Among the plethora of post-election exit-poll results, the CNBC website highlights a particularly interesting response, linked from the mega-blog Instapundit with the title “Voters Worry More About Inflation Than You Think.” The CNBC article itself, written by Allison Linn, describes the poll results in more detail:

It’s no surprise that voters in Tuesday’s presidential election identified the economy as the No. 1 issue in the campaign, far ahead of health care and the federal budget deficit.

But it was a surprise that so many voters identified rising prices as the biggest economic problem they face.

Linn notes something of a disconnect between this view and the facts on the ground:

…inflation has generally been running well under 2 percent, and Federal Reserve bankers repeatedly have said they feel comfortable that low inflation allows them to keep interest rates at rock-bottom levels.

Yet in an exit poll of more than 25,000 voters conducted by NBC News, 37 percent identified rising prices as the biggest problem facing people like them.

Unemployment was cited by 38 percent, only slightly more than the number who said inflation was their top economic concern. Taxes were named by 14 percent and the housing market was the top concern of 8 percent.

The policy stakes on understanding these responses are pretty high. In the end, the cost of inflation comes in the form of how it may distort behavior and the allocation of resources. So the expectation or perception of significant inflation is at least as pernicious as the measurement itself.

But what, exactly, does this concern about “inflation” actually reflect? Probably not what we think. Some time ago, my colleagues Mike Bryan and Guhan Venkatu (from the Cleveland Fed) made note of “The Curiously Different Inflation Perspectives of Men and Women.” Their findings are pretty informative:

Over the past few years, the Federal Reserve Bank of Cleveland, with assistance from the Ohio State University, has studied household inflation perceptions and expectations using a monthly survey of approximately 500 Ohioans (the FRBC/OSU Inflation Psychology Survey). This survey, which records respondents’ perceptions of price changes over the past 12 months as well as their expectations for price changes over the next 12 months, has uncovered a surprising result. The data indicate that the public’s estimates and predictions of inflation are significantly and systematically related to the demographic characteristics of the respondents. People with high incomes perceive and anticipate much less inflation than people with low incomes, married people less than singles, whites less than nonwhites, and middle-aged people less than young people. This Commentary describes what is perhaps the most curious observation of all: Even after we hold constant income, age, education, race, and marital status, men and women hold very different views on the rate at which prices are changing.

…[S]tatistical tests reveal that even after we adjust for the respondents’ age, race, education, and income, women in our survey tended to think inflation was 1.9 percentage points higher than men. A similar examination of respondents’ predictions of future inflation yields the same basic result: After we account for other major demographic factors, on average, women expected prices to rise 2.1 percentage points more than men.

It is important to note that this result was not unique to the Cleveland Fed study:

An examination of survey data collected by the University of Michigan (which has recorded the inflation forecasts of U.S. households on a monthly basis since 1978) reveals that women consistently hold higher inflation expectations than men, even after we hold constant other important demographic characteristics of the respondent.

Most intriguing of all, the systematic overstatement of inflation by all consumers, relative to official statistics, and the difference in responses between men and women are not a result of ignorance about the facts, according to those official statistics:

In the August 2001 FRBC/OSU survey, we sought an answer to this question by asking, “Have you heard of the Consumer Price Index (CPI) before?” and “By about what percentage do you think the CPI went up (or down), on average, over the last 12 months?”

A significantly higher proportion of men had heard of the CPI compared to women (75 percent versus 61 percent, respectively). For those who had heard of the CPI, the average perception about how much it had risen over the past 12 months was surprisingly accurate—a perceived increase of 2.9 percent compared to an actual increase of 2.7 percent. It is also very interesting that men and women perceived the CPI’s growth rate nearly identically (2.8 percent versus 3.1 percent, respectively.) However, of those who knew of the CPI, the average perception of price increases was 6.7 percent. And even within the subgroup of respondents who knew of the CPI, men had a significantly lower perception of price increases than did women (6.0 percent vs. 7.4 percent). In other words, the public believes that prices are rising more than the CPI reports, and women more so than men.

There are a couple of hypotheses that could be advanced to explain results like this. One is that the conspiracy crowd is correct and the official statistics are rigged and vastly understate true inflation. But that wouldn’t get us anywhere near an understanding of why survey responses about inflation would be systematically different across men and women, higher- and low- income individuals, and just about any other demographic cuts we might make.

A second possibility it is that individuals’ responses reflect price changes in their own personal market basket, which may differ from that of the average urban wage earner whose habits are reflected in the Consumer Price Index (CPI).That might explain why any demographic sub group could arrive at different inflation perceptions, but it doesn’t explain why respondents as a whole systematically overstate inflation relative to the CPI.

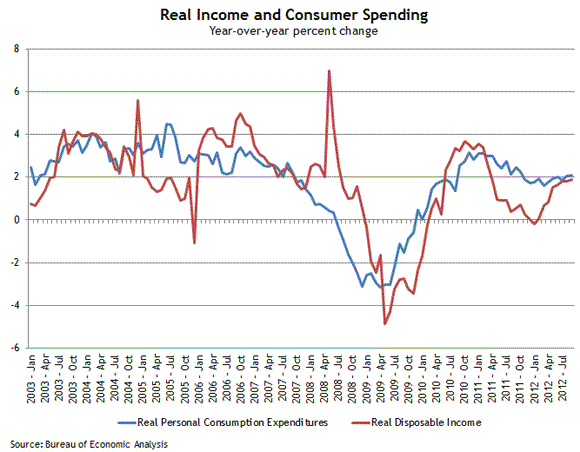

I think the most likely explanation is that the survey respondents are expressing a much different concern than whether they believe food, gas, autos, banking services, or whatever are increasing or are likely to increase faster than the official statistics indicate. My guess is that they are telling us that they are concerned that their real—or inflation-adjusted—incomes are not rising fast enough to comfortably sustain their desired spending:

As I noted, the policy stakes are high. In the current environment, the policy prescription for fighting an incipient rise in inflation expectations would be much different than one deployed to address the reality of the chart above. All the more reason to make sure we understand the questions we are asking and the responses we get back.

Just to be sure, we monitor inflation trends and inflation expectations from a number of perspectives: Treasury Inflation Protected Securities (TIPS), forecasts, and the Business Inflation Expectations (BIE) survey, to name just three. And all are available on the Atlanta Fed’s Inflation Project for the terminally curious to monitor with us.

Leave a Reply