It’s been a while since we’ve weighed in on Apple (AAPL). Well, at least a few weeks since our March 30th post as we wondered out loud if the stock needed to fill its March 14th gap open at $568.

The stock subsequently rocked after our post to make a new high at $644 on April 10th. That’s what markets do. They humble you and make it almost impossible to get both direction and timing right simultaneously.

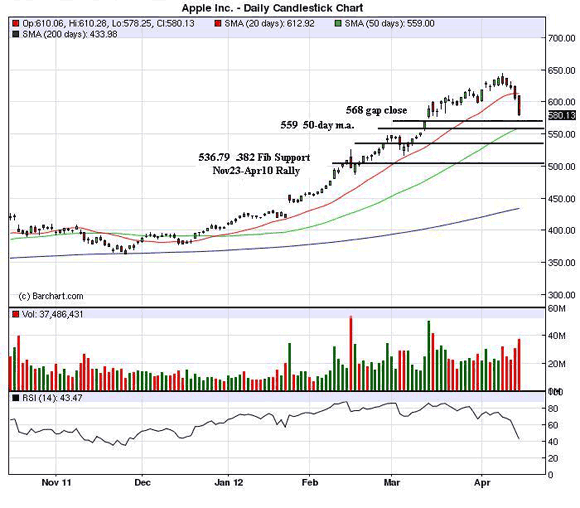

Apple’s stock was down over 4 percent yesterday and has come in almost 10 percent in the past week. It is still up over 40 percent for the year and almost 60 percent since the latest leg of the rally began on November 23rd, however.

Where to now?

Longer term, higher, in our opinion, but it has had a tremendous run, a lot of good news is priced, everyone that needs to own it probably does, and there are just too many bulls and not enough bears, in our opinion.

Next week’s earnings release will be particularly important to see if the new iPad has been the smash hit that the stock had been pricing. We’re not as comfortable going into this earnings announcement as we have been in the past and think it’s healthy the stock is selling off prior to earnings, especially after such a huge run.

We did cite some of our anecdotal evidence of the lack of buzz around the release of the new iPad in our recent post,

We were in the local Apple store last Friday and were surprised by the lack of enthusiasm over the new iPad. Also we noted a couple of customers asking for financing on their new purchases, which Apple does provide — no interest on for 6 months on purchases under $999 and 12 months for over purchases $999. All anecdotal, but interesting, nonetheless.

If new iPad sales disappoint, we expect the stock to get hammered. We’re trying to be patient and hoping the market gives us a better price to buy the stock and selling on the earnings release may provide that opportunity.

The chart illustrates the support and potential entry levels we’re watching.

Actually it has been about a week which is, considering the quality of the commentary, far too short a period. Get long or go home.

Obviously, earnings and iPad sales to be announced next week could disappoint. However, I believe little can be read from absence of the typical clamor for new products at Apple stores any more. The Apple supply chain and greater promotion of online purchases and home/office delivery is, I believe, the result of Apple attempting to reduce the cost of sales by reducing dependence on Apple physical stores. Apple stores today seem to be serving mall customers with no prior experience with Macs and iPads.

I’m delighted to see that Apple is offering rebates on purchases of recent iPad 2 purchases. I was a bit troubled to note that a local Apple store was doing a great business in iPad 2 sales on March 7, the day of the iPad 3 announcement, with no comments to purchasers.