“The market can remain irrational longer than you can remain solvent” – John Maynard Keynes

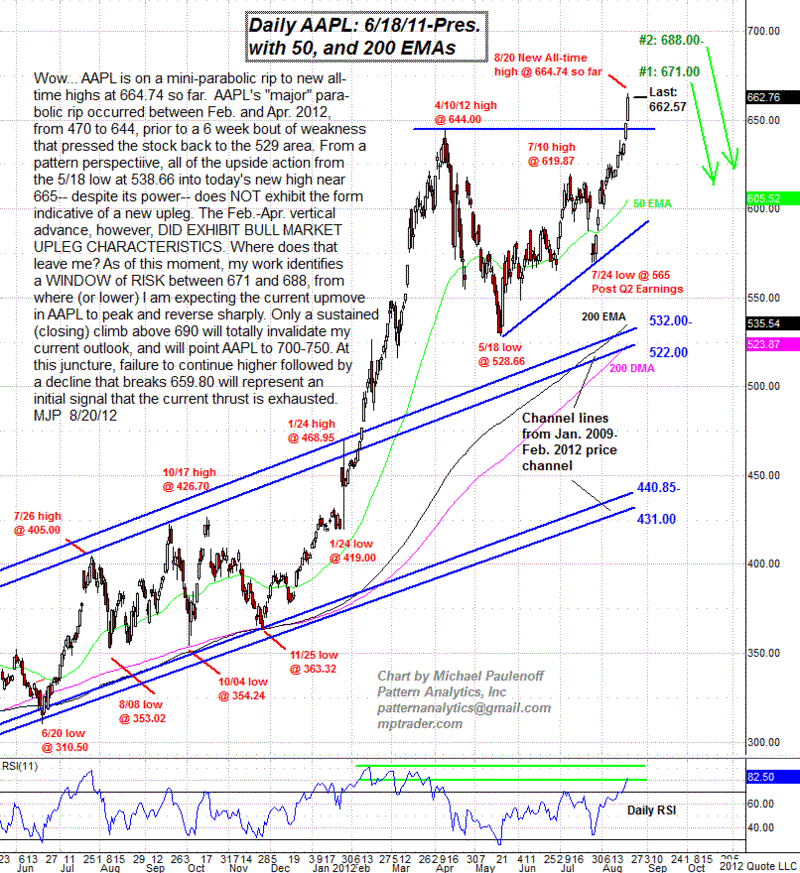

When AAPL ran up into an interim peak in March, I asked whether AAPL has peaked? I used a chart which showed two potential pivots: at 593-601, which formed the interim top; and 668-677. We have now come to 675 and fallen off a bit. Apple’s next big announcement is coming, and often stocks run up on rumor and fall on news. That may be all this is; or, is this the peak?

If you expand this thumbnail of AAPL’s incredible run up, courtesy SlopeofHope, you will see a classic parabolic rise pattern. We saw it in 2008 with oil, which shot up to $147 a barrel then fell like a drill bit straight down over the next six months to $32. We saw it with the NASDAQ from late 1998 to early 2000, where it too fell like a dead cat from April to October of that year. And of course in stock after stock and commodity after commodity.

AAPL has now become the highest market cap in history, at least in nominal dollars. In inflation adjusted dollars, Microsoft (MSFT) was worth more in 1999, and IBM was much higher in 1967. Still, a seminal achievement for AAPL, and a warning flag for investors.

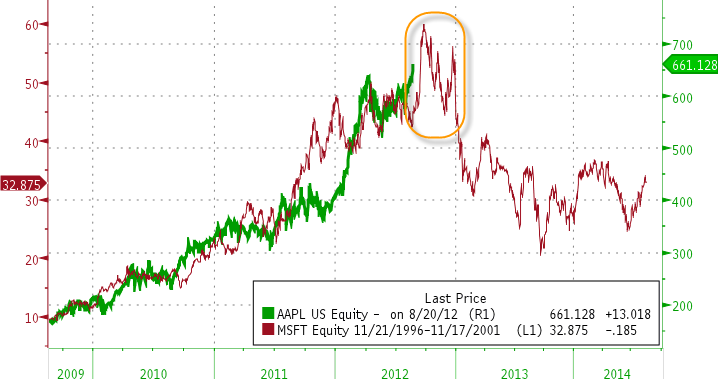

I ran a comparison of Google’s thrust to its peak vs. Apple (AAPL) in my prior post, supporting the argument of a peak based on analogy. Here is the comparison to Microsoft’s thrust up during the dot-com bubble, which shows Apple may have more room to run:

(click to enlarge)

Word of caution: parabolic thrusts end badly, but by their very nature (underlying stampede of the herd) are unpredictable of how high they will run and when they will end. Arguing from a few analogies, like Google (GOOG) and Microsoft, is very thin to base a trade upon. The dynamic for Google several years ago or Microsoft in 1999 were very different than today. This is not an argument for “this time it is different,” just a reflection of the über momentum behind parabolic rises, and how the emotion of greed (or for money managers, fear of falling behind) can run for a longer time than a short can stay solvent. Particularly so in this environment, of a Global Scramble for Yield; money managers have to have AAPL to keep up with their brethren, and boy do they enjoy the outsized yields so far.

A little technical analysis may help. Here is the updated chart from the last report, with predicted levels of resistance, now shifted a bit to 671-688, a range we hit already:

(click to enlarge)

Yes, I saw this too. Add an inflationary curve and Apple has 150-250 pts to run. Another thing to consider is the season. If you think it’s hot now… What do you think everyone will buy for the holidays. My guess is a lot of apple gifts. Furthermore, the expansion of iTunes which is hardly mentioned. It’s not even considered in the numbers. I think we might be at the base of a parabolic shift. Scary thought

Apple never has been a chart company, it’s been an EARNINGS company! Apple will blow through $700 this year, and $1,000 next year. If the iPhone 5 sells as much as its expected to on top of Apple dominating every other market and PC users switching to macs at incredible rates, then $1,000 a share isnt even a high price! It’s just a lot of money.

While the iPhone has and will continue to be the force mainly driving the parabola, there is some concern that the space between the iPhone 5 and the “5s” or “6” might not be as short as it has been in recent iterations. While many analysts immediately dismiss the impact of the iPad on profits, the combination of a tweaked “new iPad” and an iPad mini, combined with an accelerating tablet-PC replacement rate, could sustain AAPL growth and profits despite phone-market slowdowns. For what people want a larger-screen phone (like the Galaxy S3), one may be able to purchase a larger wi-fi iPad mini without changing one’s data plan, capitalizing on the ubiquity of wi-fi, especially on college campuses, homes, offices and public places. Those iPads will fuel an iTunes/App-store profit explosion. Amazon recently attempted to get out ahead of the media-sales curve with software that detected when an iPad connected to their site, pushing their Kindle app.

Maybe so, but can you show me another large listed company with Apple’s growth selling at 11X forward earnings??? Maria Bartiromo amuses me with her “concerns” about ” what about ten years from now”

I think Apple goes to $750 by year end and then we wait and see, but IF the I5 and Mini are as big as many analysts think, …….