Is anyone else bothered by the following: In the opening minutes of A New Hope, C3-PO warns R2-D2 that “There will be no escape for the Princess this time.” Then presumably less than 24 hours later when Luke stumbles accross the hologram of Leia begging for help from Obi-Wan, C3-PO seems to not know who she is:

LUKE: Who is she? She’s beautiful.

THREEPIO: I’m afraid I’m not quite sure, sir.

LEIA: Help me, Obi-Wan Kenobi…

THREEPIO: I think she was a passenger on our last voyage. A person of some importance, sir — I believe.

Maybe this is what you get for seeing a movie 498 times…

Anyway back to economics. Merrill Lynch is out with a intriguing analysis in their latest Credit Market Strategist. “The Myth of the Overleveraged Consumer.” Before you dismiss this as blindly bullish bullshit from the Bull, let me tell you that the report isn’t terribly rosy in its conclusion. But it does cause one to really think about what drives consumption in the U.S.

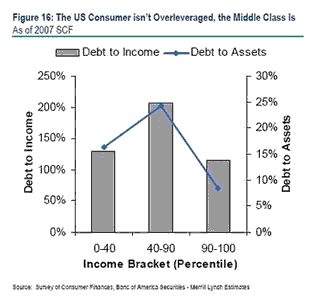

First, they estimate that the top 10% of Americans in terms of disposable income account for 42% of consumption. The 40-90 income percentile (“the middle class”) accounts for 46%, leaving just 12% for the 0-40 percentile.

Combine this with the balance sheet of these various income categories:

Merrill’s headline says it. The middle class is over-leveraged, not The Consumer. What we see is that the over-leverage of the middle class impacts 46% of spending even though its about 60% of the population.

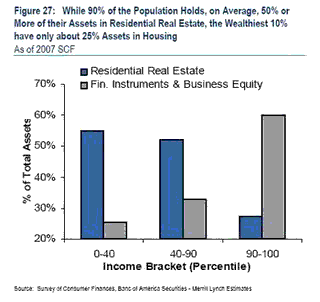

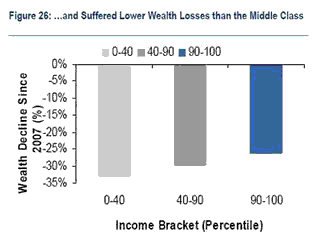

The differential is even more stark when you look at wealth lost as a percentage of assets. Because the middle class’ net worth is mostly their home, the crisis has hit them harder:

We think of the wealthy as being hit hard because of how poorly financial assets have performed, but stocks have rebounded at least somewhat. Homes have not. Add to that the fact that the wealthy tend to have a cushion of assets to support spending should they experience a temporary loss of income. So the highly paid commissioned salesman might not cut back much if his/her income is down for a year. S/he might just spend some savings. The middle class doesn’t have that luxury.

The point is that the wealthy can keep spending at approximately the same rate, and if they represent 42% of consumption in normal times, then maybe consumption won’t fall as much as we feared. Of course, we can’t just dismiss the middle class’ position. I stand by my idea that consumers overall can’t spend at the same rate and will have to continue balance sheet repair.

But this does make you question certain popular trades. Like selling luxury brand companies for “trade down” stocks. If the wealthy are spending but the middle class is cutting back, who gets hurt more? Wal-Mart (NYSE:WMT) or Tiffany (NYSE:TIF)? Toll Brothers (NYSE:TOL) or Ryland (NYSE:RYL)?

Merrill’s piece closes with a warning. All the government programs will eventually come at a cost: rising taxes on the wealthy. Now we find out if that code is worth the price we paid.

- Bulenox: Get 45% to 91% OFF ... Use Discount Code: UNO

- Risk Our Money Not Yours | Get 50% to 90% OFF ... Use Discount Code: MMBVBKSM

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply