What should happen, what could happen, and what will happen?

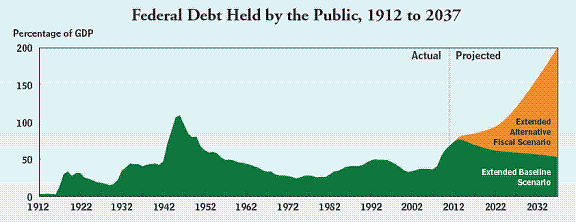

Let’s begin by acknowledging the obvious: the United States faces a very significant long-run issue of fiscal solvency. The graph below, taken from a recent analysis by the Congressional Budget Office, plots projected federal expenditures as a percentage of GDP under two scenarios:

The extended baseline scenario, which reflects the assumption that current laws generally remain unchanged; that assumption implies that lawmakers will allow changes that are scheduled under current law to occur, forgoing adjustments routinely made in the past that have boosted deficits.

The extended alternative fiscal scenario, which incorporates the assumptions that certain policies that have been in place for a number of years will be continued and that some provisions of law that might be difficult to sustain for a long period will be modified, thus maintaining what some analysts might consider “current policies,” as opposed to current laws.

Source: CBO: The 2012 Long-Term Budget Outlook

Obviously any such projections are problematic. Nobody knows with any confidence what U.S. GDP is going to be in 2037. But the basic feature of the CBO’s “alternative” scenario seems indisputable– if historical policies remain in effect for the next 15 years we are going to be in real trouble. There is no ambiguity about the fact that medical expenditures have been rising much faster than other categories, and that the American population is going to continue to age. The historical combination of existing tax rates and the rising federal role in health care is unquestionably unsustainable.

Although I emphatically agree that America needs to make changes today that change the fundamentals of those long-term trends, I do not think it is necessary to do so with immediate tax increases or spending cuts. As Karl Smith observes, with the current negative real yields on government debt, the government is actually making a profit by running a budget deficit, as long as the government’s borrowing cost remains as low as it is at the moment. Granted, we’ve seen some of the European countries move from that situation to one of needing to pay very high interest costs very quickly in response to rapid shifts in investor sentiment. The U.S. would face an enormous problem if the same kind of debt flight were to hit our Treasury auction. That’s one of the reasons why I think it’s extremely important to put in place today policies that permanently change the long-term fundamentals, but whose fiscal bite increases only gradually over time. Examples include the recommendations of the Debt Reduction Task Force, phasing out the Bush tax cuts, raising the retirement age, means-testing Social Security and Medicare, and gradually raising Medicare copays.

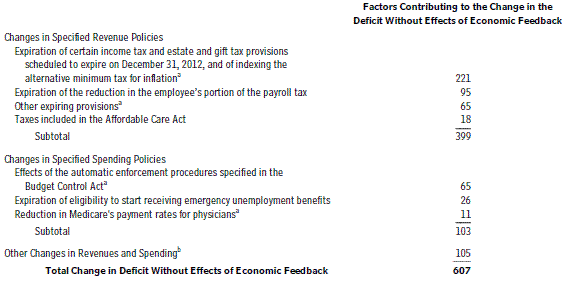

However, the “extended baseline scenario” in the CBO graph above is a far cry from any of those ideas. Existing law tries to make the transition all at once with very significant tax increases and spending cuts. These are scheduled to be implemented at the end of this year, a situation that some refer to as “America’s fiscal cliff.” The tax increases and spending cuts described in the table below sum to over $600 B in fiscal year 2013, a figure that represents about 4% of total GDP.

Source: CBO: Economic Effects of Reducing the Fiscal Restraint That Is Scheduled to Occur in 2013

How big an effect this would have on the economy depends on the fiscal multiplier. Does a $100 B decrease in government spending reduce GDP by more that $100 B (multiplier greater than 1) or less than $100 B (multiplier less than 1)? I personally find the empirical evidence that the multiplier is substantially greater than 1 to be less persuasive than do some of my colleagues. But even if the multiplier were significantly less than 1, a 4% hit to government spending and consumer purchasing power, in an economy that is struggling to keep the growth rate above 2%, would be enough by itself to put the U.S. economy into recession.

A separate issue is the debt ceiling. One of the peculiar embarrassments of the U.S. legislative tradition is that even if Congress arrives at a consensus about how much taxes and spending are appropriate for 2013, it will need separate legislation to authorize the government to borrow the amount that the tax and spending legislation would require. If the government lacks the separate authority to carry out routine fiscal operations, the consequences could be quite disastrous.

So that’s what I think should happen and what existing law says could happen. What do I expect is actually going to happen? I propose that the key question to focus on is this: in whose interest would it be to see the U.S. go off the fiscal cliff into recession?

The clear answer is: no one’s. Democrats don’t want to see that happen, nor do Republicans. The logical thing to expect is therefore that somehow they’ll figure out a way to modify existing law before January 1, postponing the lion’s share of the tax increases and spending cuts for at least another year.

Granted, the specifics of how a compromise will be reached are unclear. And sometimes those playing too close to a cliff find themselves inadvertently falling off. Moreover, even if this all gets favorably resolved in time, the uncertainty itself can be an adverse shock to the economy. I believe that last summer’s debt-ceiling debacle did exert a measurable drag on the U.S. economy.

Although the risks are real, the rational thing to expect is that the actual fiscal contraction next year will be significantly more modest than what is implied by existing law. But the cumbersome process of getting to that outcome will once again exact its own unique toll.

Leave a Reply