To me, the central issue raised by this week’s Cyprus debacle is how it has affected confidence across the eurozone. To what degree has the possibility of insured depositors at a eurozone bank losing a portion of their deposits affected the mindset of depositors? To what degree has ECB acquiescence to this possibility undermined the notion that deposit insurance in the eurozone means the same thing in all countries? And to what degree has the ECB’s direct threat to end support for Cyprus’s banking system in the event that the government of Cyprus can not arrange sufficient funds to meet its conditions made a farce of its earlier promise to “do whatever it takes to preserve the euro”?

These, to me, are the interesting questions prompted by this week’s events. And while no one can definitively say that they know the answers to these questions, the answers will likely have a very direct bearing on the future of the eurozone. It’s a pity that we need to ask them at all — if things had been handled better in Brussels, Frankfurt, and Nicosia last weekend then we wouldn’t even be thinking about these questions right now. But they weren’t, and we are.

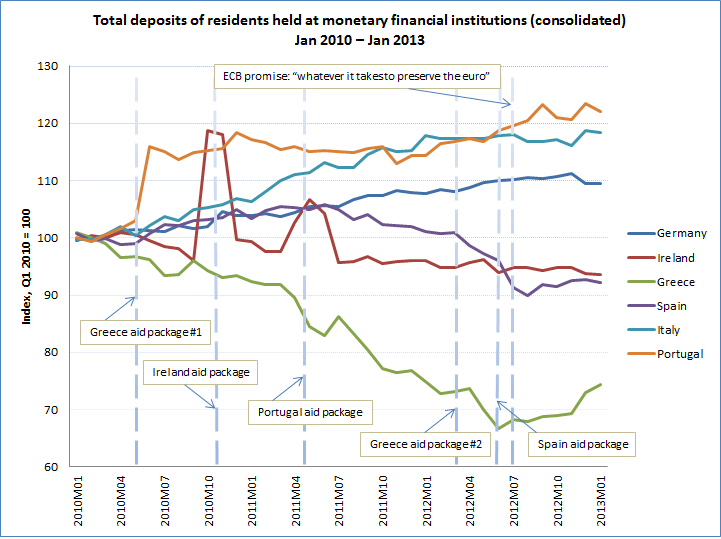

While I don’t know how significantly confidence in the eurozone periphery’s banks have been shaken by this week’s events, I do have an idea of what I will be keeping an eye on over the coming weeks and months: deposits in banks in Greece and Spain.

Perhaps depositors will shrug off this week’s events as being particular to Cyprus, with no broader ramifications. In that case, the eurozone may be able to get back to business as usual. (Cyprus excepted, of course.)

But if people around Europe’s periphery start questioning the commitment of the ECB to banks in the periphery countries, and start considering that insured banking deposits are not actually risk-free if they happen to be in a bank in a southern European country, then it’s possible that depositors may start moving their assets out of those banks.

Deposits in the already weak banking systems of Spain and Greece seem to me the most likely to be at risk. While there’s no reason to expect a sudden rush for the exits in those countries, it may not be unreasonable for people to believe that a €100.000 deposit in Deutsche Bank or ING might be a bit safer than the same deposit in Caja Madrid or Pireaus Bank. So why not shift some of that money, just to be on the safe side, before the next crisis hits the eurozone?

(click to enlarge)

A gradual shift of deposits out of Spain and Greece could spell trouble for those banks, even if the shift is well short of what could be called a bank run. As the chart above illustrates, Spain and Greece s saw their banks’ deposits steadily leaving town during 2011 and the first half of 2012. However, bank deposits in both countries stabilized in recent months, ever since the ECB’s unequivocal statement in July 2012. If people interpret this week’s events as undermining that crucial statement by the ECB last July — an interpretation that I certainly wouldn’t argue with — then we may expect to see the negative trend in peripheral bank deposits resume. And with it the periphery’s banking problems may resume as well.

The Eurozone Central Bank seems to have forgotten that one of the main functions of a central bank is to protect the solvency of the commercial banks. This principle applied in the UK until the passing of the Bank of England Act in 1998, one of the worst Acts of Parliament ever passed by a UK Labour Government.