There is little to no fanfare for the release of this report, (why do they release at such a distracted time of year, where people will ignore it?) which strips away a lot of the malarkey that the US Government delivers by providing data on an accrual basis, rather than on a cash basis, which is what the politicians argue about. As a result, the politicians take actions that hurt the future in order to benefit the present. If we viewed the national budget the way this report does, we would have had very different policies over the last 25 years.

As it is the report gives credit to Obamacare for lowering the costs of Medicare, as if a stroke of the law could reduce the medical needs of the elderly. If it does decrease actual demands on Medicare, unlikely but good. If not, we need to revise estimates up, as the alternative scenario on page 134 does. (PDF pg 156) And perhaps more than that.

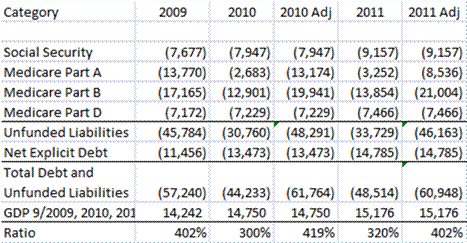

Here are the figures for the last three years:

The big shift was the passage of Obamacare, which was funded by a large cut to Medicare Parts A & B. It’s not as if that law repealed the health care needs of the elderly, but only the rates at which doctors would be paid. If the ultimate amounts to be paid by the government don’t shift, because we adjust the law & payments to meet undiminished need later, the 2011 Adjusted figures would be low by around $5 trillion.

The 2010 Adjusted figures attempt to strip out the distortions created by Obamacare. The 2011 figures leave in the adjments from Obamacare, but reflect the Illustrative Alternative Scenario on page 133:

The Medicare Board of Trustees, in their annual report to Congress, references an alternative scenario to illustrate the potential understatement of costs under current law. This alternative scenario assumes that the productivity adjustments are gradually phased out over the 16 years starting in 2020 and that the physician fee reductions are overridden.

These examples were developed by management for illustrative purposes only; the calculations have not been audited; and the examples do not attempt to portray likely or recommended future outcomes. Thus, the illustrations are useful only as general indicators of the substantial impacts that could result from future legislation affecting the productivity adjustments and physician payments under Medicare and of the broad range of uncertainty associated with such impacts. The table below contains a comparison of the Medicare 75-year present values of income and expenditures under current law with those under the alternative scenario illustration.

Another factor in holding down the 2011 deficit was that measured inflation was low, there were no cost of living adjustments [COLAs], when assumptions expected 2.5% or so. To the extent that COLAs remain low in future years, there will be further positive adjustments.

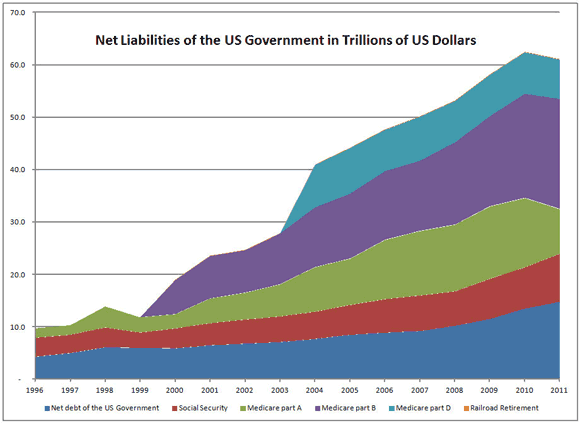

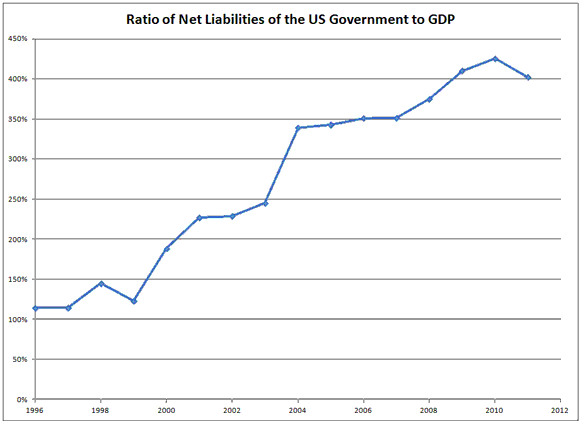

In closing, here are two graphs that display the net liabilities of the US Government and the ratio of that to GDP:

To pay down liabilities like these would require the permanent allocation of an additional 8% of GDP. Where would we find the will to do that? I suspect as a result that we will see real decreases in Medicare benefits — things that won’t be eligible for payment. Hospice care will be indicated at higher frequency when healing an old person would be costly.

So just be aware that something has to change, either taxes have to rise, or Medicare benefit levels have to fall.

Leave a Reply