Facebook (FB) returned to the headlines on Friday, after it’s stock price dropped below $20. At it’s closing pricing of $19 on August 17, Facebook was trading at roughly half it’s IPO offering price. Investors, analysts and journalists are all looking for the reason for the collapse and some at least seem to have found a ready target: the price drop, they argue, is the result of the “unlocking” of restrictions on insiders selling shares. The problem with this explanation is that it has never been a secret that insiders in Facebook would be able to sell shares starting August 16 and I would wager that no one would have even noticed the end of the lockup period, if the IPO had gone well and the stock were trading at $ 55/share. So, what is going on with Facebook? Why has its stock price plunged over the last few weeks? And is the stock cheap at $19?

The story so far…

As we look back at 2012, it is quite clear that Facebook has held us in its thrall (and not always in a good way) through much of the year and my posts over the year on the company reflect that fascination. Rather than cover up my paper trail, let me draw attention to it (warts and all):

- S1 Filing (February 2012): In my first post on Facebook this year, right after Facebook filed its financials (S1) with the SEC, I valued Facebook at $28/share (or $70 billion). I based this valuation on the company’s immense potential (its vast user base and the information it had about these users), but was concerned about the absence of a clear business plan (to convert users to revenues), the overhang from insiders stockholdings/options (yes, you could see the lock up period ending in February) and the abysmal corporate governance.

- Playing the IPO pop game (February 2012): In response to a wave of articles that seemed to suggest that investing in the Facebook IPO (at the offering price) would be a sure road to profit, I tried to provide some history on the IPO game in my second post on Facebook, noting that while it was was true that investing in the average IPO does generate a pop for investors, this pop is not guaranteed and that the IPO game can be a loser’s game.

- The day before the IPO (May 2012): On the day before the IPO, I posted on what I saw as the hubris of those involved in the IPO process – the investment bankers, the company (Facebook) itself and the institutional investors, who all seemed to think that they could lead the market by to wherever they wanted to go. I updated my valuation of Facebook to about $27 a share and contended that the stock would open with a relatively small pop (that the bankers would get the pricing right) but that the stock was overvalued for longer term investors.

- The post-IPO assessment (May 2012): The stock opened (late because of the NASDAQ technical problems) at about $42 and very quickly lost ground over the day to end the day at below the offering price. I posted my rationale for the momentum shift and argued that a great deal of the blame could be laid at the feet of the company and its bankers, who essentially took momentum for granted. I also ended the post by arguing that the switch in momentum could very well lead take the stock in the other direction, from over valued to under valued.

An updated valuation

If Facebook was over valued at $38, relative to the estimated value of $27/share, is it under valued at $19? To address this question, I revisited my Facebook valuation from May and looked at what I have learned about the company (for the better or worse) since. Has there been enough information that has come out about the firm that could have caused the intrinsic value (at least as I measure it) to drop below $19? The biggest piece of financial information that has emerged on Facebook has been one quarterly earnings report a few weeks ago and it seems to me that not much has changed on either side of the ledger since February. The earnings report was a disappointment to markets, revealing less revenue growth than anticipated and an operating loss, largely as a result of share compensation expenses that were recognized when restricted stock units owned by employees were recognized at the time of the IPO. Facebook remains a company with vast potential (their user base has not shrunk), no clear business plan (is it going to be advertising, product sales or something else) and poor corporate governance. I had not expected any of these issues to be resolved in the one quarterly report and they were not. I did make some adjustments to my valuation: (a) lowering my revenue growth (with my 2022 revenue estimates dropping by about 10%, relative to my May estimates, (b) reducing the operating margin from 35% to 32% to reflect the higher expenses and (c) reducing my sales to capital ratio from 1.50 to 1.20 to incorporate the higher cost of acquisition driven growth. With these changes, my intrinsic value for Facebook with the updated information is $23.94, a drop of just over 10% from my May 2012 estimate.

So, why did the price drop so much? There are several possible reasons. The first is that my estimate of intrinsic value is completely wrong, that the true value for the company has always been in the low teens and that the market is correcting its initial mistake. The second is that most investors in Facebook don’t know what the value of the company is and don’t care a hoot about it. Instead, they are pricing (rather than valuing) the stock, reacting to the “surprise” in each news story and to how other investors in the market are responding to that story. This, after all, is the nature of momentum investing, with positive surprises getting magnified by the crowd into unrealistic price jumps and the negative surprises into catastrophic drops. I know that analysts have turned bearish on the stock but since many of these analysts assured me that Facebook was a steal at $38/share, I am not inclined to put much weight on their prognostications. In fact, they very fact that they are turning against the stock may be a positive indicator.

Time to buy?

Now that the stock is at $19, about $5 below my estimate of intrinsic value, would I buy? To make that judgment, I considered three factors.

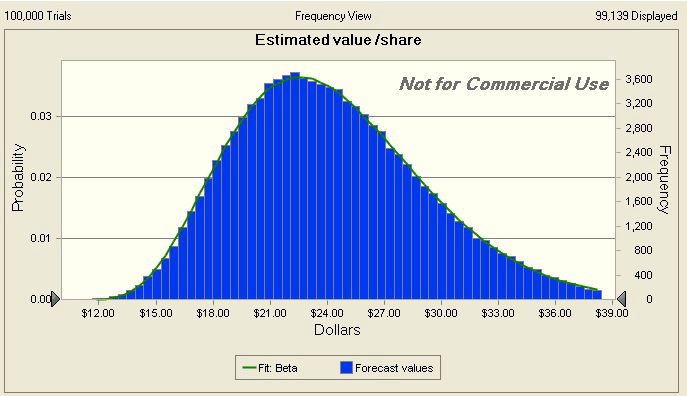

1. My value could be over stated: I understand that this is a risky investment and that my estimate of value could be hopelessly wrong. In fact, I followed up my intrinsic valuation with a simulation, where I looked at the distribution of intrinsic value, allowing revenue growth, margins and cost of capital to vary.

(click to enlarge)

Based on my assumptions, there is an 80% chance that the stock is under valued at $19 a share and an almost 85% chance that it is under valued at $18 a share.

2. Management is not going to change: The corporate governance issue is the one that I have the most trouble overcoming. The structure of the voting rights in the company ensure that there is little that stockholders can do to influence how this company is run and that can be a potential problem if it locks itself into a self-destructive path. Calling for Mark Zuckerberg to step down or share power, as an article in the Los Angeles times did, are completely unrealistic. The Russians have a better shot at getting rid of Vlad Putin than Facebook stockholders have of displacing Zuckerberg. For some, this may be a deal breaker, and it came close to being one for me.3. Vindication, even if I am right, will not come quickly: Markets know no fury to match that of momentum investors scorned, and these investors tend to turn with a vengeance on the companies that disappoint them. Put in stark terms, it is entirely possible that my valuation of Facebook could be right but that the stock price could continue to keep dropping as investors bail out. Eventually, the “intrinsic” truths will emerge, but it may be a long time coming.

My conclusion is that Facebook is not quite at the threshold of being a buy yet, but it is getting close. I have a limit buy order for the stock at a price of $18. I would be interested in seeing where you stand on the stock and you are welcome to enter your estimate of intrinsic value for the stock and your threshold for buying the stock in the shared Google spreadsheet.

Leave a Reply