When looking at the challenges of government debt in Europe the severity of the problem can look very different depending on the perspective one takes. If we focus on the last 5 years we see that:

1. The government of Spain has more than doubled its (net) debt measured as a % of GDP.

2. In the same period of time Italian (net) debt has also increased by about 20 percentage points of GDP.

The situation seems unmanageable and justifies a quick and radical reaction by those two governments.

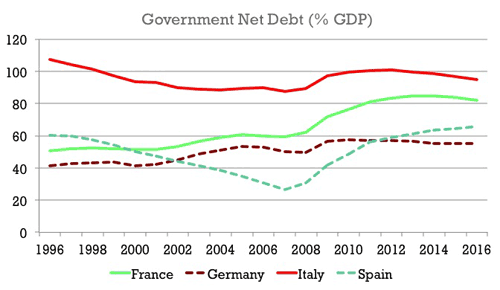

But if we go back a few more years and plot the evolution of government (net) debt for these two countries in comparison to France and Germany, the message is much more comforting. [Data is Net Government Debt as % of GDP from the World Economic Outlook, IMF]

Not only the level of debt is not high by historical standards (in the case of Italy is lower than back in 1996) but it is not far from the other two European countries. Just business as usual. Spain will be slightly above Germany in the coming 5 years but still below the level of France, that has increased at a much faster pace during the last two decades.

A similar analysis can be done for other advanced economies, including the US, and one finds that the level of government debt is certainly high and has increased as a result of the crisis but it is nowhere the levels that are implied by the panic we have observed in markets and politicians when dealing with this issue.

Of course, there is an alternative and much more negative reading that one gets when looking at a longer historical perspective. Government debt is high and governments knew about it twenty years ago and they have not been able to do much about it! Yes, a crisis did not help their efforts but governments need to plan for crisis; one cannot just make budgetary plans assuming that there will never be another recession.

This reading provides a much more pessimistic assessment of fiscal policy in advanced economies. But the solution requires a long-term framework in order to deal with the inability to match spending and income in a way that keeps debt levels sustainable. We have done very little progress to address this issue and this should make us panic. But it is not the deficit in 2012 or 2013 that should worry us, they will be irrelevant in the long term. We do not need short-term austerity we need a way to deal with long-term sustainability.

Leave a Reply