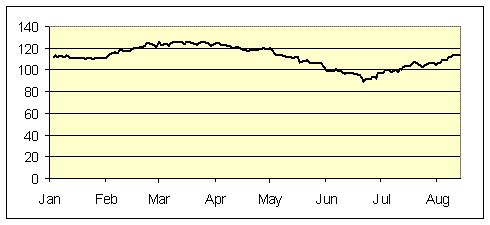

The price of Brent crude oil fell $35/barrel between April and June. But increases this summer have taken about $25 of that back.

Price of Brent in dollars per barrel, Jan 1 to Aug 13. Data source: BP.

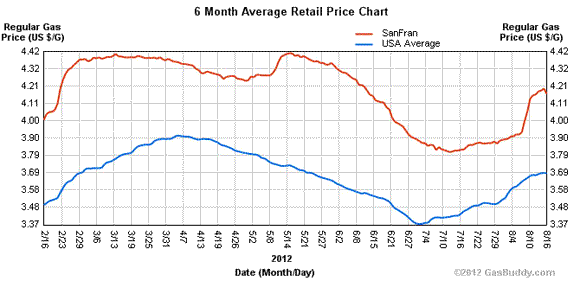

The increase in crude oil prices also wiped out most of the gains realized by American gasoline consumers this spring. Here in California, the gasoline price spike back up has been significantly bigger than the national average due to a fire at a major San Francisco Bay refinery.

New Jersey Historical Gas Price Charts Provided by GasBuddy.com

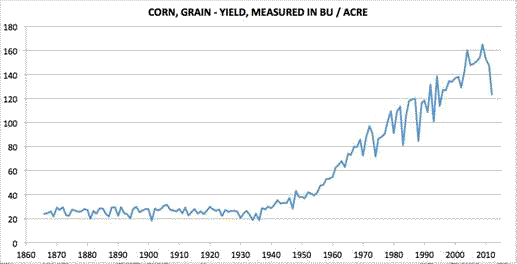

In coming months, these developments may offset some of the recent softness in U.S. inflation. Another contributing factor to that could come from the big drop in corn production resulting from drought in much of the U.S., which will matter for both food and fuel prices. Hopefully those problems will at least provide new momentum for repeal of the ethanol mandate.

U.S. corn yield per acre, 1866 to 2012 (estimated). Source: Early Warning.

What’s behind the rise in the price of Brent? Some financial reports have stressed rising tensions with Iran. However, one objective, if imperfect, quantitative measure of that comes from the market price of Intrade’s contract for an imminent attack on Iran. This has moved relatively little since April.

Price of Intrade contract for USA and/or Israel to execute an overt Air Strike against Iran before Dec 31, 2012.

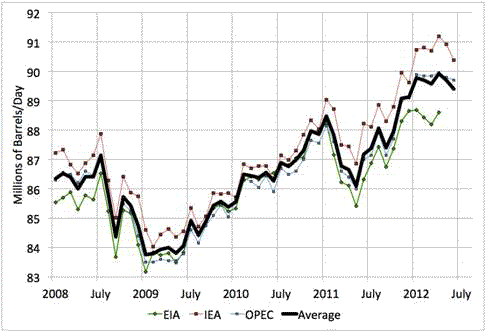

Another reason may be that total world oil production (including natural gas liquids and biofuels) has been stagnant since January, though at a level 3-1/2 million barrels/day higher than during the Libyan cutbacks in 2011, and 2 mb/d above the pre-Libyan peak in January 2011.

Estimates of world oil production. Source: Early Warning.

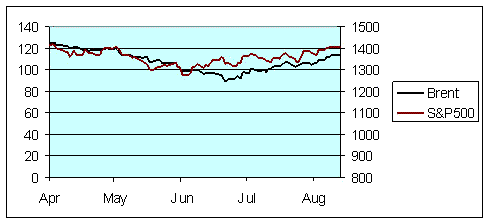

I believe that the most important factor driving oil prices recently has been changing assessments of how strong the world economy will perform over the next 6 months. The decline in oil prices in April-June and the subsequent rebound is mirrored in stock indexes like the S&P500. A stronger economy should mean both higher corporate profits and higher demand for oil. Markets are apparently betting that favorable economic trends in places like the U.S. and China are enough to outweigh the discouraging numbers coming out of Europe.

Price of Brent (dollars per barrel, left scale, from BP) and U.S. S&P500 index (right scale, from FRED), Apr 1 to Aug 13. Note percent moves in oil prices are larger than those for stock prices.

Whether markets have that right remains to be seen.

Leave a Reply