Take a look at Amrbose Evans-Pritchard’s latest piece on the Chinese economy. He quotes Charles Dumas of Lombard Street Research,

“The hard landing has happened,” said Charles Dumas from Lombard Street Research. “We don’t believe official data. We think GDP slowed to a 1pc rate in the second quarter”…

“This was the moment when stimulus was supposed to bite. It didn’t,” said Global Insight. Critics say Beijing let the property boom go too far and then hit the brakes too hard last year. Monetary tightening led to a contraction in real M1 money. The delayed effects kicked in this year just as Europe fell back into recession and the US slowed abruptly.

The Politburo has thrown all engines into reverse throttle. The reserve asset requirement for banks has been cut and regions have been given the green light for another blitz of eye-watering stimulus financed by credit from state banks. Wei Yao from Societe Generale said: “The bottoming-out process is taking even longer than we anticipated. The easing policies announced so far have not fully passed through to the real economy.

Reflating the credit bubble and building a few more ghost cities in order to reignite growth may be easier in a state-controlled economy than it is, say, in the U.S., but surely it won’t be an easy task even for the Chinese.

As is Europe, the China question is going to be around for the medium term and will have an outsized impact on the trajectory of risk assets over the next few years. Of course, interrupted by counter trend moves such as markets getting to lathered up over quantitative easing and directed credit expansion or even bouts of excessive pessimism. The key will be to filter out the noise and focus on the fundamentals that determine the trend. Not an easy task, but essential for survival.

It’s also interesting, and Evans-Pritchard makes the point in his piece, that policymakers in China now have to worry about capital flight as they weaken the currency to stimulate growth.

China Securities Journal confirmed this week that Beijing is steering the currency lower to cushion the shock. “The renminbi has entered a period of depreciation,” it said, adding that this could cause short-term capital outflows – running at $110bn in the second quarter – but the overall effect will be “beneficial, by enhancing exports.”

The policy risks a serious confrontation with Washington. “If they do the same old thing and slam down a few more roads to the Gobi desert they will end up with stagflation. They need Thatcherism to get out of this,” said Mr Dumas.

AHH! Cheaper goods at Costco and WalMart!

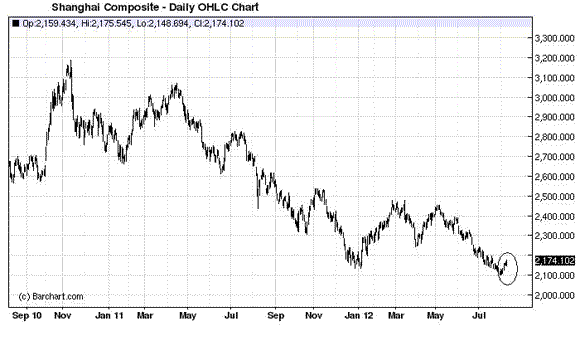

Note the bounce in the Shanghai over the past few days. It’s still got a lot of work to do to reverse the downtrend.

Leave a Reply