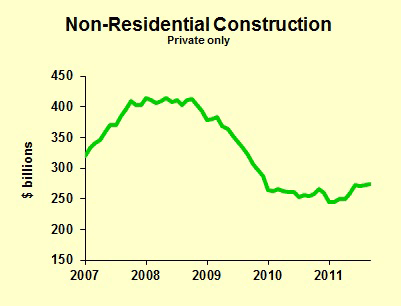

Real estate markets are unbalanced in most parts of the country: vacancy is too high, but construction is too low. That sounds contradictory, because construction should be low when vacancy is high. Looking forward, however, we’ll find insufficient supply when the economy improves.

Underlying this view of real estate is an economic outlook (more details in my Economic Forecast 2012-2013) for moderate growth in the coming two years. We won’t have enough growth to get us back to feeling good again. The unemployment rate will remain above normal, but declining to about 7.5 percent. Moderate economic growth will increase demand for all kinds of real estate, both residential and non-residential.

The current pace of construction is well below net absorption in most parts of the country, pulling the vacancy rate down. Net absorption should pick up in 2012, but the pace of construction won’t keep pace. Most construction planning is going on in cocktail hour chatter, not formal discussions with architects and bankers. Money is still tighter than average, though not quite so hard to come by as a year ago. Many developers lack the equity that their bankers want, especially with so much doom and gloom pervading the country. The key fact to remember, however, is that demand for space can grow much faster than space can be built. This applies in spades to downtown office towers, and also in less dramatic effect to suburban office, industrial, flex space and retail.

We’ve had high vacancy rates and low construction in the past. What usually happens—but isn’t happening now, at least not yet—is that developers look forward, see the tighter rental market, and then begin speculative projects. This reduces the swings between high vacancy and low vacancy. Instead of the market tightening to an extreme, low vacancy rate, the new speculative supply satisfies the rapid increase in demand. Because that’s not happening now, we’ll see a pronounced move to a landlord’s market in a few years.

Past real estate cycles have been dominated by interest rate swings. All we have now is downward creep in long-term interest rates for those with good credit, and no loans available to those with less-than-great financials. Going forward, long-term interest rates will rise but not to such high rates that development is choked off. The key issue is demand for space.

The biggest risk to Main Street America today is the European financial crisis. Over the past decades United States exports have increased substantially, now totaling about two trillion dollars a year. When adjusted for inflation, our exports have doubled since 1996, tripled since 1990, quadrupled since 1987. Most of today’s business leaders gained their experience in a time when international trade played a much smaller role in the economy. The news from Europe is tedious, for sure, greatly complicated and changing daily. The big picture is simple, however: Europe is on the brink of recession. A financial collapse on the Continent will clobber many United States companies, reducing their need for offices and industrial space, in turn reducing consumer spending, retail space demand, and families’ ability to pay for housing.

The most likely forecast is that Europe muddles through its problems and thus the United States enjoys moderate but not great economic expansion. Contingency planning for the unpleasant alternative is vital, not just for giant exporting corporations but for local real estate professionals as well.

Leave a Reply