Paul Krugman claims that should the much-dreaded bond vigilantes show up, they actually would be good for the economy. He notes that unlike Greece, the United States has its debt denominated in its own floating currency. Consequently, the appearance of bond vigilantes would lead to an expansionary decline in the value of the dollar, not a contractionary rise in interest rates. Tyler Cowen is not buying this story, but Nick Rowe sees some merit in it. I do too, but from a slightly different perspective.

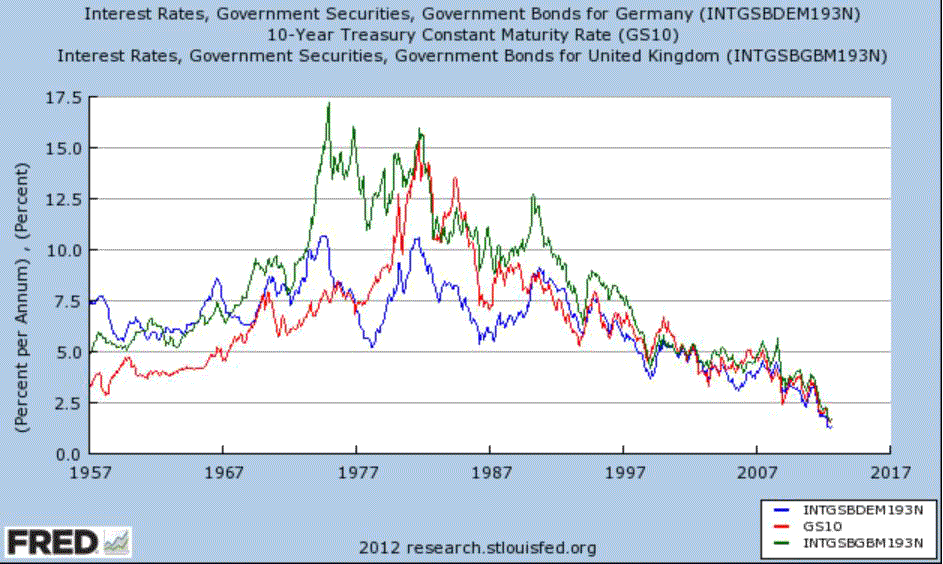

Currently, investors around the world have their portfolios inordinately weighted toward safe, liquid assets. This is because of the ongoing economic uncertainty caused by the Eurozone crisis, fiscal cliff, China slowdown, etc. They also have a seemingly insatiable demand for these safe assets as evidenced by the ongoing decline in their yields across the globe (see below). These developments, however, mean that investors are avoiding higher yielding, riskier assets more so than normal. Consequently, these unbalanced portfolios are suppressing asset prices, keeping household balance sheets weak, and ultimately are holding back robust aggregate nominal spending. Another way of saying this is that risk premiums are currently too high relative to fundamentals.

(click to enlarge)

The appearance of bond vigilantes would indicate their economic outlook has changed and are in the process are rebalancing their portfolios. This rebalancing, whether it was driven by higher expected inflation or higher expected growth, would catalyze more aggregate nominal expenditures and given the significant economic slack, more real economic growth. The problem, as noted by Nick Rowe, is that we want some portfolio rebalancing, but not too much That is why an nominal GDP level target is important. It would clearly set expectations on how much nominal income growth and, by implication, how much portfolio rebalancing would be allowed. In other words, a nominal GDP target would guarantee we get the just the right dose of bond vigilantism needed to shore up the recovery. And note that the recovery in nominal GDP would push up interest rates too. Using Paul Krugman’s terms, this would be an expansionary rise in interest rates. So let’s not fear bond vigilantes, but learn to manage their expectations in a way that will spark a real economic recovery.

(click to enlarge)

Leave a Reply