Arnab Das and Nouriel Roubini write today in the Financial Times a commentary suggesting that Euro members should get a divorce (they call it an “amicable divorce settlement”). The current policies will not work and the only solution is the break up of the Euro area to allow some of the economies in trouble get a boost from a depreciation of their (newly created) currencies.

The argument is not new but the article provides a blueprint of how it should be done, which makes the reading more interesting but, of course, it also opens up their argument to more criticism. Let me summarize their proposal before I take my turn on bringing some arguments that suggest that this might not work as well as the authors suggest. Das and Roubini want:

- Portugal, Ireland, Italy, Greece and Spain to abandon the Euro.

- A system of fixed exchange rates (or managed exchange rates) to be introduced in the transition where the ECB will play a strong role defending the announced targets. This system will provide during the transition, the necessary adjustment to exchange rates.

- After a transition, all central banks will implement congruent inflation targets to avoid competitive devaluations.

- Contracts made under domestic laws will be renominated to the new currency. Contracts made under foreign law will remain in Euros.

As I said, it is good to see a proposal with details on how to make the break-up of the Euro area work – and also one that admits its difficulties. Although their arguments are good I remain unconvinced that this would be a good solution. I disagree with their assessment that a one-time shift in intra-Euro exchange rates would generate enough growth. And I have (like anyone else) some “cheap” criticisms about why there are still details that need to be worked out and that in its current form this proposal cannot work.

Let me start with the disagreement on their analysis. At the center of their argument there is a a logic that there is a fundamental misplricing going on in the Euro area. Some countries have lost competitiveness and we need to reset some relative prices back to where they belong to allow for the necessary external rebalancing. This is a standard macroeconomics textbook argument about why systems of fixed exchange rates tend to be unstable and likely to generate misalignments in relative prices.

But the Euro area is not a system of fixed exchange rates where national central banks run independent monetary policy. It is a group of countries (regions?) that share a currency. Inflation does not exist at a macroeconomic level in Greece or Spain. Inflation can only be seen as a microeconomic phenomenon: some prices move in directions that make the factors behind those prices too expensive. We now need to reset to reset those prices to the right level and internal devaluations does not work fast enough so a depreciation of the exchange rate will be a much better tool.

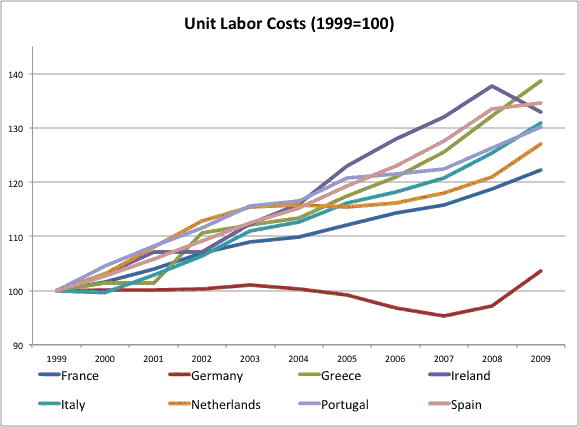

But depreciation of the exchange rate means that all local prices are being reset in the same direction by the same amount? Is this optimal? Is this the right change in relative prices that these countries need? I do not have a perfect answer to this question but I feel uncomfortable making the argument that all domestic prices or wages in these countries are too high. The argument that Greece or Portugal or Spain have lost competitiveness relative to the other Euro countries since the launch of the Euro has been made many times before but as I have argued earlier in this blog, the data is not as clear as many think. What we have seen is one country (Germany) going through a process of increased productivity with limited wage growth and relative to other countries they have managed to reduce their relative unit labor cost. See graph below that I have shown earlier in this blog. Germany is the outlier and not Southern Europe + Ireland.

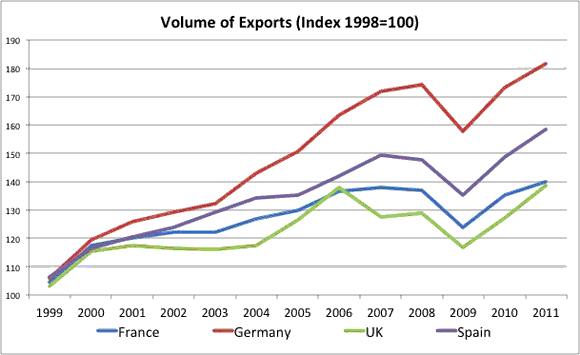

Looking at the performance of exports during the same period of time provides us with a similar message. Let’s compare (volume of) exports of four European economies: Germany, France, Spain and the United Kingdom post 1999.

Yes, Germany’s exports grew faster than any of the other countries but there are small differences between France, the UK and Spain. And out of the three, the one that showed stronger exports growth was Spain. So how can we be so sure that we need to reset the relative prices between Spain and some of those other Euro countries?

One can argue that maybe the past performance was fine but that given the current difficult economic situation of some of these countries, a depreciation will be helpful for a while. This argument is much less convincing. It cannot be that a depreciation is always good for growth (otherwise why don’t we depreciate by 99% the value of their currencies?). The argument needs to be one of setting some relative price to the correct level not simply a one-way argument towards depreciated currencies (the authors agree with this statement when they talk about avoiding competitive devaluations after the transition).

I am also concerned with how some of the details in their proposal will work. To be fair, the authors are aware that the details are not easy and that the potential for capital flights and financial sector instability are very high if we were to have a group of countries leaving the Euro, so I am sure that they share some of the following concerns:

1. How are the new exchange rates decided? And I do not mean the day of the conversion (this is arbitrary and meaningless) but after that. The only way to make this meaningful is by creating a depreciation the months that follow the exit of the Euro area. The authors suggest that it will be a controlled depreciation. Who will make that decision?

2. The moment the depreciation happens, these countries will be poorer as all their imports will be more expensive (e.g. price of oil will jump by whatever is the amount of depreciation of their currency). How will this impact economic growth (consumption, investment,…)? We all understand that there can be potential benefits to exports growth in some sectors but are we sure this is going to work in the short-run? Why is this an important question? Because the debt of governments will be at least as high as today after leaving the Euro. Without growth, the fiscal problems of Spain or Italy will be as bad or worse than today. Are we sure that the loss of confidence in their currencies combined with the immediate shock of making everyone else poorer is going to be compensated fast enough by increasing exports?

3. The authors suggest that contracts under foreign law will still be denominated in Euros. The details matter here. Suppose we convert all the government debt of Italy to the new Lira. The moment the Lira depreciates, the foreign investors will see a loss in their investment. From the perspective of the Italian government nothing has changed. The value of the debt is in Liras and so are all its future revenues (so the Debt to GDP ratio is the same as before). But it is very likely that interest rates will be higher because of the uncertainty and lack of confidence. Will Italy be able to avoid default? Are we sure that exports will grow so fast to compensate for all these costs or risks? I remain skeptical of the ability of exports to react significantly and fast enough to compensate for all the potential costs.

Leave a Reply