In keeping with this week’s theme of revisiting ghosts of valuations past, I decided to take a look at another fallen angel, Groupon (GRPN). The stock has collapsed to $4.44 from its post-IPO high of $29 and investors and employees seem to be fleeing from the exits. If you are a contrarian with a strong stomach, it would like the stars are aligned for some bottom fishing but is Groupon a buy, even at this discounted price?

To make this assessment, I decided to take a look at my posts on Groupon from last year:

- In my very first post on Groupon in June 2011, I looked at their attempt to move customer acquisition costs from the operating expense to capital expenditures column. While I was sympathetic to the general argument that operating expenses that create benefits over many years (such as R&D, exploration costs and even customer acquisition expenses) should be treated as capital expenditures, I was skeptical in Groupon’s case since there was little evidence that Groupon’s acquired customers stayed on for long periods and also because Groupon did not follow through fully and treat customers as assets (and amortize or depreciate these assets over time).

- In my second post in October 2011, I looked at Groupon (as well as Google and Green Mountain) with an eye towards potential growth, using four tests: the feasibility of the growth given the overall market served by each company, the capacity to scale up growth (i.e., maintain growth as the companies get bigger), the value created by that growth and the effect of management credibility on how the market perceives that growth.

- In my third post on November 2, 2011, I valued Groupon at the time of the acquisition. Using “aggressive” assumptions on revenue growth (50% annually for first 5 years, scaling down to mature growth by year 10) and pre-tax operating margin (23%), I estimated a value of $14.62 per share, below the $16-$20 range that investment bankers were touting.

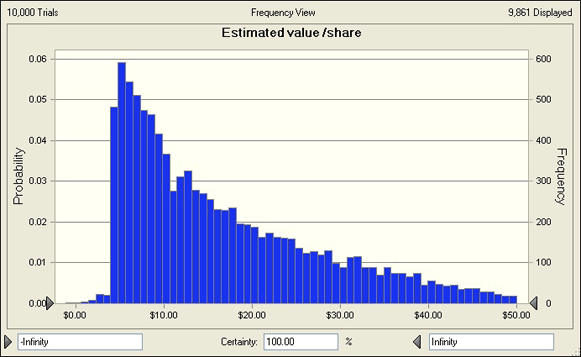

- The stock did go public on November 3, 2011, at $20/share, and jumped to $28 by the end of the day. My fourth post on Groupon, on November 4, 2011, looked at the company in the context of a discussion of the value of growth. For growth to add value, I argued that it has to be accompanied by “excess returns”, which, in turn, require competitive advantages or barriers to entry. Looking at Groupon’s business model, I could not think of any significant barriers to competition that would prevent others from entering the market and eating away at Groupon’s margins. Using a simulation, I estimated the following distribution for value/share for Groupon in November 2011 and argued that the stock was more likely to be worth less than $10/share than it was to be be worth $30:

A year later, it is clear that I under estimated how quickly any competitive advantages that Groupon’s first mover status gave them would be eroded. This is clear not only from perusing my email box every morning (and removing the dozen emails from different deal-of-the-day purveyors) but also in Groupon’s financial results. As the most recent earnings report makes clear, revenue growth has slowed, profitability has lagged and the stock price collapse is in reaction these changes.

As I revisited my valuation, as with Facebook (FB), I had to caution myself not to overreact, but the news, as I see it, is far more dire for Groupon than it is for Facebook. While Facebook’s results were disappointing in terms of converting potential to profits quickly, the potential (from their vast user base and the information they have on these users) still remains. In Groupon’s case, where the business model was clearer at the time of the IPO, the business model has collapsed and it is difficult to see what the company can do to set itself apart from the competition and make money at the same time. As a result, the changes I made in my Groupon valuation are more dramatic than the changes I made in my Facebook valuation. My base year numbers reflect their most recent quarterly filing, with trailing 12-month revenues of $1.965 billion and operating income of $71 million. My forecasted revenue growth rate is 25% (leading to revenues in 2022 of $10.3 billion, as contrasted with my earlier forecast of $25.4 billion), my target margin is 12% (down from my year-ago estimate of 23%) and my sales/capital ratio is now down to 1.25 (from a year-ago estimate of 2.00). The end result is a value per share of $4.07, which makes the stock, at best, a fairly priced stock. In fact, if you bring in the likelihood that the firm may not make it through its growth pains in the spreadsheet, the value per share drops even further. As with the Facebook valuation, you can download my spreadsheet and put your own estimates in… I have a shared Google spreadsheet for those of you who want to share your numbers…

There are two broader point that are worth making here.

- A dramatic stock price drop is not always a buying opportunity: Most young growth stocks are subject to gyrations and it is not uncommon to see growth stocks plummet, when they don’t meet the lofty expectations that investors have for them, and we have seen this happen to both Facebook and Groupon. In some cases, investors over react and push the price down far more than they should and that is the basis for my pitch I made for friending Facebook in my last post. In some cases, though, the stock price collapse is well-deserved and that is my rationale for avoiding Groupon.

- Intrinsic valuations can (and should) change over time: There is deeply held belief, at least in some quarters, that intrinsic valuations are stable and don’t change over time. While that may be true in many companies and most time periods, there are three exceptions. The first is a dramatic change in the macro environment. My intrinsic valuations for almost all companies changed between August 2012 and October 2012, as the market price of risk (in the form of equity risk premiums and default spreads) increased dramatically in the aftermath of the banking crisis. The second is when accounting fraud is uncovered and key numbers have to be restated. The third is with young growth companies where the premise on which the value of growth is based – that it is scalable, defensible and valuable – is called into question. It is the third exception that applies to Groupon and I feel comfortable lowering the value per share from $14.82 a year ago to $4.07 today.

Stupid! Why didn’t you see it coming.