Here’s a good example of someone who has learned to rationalize his self-interest so well he does not recognize when he is saying something absurd, from the WSJ:

“If you could set your tick size [minimum bid-ask spread] much wider, market participants will react,” said Jeffrey Solomon, chief executive of banking firm Cowen and Co. LLC, speaking to lawmakers at the hearing Wednesday. “Investors like round numbers–nickels, dimes and quarters.”

… Moving to broader pricing increments could be a boon to providers of equity research, which have been forced to focus on heavily traded, brand-name stocks after the move to pennies, according to Patrick Healy, Chief Executive of Issuer Advisory Group, a consultant to companies on exchange matters.

Brokerage firms often can’t afford to spend money developing reports on thinly traded companies because firms are less likely to make back that money through commissions linked to trades in such securities, said Healy. With less research available on small-cap companies, mutual funds and other institutions may not be inclined to invest in such stocks, he said.

A higher tick size raises the cost for your average retail trader who crosses spreads to transact. If you give the brokerage a greater franchise value, they will spend more on research fluff, but any mutual fund relying on these reports should be restricted to paper trading.

If people really like round numbers, why not apply this to everything. I hate coins, and feel I give more to the take-a-penny-give-a-penny tray than most. No more $2.09 coffee at Starbucks, generating 91 cents of change.

Of course, a firm wishing to increase its relative bad-ask spread it can always push its price down to below $10 via a split share, and some clearly do that.

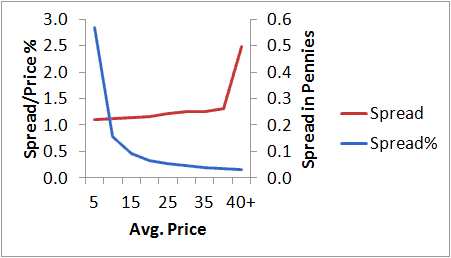

The chart above is taken from data over the past year, and shows a strong increase in the relative magnitude of the spread over the share price as the price goes below $15, so issuers can target this themselves. A Washington solution clearly would favor industry insiders, like Jefferey Solomon of Cowen and Co. LLC.

Leave a Reply