With the unemployment rate still above 8% and some inflation measures below 2%, many people argue that the Fed is “missing on both sides of its dual mandate;” see, for example, Fed Harms Itself By Missing Goals.

Jim Bullard, president of the St. Louis Fed, has a different view, which he just published here: Patience Needed for Fed’s Dual Mandate.

My interpretation of his critique is as follows.

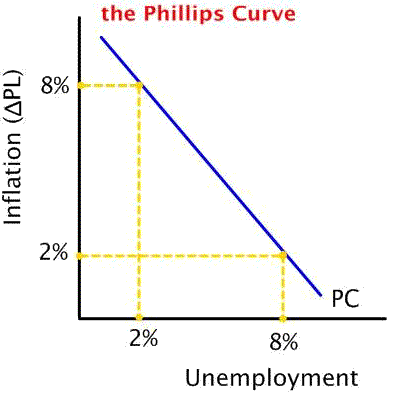

People who make this critique invariably organize their macroeconomic thinking along “Keynesian” (or New Keynesian) lines. An important pillar of this way of thinking is some version of the Phillips Curve (see here for Mike Bryan’s humorous critique of the concept). Here is what a Phillips curve is supposed to look like:

Now, imagine that the economy is hit by a large negative “aggregate demand shock.” Unemployment rises, and inflation falls–there is a movement along the PC, downward, from left to right (see diagram above).

Next, suppose that the Fed has the power to exploit the PC relationship (this is a questionable supposition, in my view, but it’s what people like to believe, so let’s run with it). What would the unemployment-inflation dynamic look like in response to such a shock under an optimal (or near optimal) monetary policy? (Bullard references the Smets and Wouters NK model: Shocks and Frictions in U.S. Business Cycles: A Bayesian DSGE Approach.)

Bullard’s suggests that a non-monotonic transition path for inflation is unlikely to be part of any optimal policy in a NK type model. The optimal transition dynamics are typically monotonic–think of the optimal transition path as a movement back up the PC in the diagram above. If this is true, then the optimal transition path necessarily has the Fed missing on both sides of its dual mandate.

Of course, conventional NK models frequently abstract from a lot of considerations that many people feel are important for understanding the recent recession and sluggish recovery. The optimal monetary policy may indeed dictate “inflation overshooting” in a different class of models. Please feel free to put forth your favorite candidate. Tell me why you think Bullard is wrong.

Leave a Reply