There has been a lot of Fedspeak over the last few days as policymakers expand upon the shift to open-ended QE. See Cardiff Garcia at FT Alphaville for an overview of some of the dovish talk, and see Pedro Da Costa at Reuters for some thoughts on the hawkish talk, described as a “vocal minority.” See also Reuters for an interview with St. Louis Federal Reserve President James Bullard, who claims that he would have voted against QE3:

“I would have voted against it based on the timing. I didn’t feel like we had a good enough case to make a major move at this juncture,” said Bullard, who has been viewed as a centrist on the spectrum of Fed officials, though in recent months he has sounded opinions that have sounded more hawkish as he has expressed doubts about the need for further stimulus.

Bullard does acknowledge his preference for open-ended QE, if he had believed it was needed:

Even so, Bullard said some of the contours of the plan, which has no set end date, were in keeping with how he thinks monetary policy should be conducted with interest rates already near zero. Leaving end dates off a bond buying program can make the policy “more effective,” he said.

Bullard is also reported to have expressed support for dropping the dual mandate, although I am not seeing a direct quote. Same for concerns about commodity prices:

He also voiced concern that QE3 could spill over into higher commodity prices, as happened with the previous rounds of Fed bond-buying, although he said the soft tone of the world economy would help curb price rises.

The reporter reaches the conclusion:

In discussing his views on more monetary stimulus, Bullard said, “We should take a little bit more (of a) wait-and-see posture.” His comments, in an interview with Reuters Insider, highlight potential dissent on the Fed’s policy committee next year when he will be a voting member.

Should we be concerned about this warning? I would say no. I think it is easy for Bullard to say that he would have dissented, but a lot harder to actually dissent if he was seated in the meeting. Indeed, he gets the best of both worlds – he gets to display his hawkish credentials by saying he would voted against QE without the pressure of the actual vote. Might he get more vocal next year? Maybe. I suspect his comments will be a function of which way the political winds are blowing. All of his comments to Reuters – anti-QE, concerns about commodity prices, desire to dump the employment mandate – sound like attempts to position himself for a role in a Republican Administration. The more he needs to position himself in that direction, the more hawkish he will appear.

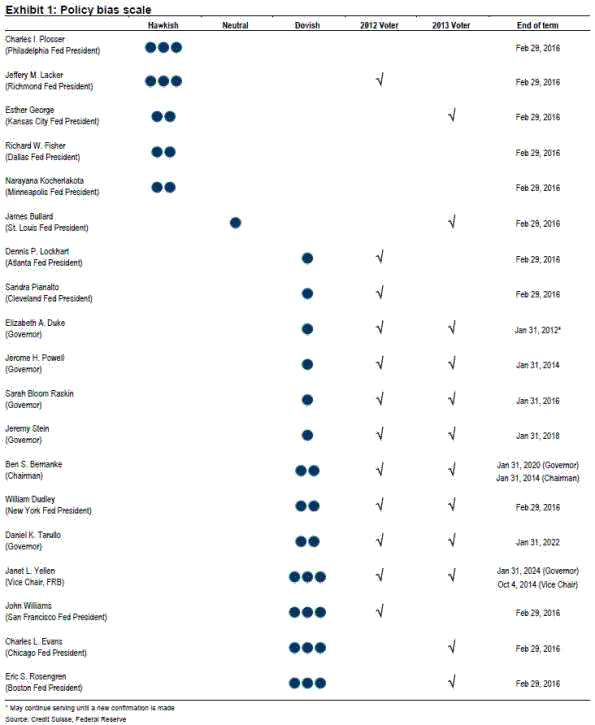

And note that fundamentally, whatever Bullard (or other hawks) say is for the time largely irrelevant. As a group, they were small to begin with, and by now have been intellectually marginalized. Via Cardiff Garcia, Credit Suisse provides a summary chart of policymakers:

(click to enlarge)

The hawks are all bark, no bite. They are more than overwhelmed by dovish-leaning policymakers, even if Bullard joins Kansas City Federal Reserve President Esther George in hawkish dissent. What remains important heading into 2013 (aside from the data, of course), is Federal Reserve Chairman Ben Bernanke. He can pull the moderates where he wants to go. And it obviously is not in a hawkish direction.

Bottom Line: Fed hawks are largely marginalized. Their views have not and will not have a significant impact on policy making. They will only appear to have an impact on policy if the data signals that a policy shift is needed. Given the current set of policymakers on the Fed, the hawks will only have a voice if Bernanke is replaced with one of their own. And that is when it would get interesting, as I am not sure that the moderates would follow a hawkish Chairman.

Leave a Reply