This week the Economist places François Hollande, the socialist presidential candidate who is likely to win the election in France on May 6, on its cover with the headline “The rather dangerous Monsieur Hollande“. A socialist in charge of Europe’s second-largest economy is apparently cause for serious concern.

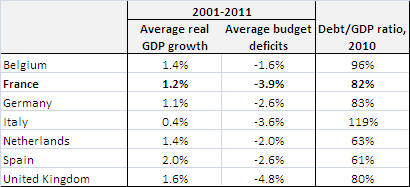

But why? France is overburdened with a massive welfare state and needs to make changes, argues the Economist: “Public debt is high and rising, the government has not run a surplus in over 35 years, the banks are undercapitalised, unemployment is persistent and corrosive and, at 56% of GDP, the French state is the biggest of any euro country.” But looking at the data, France actually does not seem to be doing particularly badly. A look at a few basic economic indicators over the past ten years fails to reveal any obvious signs of an economy that has been oppressed by an oversized government sector, as seen below.

Yes, the French have chosen to allow the government to perform more functions than in many other countries, but economic growth has not been notably worse than its neighbors, and its public debt burden is on par with Germany and the United Kingdom. Despite ideological wishes to the contrary, there is little evidence that countries that choose to have a larger government (within a reasonable range) perform worse economically.

Hollande’s chief sins are, according to the Economist, that he advocates a very high top income tax rate, that he supports a suspension of a planned increase in the retirement age for those who have contributed the longest to the nation’s pension fund, and that he has a generally “anti-business attitude”. But it’s hard for me to see how any of this could spell doom for the French economy. And on the other side of the ledger, Hollande has something extremely important to recommend him to those who care about European economic performance: a potentially strong voice against the counterproductive austerity madness that has dominated eurozone politics for the past couple of years.

The tide may be turning more widely in the battle for the eurozone’s macroeconomic sensibilities; perhaps the steady repetition by certain prominent voices of the simple truth that austerity is counterproductive under current circumstances may finally be bearing some fruit. But if Hollande becomes France’s president, the relative weight of the anti-austerity camp will grow considerably in the eurozone. And that can only mean good news for the future of the eurozone.

Won’t eurozone bond markets be spooked by Hollande’s softness on deficits, though? I doubt it. I tend to think that bond market participants are, on average, quite savvy. And they fully understand (probably quite a bit better than a lot of politicians do) the arguments for why pro-growth policies are the best ways to restore long run fiscal health to eurozone (and other) economies. Instead of causing fiscal armageddon, expansionary fiscal policies could actually reduce national debt burdens in most eurozone countries, given present circumstances.

So rather than be afraid of things like a possible Hollande victory, or the collapse of the conservative, austerity-promoting government of the Netherlands, I actually see such developments as reason for the slightest bit of (cautious) optimism. The eurozone crisis is and always has been primarily a balance of payments crisis, not a fiscal crisis. So if we are finally nearing the end of the disasterous blanket prescription for austerity as the solution to the eurozone’s financial market crisis, that can only be a good thing.

Leave a Reply