Last weekend I attended the American Economic Association meetings in Chicago where I had been asked to discuss a paper on historical lessons lessons on government debt reduction. The paper is written by Carmen Reinhart and Belén Sbrancia and the title is “The Liquidation of Government Debt”. The paper presents a historical review of episodes where governments paid interest rates on their debt below market rates. This reduction in financial expenses can be seen as a source of revenue that can keep the debt under control or reduce it.

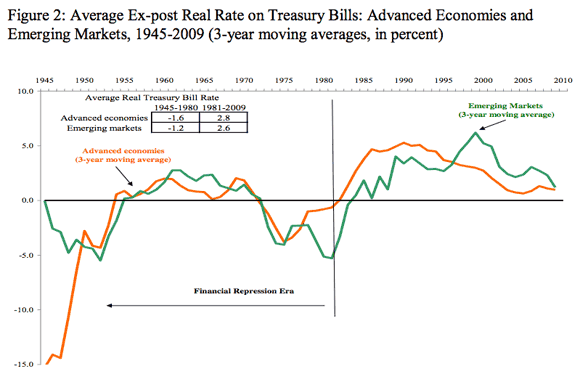

The paper focuses on periods where real interest rates on government debt were negative which were common in the pre-1980 period. Here is a chart from their paper.

They refer to the pre-1980 period as the era of “financial repression” because on average real interest rates were negative driven by the behavior during the 1945-1955 period and the early 70s. Financial repression comes from two sources: financial market regulation (e.g. ceilings on interest rates, legal conditions that favor government debt holdings by institutional investors) and surprises in inflation. The early years of the sample are characterized by capital controls and strong regulations on interest rates. The real negative interest rates of the early 70’s are more driven by inflation being higher than expectations (although controls on capital flows and distortions on interest rates were also present).

A quick calculation shows the importance of this channel during the 1945-1980 period. For example, for the US and UK economies, negative real interest rates allowed a reduction of government debt equivalent to about 2-3% of GDP per year. This is a large amount compared to their ratios of taxes to GDP (this amounts to 14% of the average tax revenues for the US during these years). What this suggests is that the reduction in government debt that advanced economies witnessed in the post-second world war period was partly driven by unusually low (even negative) real interest rates.

The authors argue that we might see something similar going forward. A combination of financial repression (regulation, moral suasion) and inflation could produce negative real interest rates.

Today, the German government issued for the first time debt with a negative (nominal!) yield. This is not financial repression as the authors of the paper describe it. It is more about risk aversion, flight to quality and a reaction of what is happening in other Euro countries, but it has the same effect on the German government. It finances its debt at negative real interest rate (this is one of the benefits of the Euro for the German economy…). Same is true for the US government where over the last years nominal yields have been close to zero while inflation remained positive. Of course, not all governments (Greece, Italy or Spain) are as lucky and can benefit from fear and perceptions of risk, their real interest rates remain positive and high.

Leave a Reply