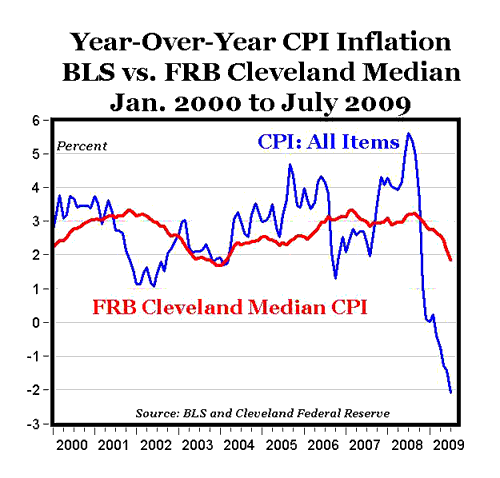

The BLS reported today that annual standard CPI inflation (deflation) from July 2008 to July 2009 was -2.10% (see chart above, blue line), mostly because of a -28.1% decrease in energy prices and a -14.1% decrease in transportation prices from a year ago (when gas was $4 per gallon and oil was $130 per barrel).

In contrast, the Cleveland Fed reported today that its adjusted, Median CPI increased by +1.8% year-to-year through July 2009 (see chart above, red line), similar to the BLS’ +1.5% annual “core inflation rate” for July based on the “CPI less food and energy.”

The Cleveland Fed has been studying and reporting median CPI for a long time, here is a paper from 1991 on “Median Price Changes: An Alternative Approach to Measuring Current Monetary Inflation,” which concluded that:

Differences between changes in the CPI and the median consumer price change underscore the impact of the distribution of price movements on our monthly interpretation of inflation. The median price change is a potentially useful indicator of current monetary inflation because it minimizes, in a nonsubjective way, the influence of these transitory relative price movements.

As Greg Mankiw reported on his blog several months ago:

The average of any data set can be thrown off by a few extreme outliers; the median is a more robust statistic to estimate the central tendency in the data. Right now, the two measures of inflation are diverging substantially. The standard CPI shows deflation over the past year, but that average is due to a few anomalous sectors, such as energy. If you look at the median CPI, which shows what a more typical price is doing, the inflation rate does not look very unusual.

MP: There are some concerns about future inflation from the expansionsary monetary policy in 2008 that doubled the monetary base, but that loose monetary policy certainly hasn’t yet started showing up in the median CPI inflation, or CPI inflation less energy and food. Unless and until median CPI inflation and core CPI inflation start to show inflationary signs, we really won’t have any real inflationary pressures to worry about.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply