I spoke with Ben Levinsohn last week, as he’s a pretty good guy for the WSJ who writes about low vol on occasion. He took this snippet out of our conversation:

“If you want low volatility, you should get utilities and not worry about it,” says Eric Falkenstein

Alas, that’s not exactly what I meant, though I did say it.

What I was trying to say was that while a low volatility strategy has more of a utility weighting than the S&P, your average low vol investors should not to worry about it. A low volatility focus dominates the indices, which dominate active portfolios, which dominate picking individual stocks. So the ‘low vol’ focus should be encouraged.

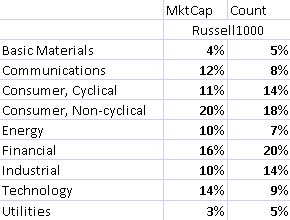

Here’s the weighting of the Russell 1000 by industry sector, by value-weighting and count:

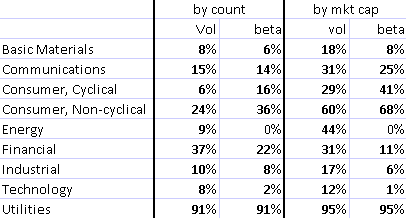

Now, if you apply a filter so you grab the bottom 20% of stocks with the lowest beta or volatility, here’s the allocation you get, both by count (equal weighted), or market cap (if you allocate via market cap), where the percents are relative to the Russel, so that 20% would be neutral (because I’m choosing the bottom 20% of stocks):

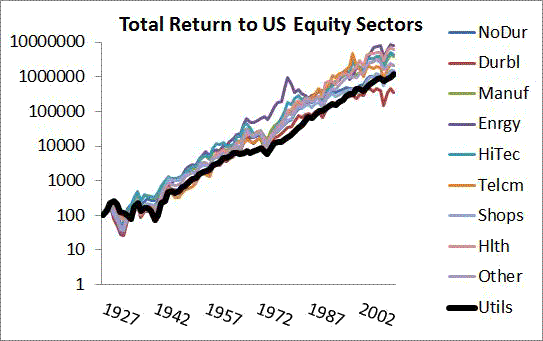

There are several ways you can make low vol better, and utilities, historically, don’t seem to be the secret sauce of low volatility. Below is the total return index for 10 major indices since 1927, and utilities are near the bottom in total return. As low vol has historically out-returned high volatility, this clearly suggests utilities are a drag on the strategy.

Yet, if you get worried about this nuance, you probably will get led down the path of gilding the lilly, making thing worse in an earnest attempt to do things better. I mean, if you restrict utilities, what next? Value (because that overlays one’s value allocation)? How about industry caps in general? While I think there are better ways to play low volatility than SPLV, for most people this is their best play.

I don’t talk about tactics I think really add alpha because really good specific ideas are better kept off the web: the masses will dismiss them, and smart people will steal them without attribution. Big strategies are useful to discuss in public because they are interesting and too big to be a secret anyway.

As most people screw things up doing it themselves, usually by adding a signature flare (most new ideas are bad, after all), most people will ruin the benefits of low vol by noting that utilities detract from low vol. In practice people don’t stop with just one refinement, to their detriment.

If you can afford or know someone really good (ie, in the top decile), do it fancy, but otherwise, simpler is better.

Leave a Reply