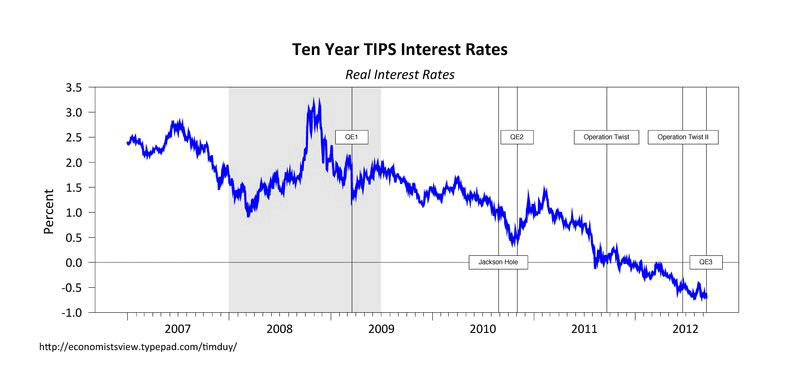

Weighing on my mind is the possibility that we do not lift off the zero bound – in other words, we don’t normalize the economic environment – before the next recession hits. When I say normalize the environment, I am thinking in the terms David Beckworth describes here. Begin with the premise that interest rates are abnormally low. I can’t see how anyone can not come to that conclusion with ten year TIPS in negative territory:

(click to enlarge)

Rather than seeing the Federal Reserve’s action as the cause of the low interest rate environment, I tend to think it was the Federal Reserve’s inaction. If monetary policy was gaining traction, interest rates should rise, forcing the Fed to follow rates up. Instead, Fed policy continues to follow interest rates down.

Looking at the Fed’s extended guidance, they do not see the need to raise short term interest rates until mid-2015. June 2015 would mark 90 months since the peak of the last business cycle in December 2007. The average peak-to-peak cycle of the last three recessions 96 months, the average since 1945 is 66 months. Now, I don’t think you can say that the probability of recession in the next month is a factor of the time since the last recession. But you can say that given past business cycle timing, it is perfectly reasonable to believe that the next recession will hit before we lift off the zero bound. Moreover, it would be relatively uncommon for the peak-to-peak cycle to last more than 90 months. Only 4 of the last 11 cycles have exceeded this length of time.

So I am getting a little nervous that we will not lift off from the zero bound before the next recession hits. Or maybe the attempt to lift the economy off the zero bound is the trigger of that recession. In either case, I am thinking it would be very bad to be still at the zero bound when that recession hits. So I am wondering what is the equilibrium path that returns the US economy to a normal interest rate environment. Furthermore, can the Fed push the economy to such a path by itself, or is fiscal cooperation required? I don’t have answers to these questions, but my suspicion is that the job would be easier with coordinated fiscal and monetary policies.

Leave a Reply