Cisco Systems (NASDAQ:CSCO) is getting some analyst love this morning as both Piper Jaffray and Goldman Sachs are upgrading the stock.

– Interestingly, both firms say their checks revealed better than expected enterprise demand

*Piper Jaffray is upgrading CSCO to Overweight from Neutral with a $22 price target (prev. $20) saying they believe Cisco will report respectable FQ4 results with revenues inline with consensus, but better margins and cost controls providing upside to EPS.

Their confidence is based on proprietary channel checks and data points from distributors, coupled with Cisco’s recent improved execution. Firm expects Cisco will provide some cautious commentary regarding macro headwinds in Europe and the Fed vertical, but believe these concerns are already factored into expectations and the current stock valuation. They believe CSCO’s stock will work higher with investor interest in networking stocks returning and estimates likely moving higher (accretive acquisition and cost controls). Piper also also believes CSCO’s stock offers downside protection if markets turn negative with an attractive valuation (5.5x CY13 EPS ex-cash) and nearly 2% dividend yield.

Favorable Channel Checks – Based on proprietary channel checks, data points from distributors and their recent VARs survey, Piper believes Cisco will meet or slightly beat revenue expectations and tight cost controls should drive better than expected EPS results. They anticipate Enterprise sales were above plan, with the sluggish sales from service providers preventing limiting upside in the quarter.

2H Carrier Expectations – Piper believes 2H spending from North American service providers will increase over the 1H. While the rate of growth is likely below historical trends, they believe this will aid Cisco’s ability to exceed the 2H estimates that are currently reflecting below historical seasonality.

Firm believes CSCO shares will trade higher throughout the remainder of CY12 given improving investor sentiment and upward EPS revisions.

*Goldman Sachs is adding CSCO to their Conviction Buy Listi with a $24 price target representing 40% return potential. According to the firm they believe believe its fundamentals are inflecting positively, with both their recent IT Survey and their just-published channel survey pointing to stronger than expected growth in enterprise networking, and switching in particular, as well as to a stronger competitive position for Cisco.

Moreover, North America capex appears set for above-seasonal growth in 2H 2012. Separately, they think longer-term concerns such as software-defined networking (SDN) are overdone, with Cisco’s 1.3X EV/S implying the market is pricing in rapid margin degradation from the current 28%, which they view as unlikely.

Catalyst

Goldman expects Street estimates for Cisco to move up post F4Q (Jul) earnings next week, and their next two quarters’ EPS estimates are 6-7% above consensus on stronger growth in switching (due to the 10 Gb upgrade cycle) and routing (100 Gb upgrade cycle in core, share gains in edge), cost controls, and accretion from NDS (GSe $0.05 in FY13), which the Street hasn’t yet modeled. They also think Cisco can gain share in service provider video (8% of sales) given Google’s reported plans to sell Motorola Mobility’s set-top box business. Further out, Goldman expects Cisco’s analyst day in September and upcoming investor conferences to clarify its SDN strategy and alleviate investor fears of imminent and significant margin declines, which they expect will lift its multiple to low double digits, consistent with their 8.5% EPS CAGR expectation for CY2011-14.

Enterprise spending on network equipment is on more solid footing than feared

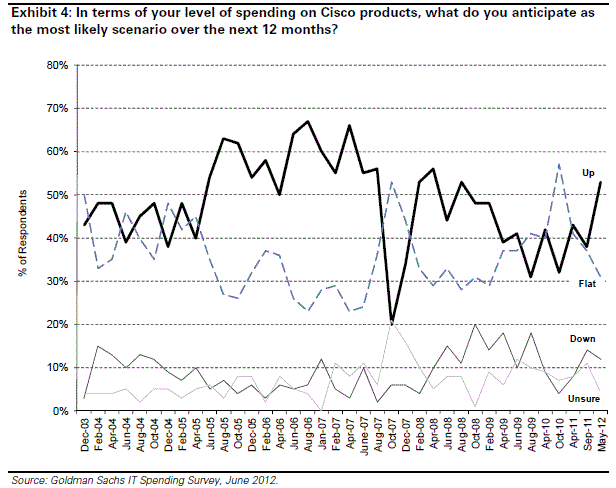

While there is still a high level of consternation among investors on end demand trends in the networking segment, recent datapoints suggest that demand is better than expected. Goldman’s June IT survey, which polls 100 IT executives from Global 2000 companies, showed that 53% of respondents expect to increase their spending with Cisco over the next 12 months. Importantly, this represents the highest level since 2H 2008, putting this data series back into the 50-70% range that they have historically considered “healthy” for Cisco. Meanwhile, the percentage of respondents expecting spend to be flat or down declined meaningfully since the firm last asked that question in September 2011. For context, enterprise spending (not including SMB) drives about a third of Cisco’s bookings.

Similarly, Goldman’s just published VAR survey points to stronger than expected growth for network infrastructure in 2012 and for Ethernet switching in particular. Recall that VARs are particularly important for Cisco, given that about 80% of its revenues come from the channel.

Notablecalls: This could be something – two separate firms out with positive channel checks. Goldman is actually making a positive sector call with a survey report titled “Channel survey shows surprising strength; Buy CSCO and ARUN”.

Definitely out-of-consensus stuff.

I expect CSCO to see meaningful buy interest in the n-t. The stock could trade close to $18 today if the tape cooperates.

Leave a Reply