides us with those estimates, as a share of potential GDP…

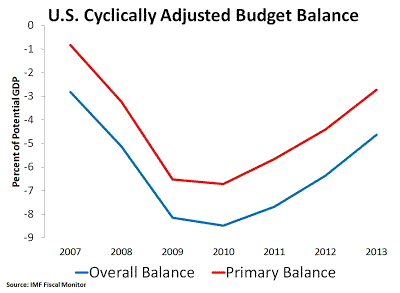

Here is the IMF’s cyclically-adjusted or structural budget balance for the United States:

So what does this figure tell us? It shows that fiscal policy, independent of business cycle influences, has been tightening since 2010. It has gone from a deficit of 8.5% in 2010 to an expected one of about 4.6% in 2013. In other words, the reduction in the federal budget deficit over the past three years is more than just the government adjusting its balance sheet in response to improvements in the private sector’s balance sheet. It is also the result of explicit policy choices to impose fiscal austerity. And these explicit policy changes have been relatively sharp.

Many observers have overlooked the implications of this structural austerity experiment. Three years of explicit fiscal austerity in a depressed economy should, all else equal, lead to even more economic weakness. But it has not. Nominal GDP growth–a proxy for aggregate demand (AD) growth–has been remarkably steady. There is no evidence AD over the past three years has been adversely affected by this austerity. Friday’s job report underscores this point.

So what explains this development? The answer is not that fiscal policy has no effect, but rather that all else is not being held equal for U.S. aggregate demand growth. Specifically, Fed policy has effectively responded to the fiscal austerity, Eurozone shocks, China slowdown shocks, and other shocks to AD. Though this is a great accomplishment, it is far from adequate and is ultimately frustrating to watch. For it speaks to both the power and shortcomings of current Fed policy.

It is not surprising to me that Keynesians and other observers fail to see this structural austerity. The Fed has offset it over the past three years and therefore kept it out of sight, out of mind. The ECB, on the other hand, has not and so it is more apparent to observers. But just because it is not seen, does not mean it is not there.

Leave a Reply